French IP Is Expanding But Had a Tough Month

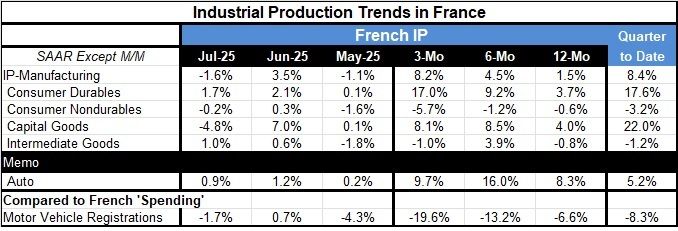

The end of summer is turning out to be a difficult time for France even though industrial output is in a seemingly solid trend. Output in June rose by 3.5%, it did that after a weak May when output fell by 1.1% and now in July output is falling by 1.6%. By itself, the manufacturing trend is simply not that worrisome, but it is built upon somewhat more convoluted trends with July’s drop. Add this complication to a political environment that is quite difficult as in real time, in September, France's government is being dissolved, the Prime Minister is being dismissed, and President Macron is under pressure. There is a decidedly split and fractured legislature to deal with as he is going to have to appoint yet another prime minister, the second lost government in less than a year. Macron continues to resist calling elections or stepping down himself.

France has been called out by the markets for the size of its government sector and its debt as Macron’s earlier tax cuts produced fiscal deficits not growth. French deficits continue to push up bond yields toward levels being paid by Italy. The U.K. is also under pressure for its substantial indebtedness and its inability to get control of its economy and generate growth. None of these are new trends and certainly not foreign to anyone in the United States where large fiscal deficits, concerns about future fiscal deficits, and President Trump's own concern about deficits as exhibited by his attempt to try to push interest rates down to reduce the interest cost of the debt. This has pushed the fiscal budgeting process into the mainstream of making monetary policy creating a clash over central bank independence in the United States- with reverberations abroad.

The best way to keep debt or the size of the government sector from becoming a problem is to control it and none of these governments seem to have been able to do that. A country that is going to rely on debt and increasing indebtedness is pushing the day of reckoning out on the future generations. That becomes increasingly unpalatable as population growth has been slowing. Slowing population growth and rising debt levels are an extremely bad combination and yet we see these as real international trends.

In France, the one-year trend for industrial production in manufacturing is still relatively solid at 1.5% growth over 12 months, stepping up to 4.5% at an annual rate over six months and up to 8.2% annualized over three months. On the face of these figures, if they hold up, the progression for growth is pretty good. However, when we see what produces these results in the table, which is a sharp drop in May and July, with a sharper increase sandwiched in between, we are left wondering whether the sequential trend is going to hold up at all. Consumer durable goods output trends are one of the reasons that that output trend in manufacturing is so strong with positive growth in May, June and July; the sector logs 12-month growth of 3.7%, 6-month growth at 9.2% at an annualized rate, and 3-month growth at a stunning 17% annual rate. That would seem to be a lot of strength to carry the day, but consumer nondurables output trends point in the opposite direction with -0.6% over 12 months, a -1.2% annual rate decline over six months and then -5.7% at an annual rate over three months. The capital goods sector sides with growth with a 4% rate over 12 months and an 8.5% pace over six months and that largely holds up at 8.1% over three months. However, the sequential growth rate for intermediate goods shows a drop in output of 0.8% over 12 months, a nice rebound with a 3.9% annual rate over six months and then the declining pace of 1% annualized over three months – a bit less coherence.

Transportation output in France is considerably stronger than the trends in motor vehicle registrations. Even though output in the auto sector continues to be quite firm to strong, registrations are weakening. That can’t be good.

France is clearly in a difficult spot with President Macron also caught between a political rock and a hard place given the importance of Algerians in the French economy and given the conflict in Israel involving Hamas in the Gaza Strip. His political base domestically is severely fractured, and economic performance now is spotty. One good bit of news for the European Monetary Union is that, while inflation runs mildly over the top of its target, it is not accelerating; the ECB seems content to let inflation set at a pace slightly above its target as long as it continues to mind its business there.

It's certainly a bad time for France to be dealing with geopolitical tensions in the Middle East and Ukraine and with these political divisions at home they're deepened by those kinds of divisions as well as an economy that's showing signs of stress, signs that have been inevitable to show up in the wake of the recovery from COVID since governments did so much to try to bail their economies out. The unwinding of those actions has been destined, for some time, to create management problems for the economy and for continuing growth globally. For the time being, governments have managed the situation by tolerating inflation overshoots and pretending that having inflation over target is fine. However, Trump's tariffs seem to be calling the bluff on that to some extent. Tariffs will exacerbate inflation pressures and probably chill growth prospects at least by increasing uncertainty in the short run. This means that the risk of a downturn has risen but it's not clear that it's risen to a point that should be concerning although it certainly could be. It's more likely to be an issue and economies that have continued to place a great deal of emphasis on government efforts to sustain growth.

The next few months could be pivotal for global growth not just in France, as we begin to see what challenges tariffs are going to propose for local economies in terms of adversely affecting growth and adversely affecting inflation. The problems have been manageable so far, will that continue? That essentially is the question for the outlook.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global