Euro Area IP Makes Modest Rebound—or Does it?

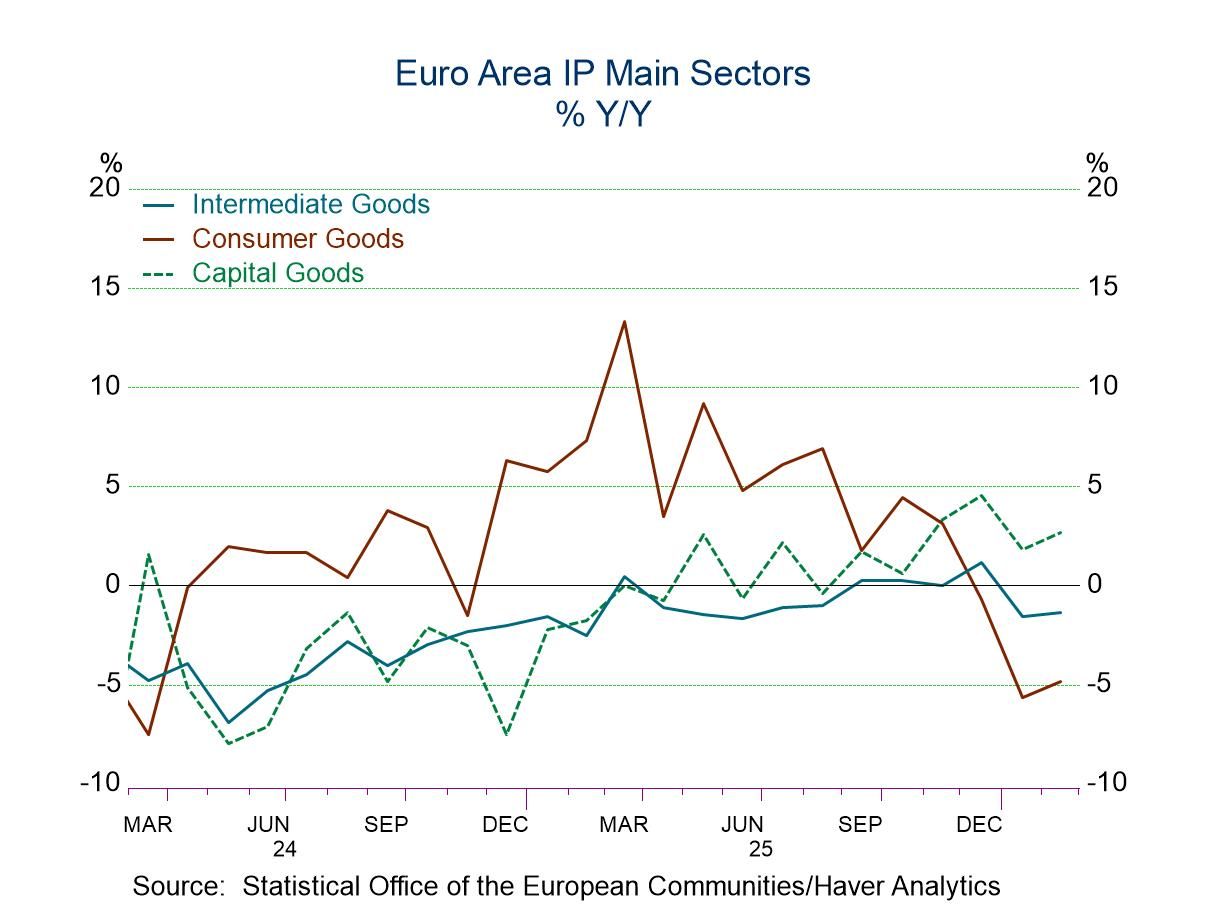

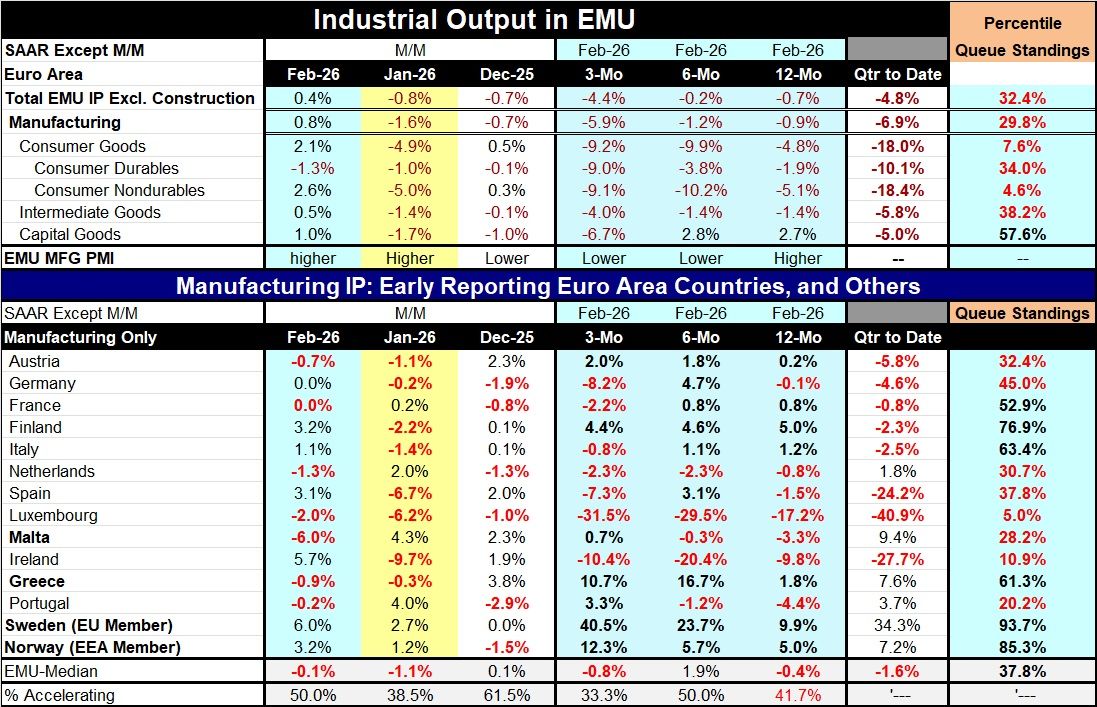

The rebound that wasn’t Industrial production rebounded without vigor in February, gaining 0.4% after falling by 0.8% in January. Moreover, the trends are poor and show no sign of stabilization. 12-month to 6-month to 3-month overall output is sinking faster than is manufacturing output. And all the major manufacturing sectors show either clear signs or strong hints of progressively faster declines in output.

Half or more of the countries in the table report output falling in January and in February. This is not a stabilizing condition.

All sectors show quarter-to-date (QTD) declines in the unfolding Q1 output stream, and only six countries show QTD output increases in progress. The breadth of output increases is poor, and their trends for growth are extremely poor. So I have to brand this rebound as technically visible in February alone, but in a broader perspective, conditions are weakening.

In terms of sectors, only one EMU-wide sector has a 12-month growth rate above its median pace—that sector is capital goods, with a ranking in its 57th percentile compared to the median whose ranking is 50%. Only six countries in the table have manufacturing growth rates that exceed their historic median pace. That makes the breadth of IP growth as weak as well.

Not reassuring There is nothing reassuring about the February IP report, and it precedes the onset of the Iran war. We have since seen very broad weakness ahead in the S&P PMI indexes. We are certainly headed for a difficult period ahead. Since the period of international disruption has just begun in March, we are entering this difficult time in a weakened position. It would seem to be a good time to get defensive since inflation is bound to go up and high oil prices will weaken demand and already are creating some significant local chaos in developing economics that already were hand-to-mouth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global