Global| Aug 05 2025

Global| Aug 05 2025Global Outlook Brightens for 2025

|in:Viewpoints

After a turbulent first half of the year, summer has brought calmer conditions for the Trump administration, the global economy, and financial markets. Major US trading partners have signed or are negotiating new trade agreements. While we previously noted that finalising these deals would take time, the easing of trade tensions alone has been enough to draw businesses, consumers, and investors back into action.

The view that the second half of 2025 will outperform the first remains intact, supported by solid business cycle fundamentals.

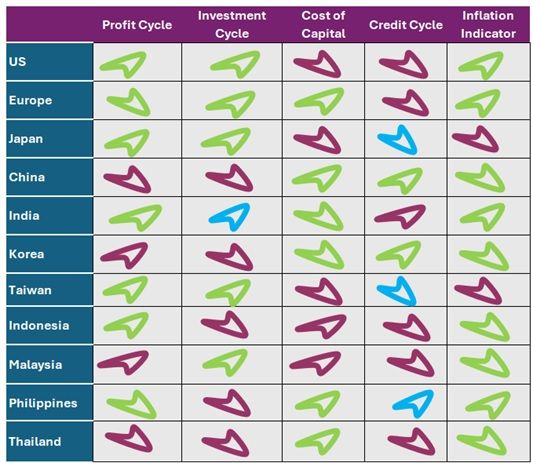

Business cycle indicator assessment

Figure 1 summarises the latest business cycle assessments. Green signals positive conditions, blue neutral, and maroon negative, with arrows showing momentum.

Since the last review: • Unchanged: US, China, India, Korea, Indonesia • Improved: Europe, Malaysia, Philippines • Weakened: Japan, Taiwan, Thailand

Europe’s uptick stems from an investment cycle rebound ahead of the tariff war. In Malaysia and the Philippines, broad money growth has turned positive, signalling stronger activity ahead without inflation risks.

Japan’s deterioration reflects an unusually low two-year real lending rate (-2.8%), which points to inflation risks but is tempered by slowing broad money growth and a weakening credit cycle. Inflation is moderating—3.2% YoY in June vs. 4% in January—despite public dissatisfaction over living costs.

Taiwan shows weakening broad money growth and credit, suggesting slowing domestic momentum. Thailand fares worst: the investment cycle is in downswing, leaving three of its five business cycle indicators negative.

Conclusion: Shifts in scores are not large enough to warrant changes to 2025 investment recommendations.

Figure 1: Business cycle indicator assessment

Source: Westbourne Research

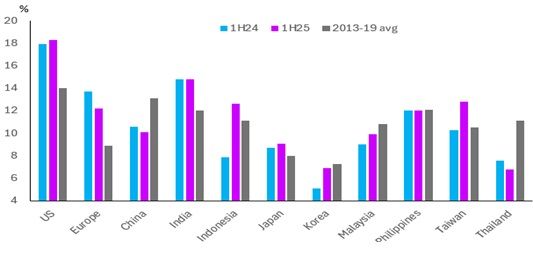

The corporate profit cycle

As regular readers—and followers of Austrian economics—will know, the profit cycle is a critical leading indicator. It marks the turning points of both the business cycle and stock markets, and in fact, precedes them. When the profit cycle turns down, it signals that the economy is heading for a slowdown at best, a recession more likely, and in the worst-case scenario, a full-blown bust. For equity investors, the peak of the profit cycle is the earliest and most reliable signal to sell and take profits.

Figure 2 tracks average return on equity (ROE) for listed sectors—a proxy for corporate profit trends. • Strengthening or Stable: Most countries, including the US, Japan, Taiwan, Indonesia • Weakened: China, Thailand

In the US, rising profitability supports the stock market rebound and quells fears of a tariff-driven recession. Indonesia surprised with a sharp ROE jump—from 7.9% in 1H24 to 12.6% in 1H25. Europe’s ROE eased (12.2% from 13.7%) but remains healthy. India’s profits held steady.

Figure 2: Return on equity

Source: Bloomberg & Westbourne Research

China remains a key outlier: high debt, excess capacity, and intense competition—especially in solar, wind, and EV sectors—continue to pressure margins. Price wars have prompted Beijing to push for consolidation and curb aggressive discounting.

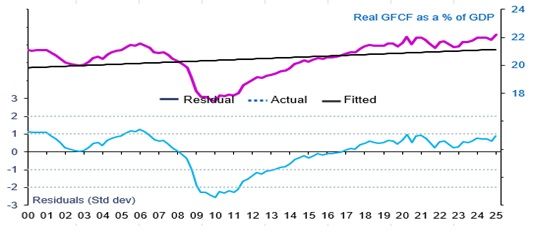

The investment cycle

The profit cycle leads the investment cycle, which in turn drives the credit cycle. Rising profits encourage firms to expand capacity, creating jobs and supporting wage growth. Entrepreneurs launching new products behave differently: they invest to meet unmet demand, often using seed capital or loans. If demand materialises, costs fall, markets expand, and investment accelerates.

Currently, investment cycles are in upswing in the US, Europe, Japan, Taiwan, and Malaysia. In the US, the ratio of real investment to GDP continues to move above trend, confirming the cycle’s strength (Figure 3).

Figure 3: US investment cycle

Source: Haver Analytics & Westbourne Research

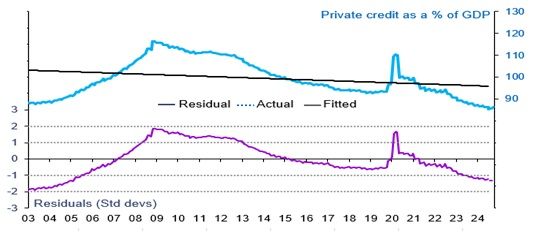

The credit cycle

Credit cycles are in downswing in the US, Europe, India, Indonesia, Malaysia, and Thailand, and weak in Japan, Philippines, and Taiwan.

Even with aggressive ECB rate cuts, credit demand in Europe remains subdued. This is normal in early-stage investment upswings, as firms initially fund growth from internal resources. Credit demand typically picks up only once confidence in demand, earnings, and wage growth is entrenched.

In India and Indonesia, credit cycles will not turn until their investment cycles reverse—likely with a lag. Japan, Taiwan, and the Philippines face soft credit demand due to recent trade tensions, political uncertainty, and living-cost pressures.

The only economies where credit is growing faster than nominal GDP are China and Korea. In China, this is largely due to central bank and government stimulus, with private sector demand still weak. In Korea, household borrowing drives the expansion.

Figure 4: Europe credit cycle

Source: Haver Analytics & Westbourne Research

The cost of capital

In six of the eleven countries—Europe, China, India, Korea, Philippines, Thailand—real lending rates are appropriate for their business cycle stages, giving central banks room to cut without stoking inflation.

Indonesia, Japan, Malaysia, and Taiwan have negative real rates outside normal ranges. Taiwan and Malaysia are extreme cases, making near-term rate cuts unlikely.

In the US, the real cost of capital has risen for 10 straight quarters, from -6.4% in 4Q22 to 2.7% in 1Q25. Monetary policy is tight, and while Trump’s criticism of Powell for not cutting rates faster has some basis, the Fed’s caution is understandable.

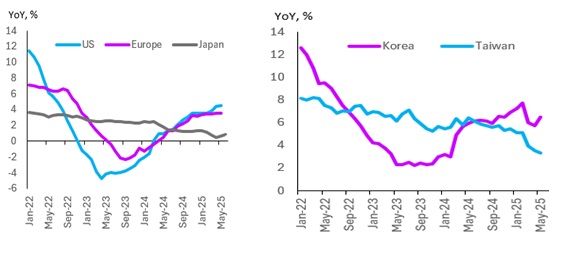

Broad money growth

Broad money growth is a leading indicator for inflation and monetary policy shifts. Central banks often respond late, so investors should watch money growth closely for early signals.

Figure 5 and 6 show money supply growth trends. The key takeaways are: first, if the US Fed is sitting tight, it’s with good reason. Broad money growth is picking up and so is headline inflation. This is also reason for the ECB to stay on hold. Second, despite negative real lending rates and talk of another fiscal stimulus package and a cut in the consumption tax the BoJ is likely to hesitate to tighten. Third expect central banks in Korea and Taiwan to err on the side of caution.

Figure 5: Broad money growth trends 1

Source: Haver Analytics & Westbourne Research

Fourth, at best the Reserve Bank of India will deliver another 25bps in policy interest rate cuts this year. Finally, Figure 9, Chart 2, shows ASEAN broad money growth is easing, implying that there is room for their central banks to reduce lending rates. However, there is no urgency. Capital is priced neither too high nor low.

Figure 6: Broad money growth trends 2

Source: Haver Analytics & Westbourne Research

In summary

Across our eleven-country universe, aggregate business cycle scores have improved. Corporate profit cycles are strengthening in more economies than they are weakening. Investment cycles are in upswing in five major economies—most notably the US, Europe, and Japan, which together account for nearly half of global GDP.

Credit cycles are lagging, but this is expected and not a concern. The cost of capital is broadly appropriate, with rates too low in Japan and Taiwan. Broad money growth is accelerating in the US and Europe, consistent with a cyclical pickup in inflation, but far from the 2022–23 inflation shock.

The second half of 2025 should bring better economic conditions, supported by improving profits, expanding investment, and stabilizing global trade relations.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.