Global| Oct 08 2025

Global| Oct 08 2025Europe’s Economy Holds Up, but Headwinds Mount

|in:Viewpoints

Europe recovery to continue

The euro area’s economic performance in 2025 has been uneven. The year began on solid footing, with GDP expanding by 0.6% QoQ in Q1, only to lose momentum in Q2 as growth slowed sharply to 0.1% QoQ, with output contracting in both Germany and Italy. This slowdown coincided with the peak of the U.S.-led trade war, which weighed heavily on net exports after their strong rebound earlier in the year.

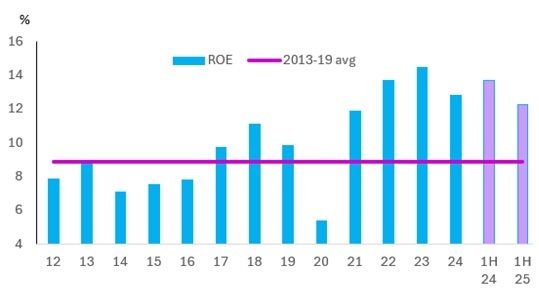

Despite the softer second quarter, Europe’s business cycle upswing remains intact. As shown in Figure 1, the average return on equity for listed European firms moderated in the first half of the year compared with the same period in 2024. Yet the corporate profit cycle, which began in 2021, continues to advance. Key indicators—EBITDA, free cash flow, and retained earnings—remain well above pre-pandemic averages. Although earnings per share and cash flow softened slightly in 1H25, corporate balance sheets remain healthy and capable of supporting further investment in production capacity and employment.

Figure 1: Europe average return on equity

Source: Haver Analytics & Westbourne Research

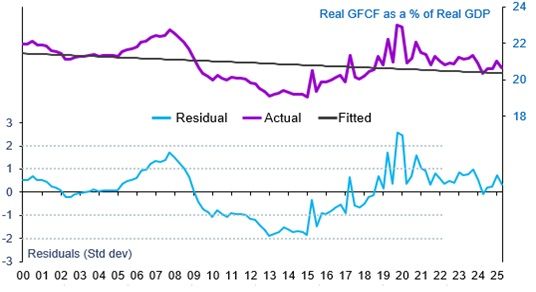

The investment cycle also remains in expansion. As Figure 2 shows, investment spending fell 1.8% QoQ in Q2 after a 2.7% jump in Q1, suggesting a short-term correction rather than the onset of a broader slowdown. The macroeconomic backdrop remains supportive: interest rates are falling, fiscal policy is accommodative, and the worst of trade-war uncertainty has passed. Encouragingly, momentum is building—particularly in Germany—to ease regulatory burdens and advance deregulation, improving the business environment and competitiveness.

Figure 2: Europe investment cycle

Source: Haver Analytics & Westbourne Research

Meanwhile, the European Central Bank (ECB) retains room to ease policy further. Inflation remains far better contained than in the U.S.: headline inflation in the euro area has held steady at 2.1% YoY, while a strong euro continues to dampen producer and import prices. There are no signs of pipeline inflation. By contrast, U.S. CPI rose to 2.9% YoY in August, well above the Federal Reserve’s 2% target.

The labour market remains resilient. Unlike in the U.S., where unemployment has edged higher, the euro area jobless rate continues to decline. Wage growth across services and manufacturing remains solid—up 4% YoY in 1H25, slightly slower than in 2024. In real terms, wages grew 1.9% YoY, down from 2.2% a year earlier but still consistent with sustained consumer spending. Real retail sales are rising about 2% YoY, with momentum easing in Germany, France, and Italy, while household credit demand is reviving as rates fall—pointing to firmer consumption ahead.

In summary, Europe’s cyclical recovery remains on track, but its growth will continue to lag the U.S., weighed down by deep structural challenges.

Europe’s structural headwinds to weigh

The U.S.–EU trade war may have officially ended, but Europe has come away with a poor deal. Under the new framework, EU exports to the U.S. face a 15% import tariff—down from the previously threatened 30%, but still substantial. Only a few sectors—such as aircraft parts, chemicals, agricultural goods, and semiconductor equipment, worth roughly €70 billion in trade—enjoy zero tariffs. Tariffs on metals remain unchanged. In return, the EU agreed to eliminate tariffs on U.S. industrial goods and ease non-tariff barriers. As a result, the average U.S. trade-weighted duty on EU goods has surged to 16%, up from 1.36% at the start of the year, now affecting nearly all EU exports. The euro’s 17% appreciation against the dollar since January adds further pressure, eroding competitiveness.

Europe’s concessions go beyond tariffs. The bloc has pledged to invest €600 billion in the U.S.—around 3.3% of EU GDP—focused on energy, defence, and infrastructure, and to purchase at least €750 billion of U.S. energy through 2028. These commitments pose fiscal and balance-of-payments risks, diverting demand from domestic producers and straining external accounts. The tariff shock has exposed deeper structural weaknesses in Europe’s competitiveness, particularly in cost efficiency and productivity, suggesting a prolonged adjustment period for exporters already facing high input costs.

According to the European Commission’s 2025 Competitiveness Report, Europe’s position in advanced technologies continues to deteriorate. The EU’s share of global tech revenues has fallen from 22% in 2013 to 18% in 2023, while the U.S. share has risen to 38%. Energy prices in Europe remain two to three times higher than in the U.S., and R&D spending—at 2.2% of GDP—lags far behind global peers such as Korea (5.2%) and the U.S. (3.6%). Productivity stands at roughly 77% of U.S. levels, and SME productivity has fallen from 68% to 60% of large firms’ productivity since 2008. Regulatory fragmentation—with 270 regulators and over 100 tech-related laws—combined with limited access to financing, has stifled innovation. Europe’s share of global FDI flows has plunged from 34% in 2019 to 17% in 2024, while venture capital investment, at just 0.05% of GDP, is one-tenth that of the U.S.

At the same time, geopolitical pressures are intensifying. President Trump has largely disengaged from the Ukraine–Russia conflict, shifting responsibility to Europe. At the 2025 Hague Summit, NATO members pledged to raise defence spending to 5% of GDP by 2035, including 3.5% for military spending and 1.5% for dual-use infrastructure. Europe’s ReArm Plan, aimed at closing capability gaps and strengthening defence industries, carries an €800 billion price tag.

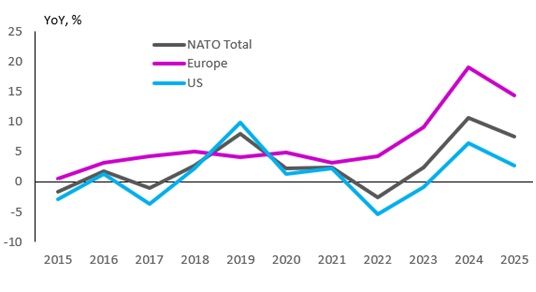

Defence spending is already accelerating (Figure 3). European outlays are projected to reach €381 billion (2.1% of GDP) this year, up from €343 billion in 2024. Investment is up 23% YoY, with equipment procurement exceeding €100 billion. Real defence spending is expected to rise 14% this year after 19% growth in 2024, outpacing the U.S. While this underscores Europe’s determination to enhance security and autonomy, it also highlights the heavy fiscal burden facing a continent struggling with weaker competitiveness, a costly transatlantic trade deal, and the economic fallout of a shifting global order.

Figure 3: Growth in defence spending, real terms

Source: NATO & Westbourne Research

Fiscal pressures are also mounting. France’s budget crisis has dominated headlines, with Prime Minister Sébastien Lecornu the latest to resign after failing to secure cross-party support for next year’s budget. Political uncertainty has deepened, and outcomes remain unclear.

At first glance, Europe’s fiscal position looks solid. According to Eurostat, the euro area’s budget deficit averaged 3% of GDP in Q1, with public debt at 86.5% of GDP—figures that compare favourably with the U.S., where the deficit reached 5.7% and debt 119% of GDP in 1H25. Yet these headline numbers mask growing fragility.

As defence costs rise and fiscal strains broaden, governments are likely to rely on creative accounting and debt mutualisation to avert another euro area debt crisis. The process is already underway. Following the precedent of the post-pandemic EU Recovery Fund, the European Commission has launched a new mechanism—the Security Action for Europe (SAFE)—to raise up to €150 billion in joint borrowing for defence investments. More such instruments are expected as fiscal demands expand.

Meanwhile, member states have been allowed to invoke the national escape clause of the Stability and Growth Pact, enabling them to exceed EU public spending limits by up to 1.5% of GDP for four years.

Conclusion

Europe’s cyclical upswing remains intact, but the region faces an uphill climb. Structural weaknesses in competitiveness, high energy costs, and escalating fiscal pressures risk constraining growth well below U.S. levels. While policy support and deregulation efforts may sustain the recovery, Europe’s long-term outlook will depend on whether it can rebuild productivity, technological capacity, and fiscal resilience in an increasingly fragmented global economy.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.