Are Foreigners Paying the Tariffs?

by:Joel Prakken

|in:Viewpoints

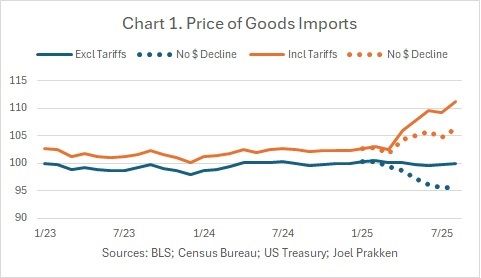

From January to August the average tariff rate on all imported goods increased 9 percentage points, from 2.3% to 11.3%, while the price of those imports, recorded by the Bureau of Labor Statistics (BLS) excluding tariffs, was essentially unchanged. Hence, the price of imports, including tariffs, rose 1.113/1.023 - 1 = 8.5%, reflecting the full amount of the increase in tariffs (Chart 1, solid lines). This suggests the cost of the tariffs has been borne entirely by American businesses and consumers, with none of that cost passed backwards to foreign suppliers.

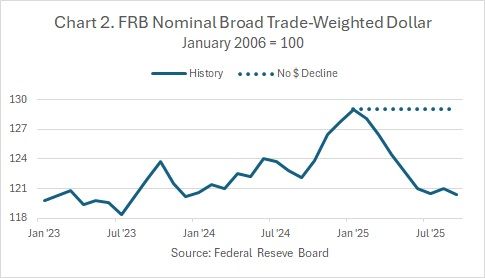

Ceteris, however, are not paribus. Over those same months - and somewhat paradoxically - the Federal Reserve’s broad, nominal, trade-weighted dollar index declined 6.7% (Chart 2), one of the steepest year-to-date depreciations on record. I say paradoxically because the textbook narrative is that tariffs, by reducing the demand for imports and hence the supply of dollars to the rest of the world, put upward pressure on the dollar that offsets the cost of the tariffs by putting downward pressure on the price of imports. In 2025, however, depreciation has re-enforced the inflationary impetus of the tariffs and, in the process, may have obfuscated a shift in the burden of tariffs backwards onto foreign suppliers.

We cannot observe the counterfactual path of the dollar, and we can certainly debate the causes of the recent depreciation. Perhaps it reflected the approaching, expected, late year easing of monetary policy. Yet given the timing of the dollar’s decline, the most reasonable explanation is that the uncertainty caused by the Trump Administration’s policies on immigration and (especially!) tariffs encouraged a shift away from dollar-denominated assets.

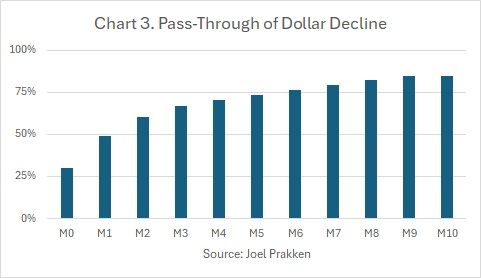

Be that as it may, using monthly data since 1989, I estimated the pass-through of fluctuations in the Fed’s dollar index to the BLS index of the price of imported goods. The results suggest that 85% of a persistent depreciation is passed through to higher import prices over 11 months, with the response front-loaded (Chart 3). Using this model I then simulated the recent path of import prices, assuming no decline in the dollar since January. The results (Chart 1, dashed lines) suggest that had the dollar not declined this year, the price of imports excluding tariffs would have fallen 4.7% by August, while the price of imports including tariffs would have increased only 3.7%, not the 8.5% reflecting the full amount of the new tariffs.

While the inference is indirect, the ratio of (8.5 – 3.7) / 8.5 = 57% can be interpreted as an estimate of the share of the cost of the new tariffs shifted backwards onto foreign suppliers.

A PDF version of this commentary is available here.

Joel Prakken

AuthorMore in Author Profile »Joel Prakken is former Chief US Economist of S&P Global and IHS Markit, co-founder of Macroeconomic Advisers, and past president and director of the National Association for Business Economics. He has served as an outside advisor to the Congressional Budget Office, on the Advisory Panel of the Bureau of Economic Analysis, and as a consultant to the Joint Committee on Taxation. He holds a BA in economics from Princeton University and a PhD in economics from Washington University in Saint Louis.