Data that Have Caught My Eye – Equities, CPI Inflation and Bank Credit

|in:Viewpoints

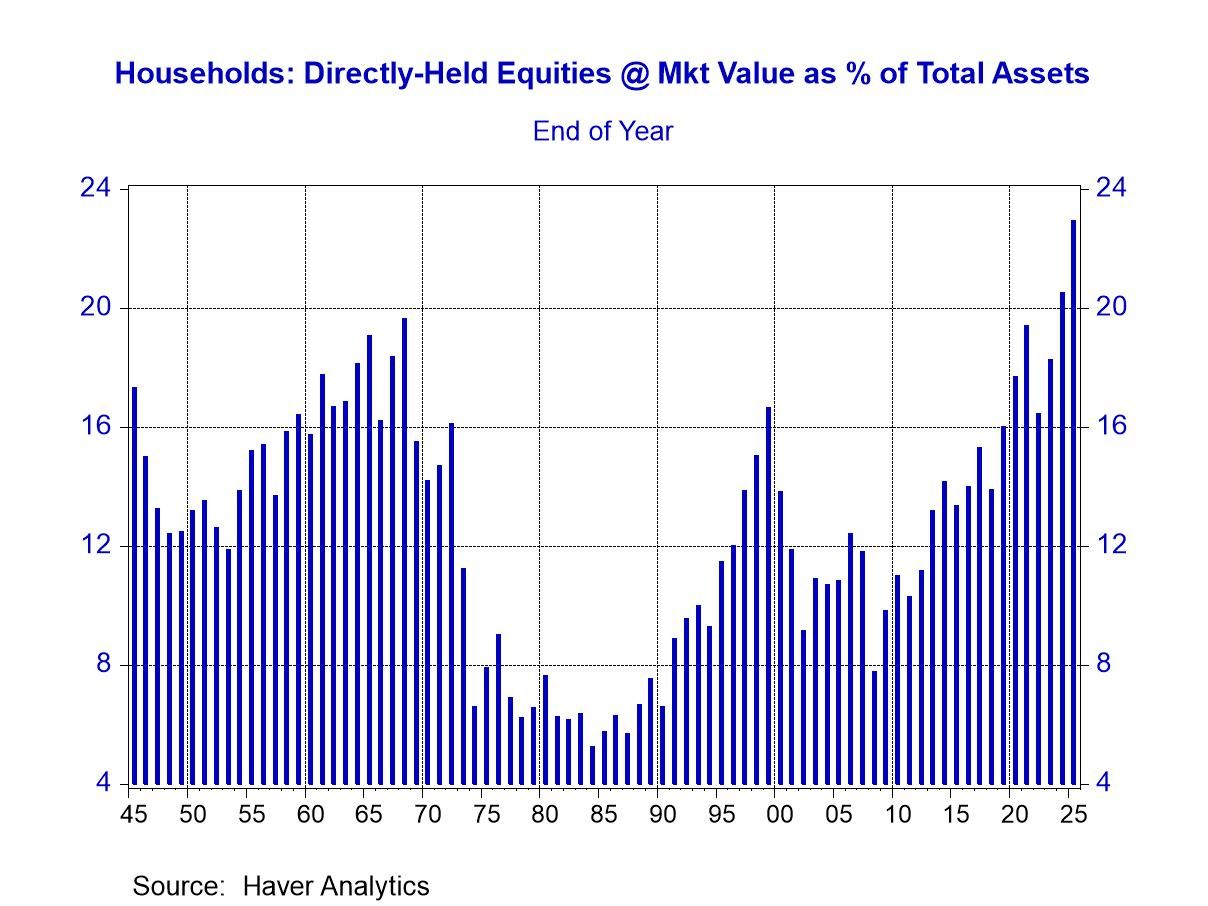

Let’s look at some data related to US equities first. Plotted in Chart 1 are the end-of-year values of directly-held equities held by households at market value as a percent of households’ total assets at market value. At the end of 2025, this percentage was 22.95, a post-World War II record high.

Chart 1

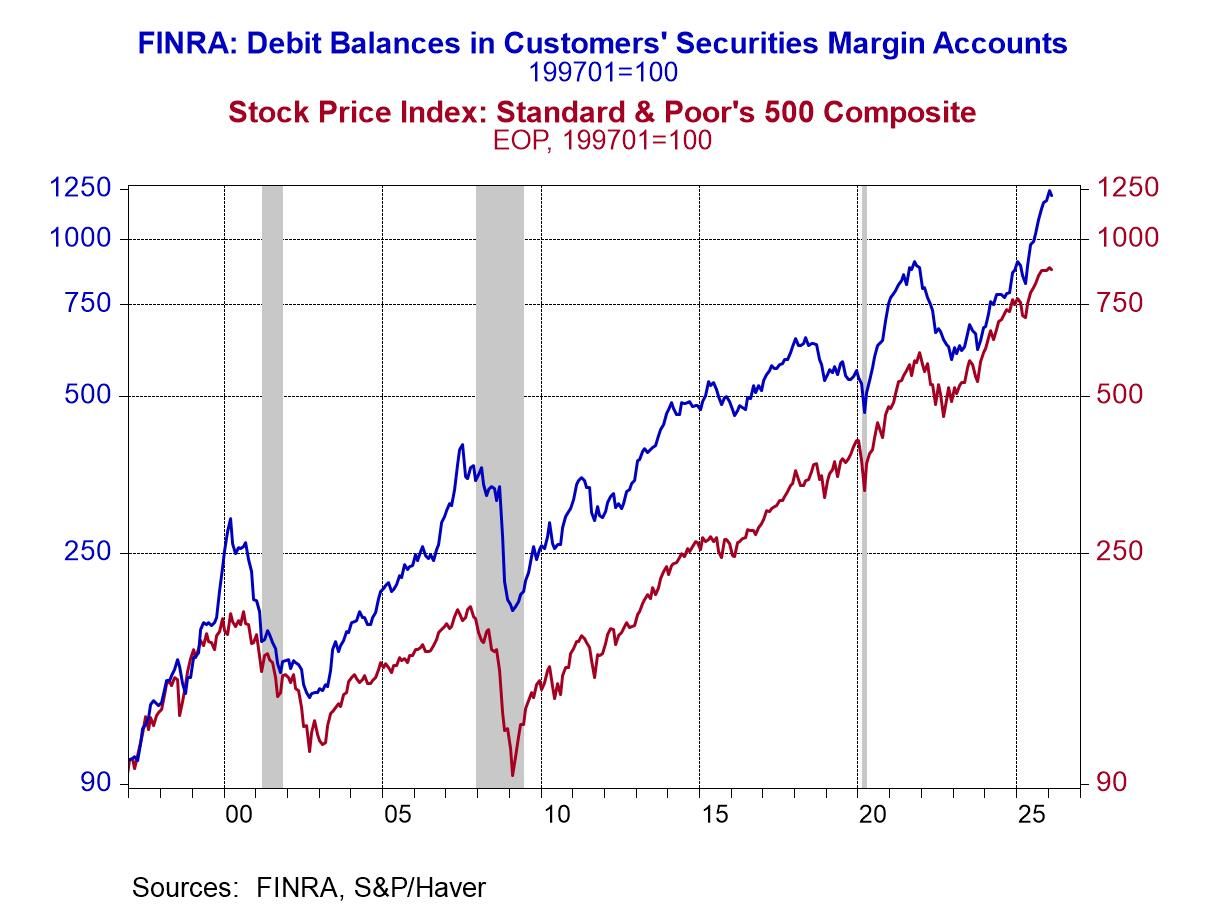

Plotted in Chart 2 are the end-of-month indices of debit balances in securities margin accounts and the S&P 500 stock index. The plot is in semi-log scale, which means that the slope of a line represents percent change. The February 2026 value of the debit balance in margin accounts is just off a record high.

Chart 2

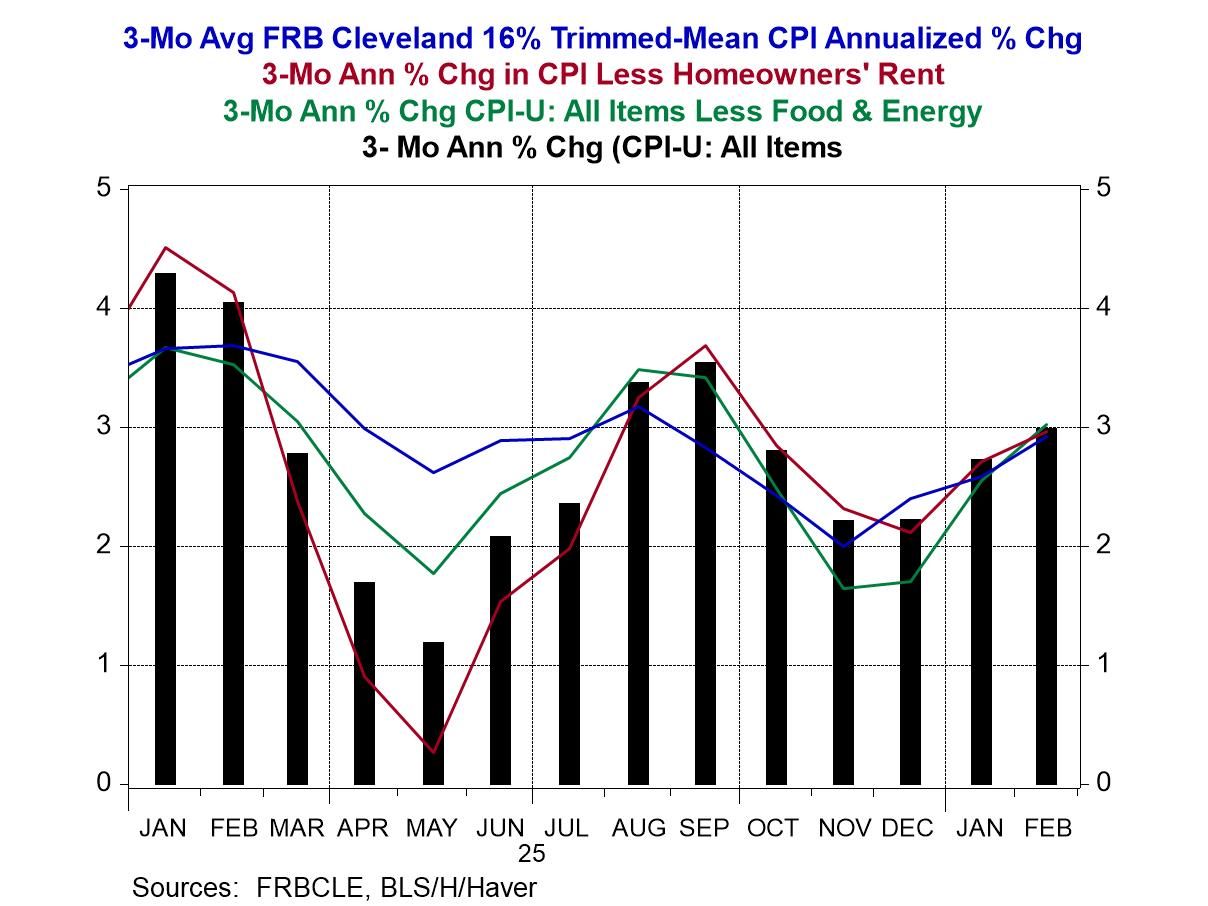

Now, just because these data series are at or near record highs certainly does not mean that they are at their cyclical peaks. But when things reach extremes, my congenital pessimism kicks in. What if the Fed’s next move is to increase the federal funds rate, rather than to cut it? Why might this be so? Because, as shown in Chart 3, no matter how you slice it or dice it, as of February 2026, the 3-month annualized rate of CPI inflation was 3%, not 2%. And this was before the prices of crude and refined petroleum products spiked higher in recent weeks. Even if the spike in energy prices is temporary, it will impart an upward bias to the CPI excluding the usual subjects.

Chart 3

If the market were surprised by a Fed interest-rate hike this year, the equities market would likely sell off. The Fed would no longer be its friend. All else the same, with equities being such a large proportion of household wealth, households might have an increased appetite for deposits and money market funds. In other words, the demand for money to hold would increase (or the velocity of money would decrease), which would imply a slowing in household spending on goods and services.

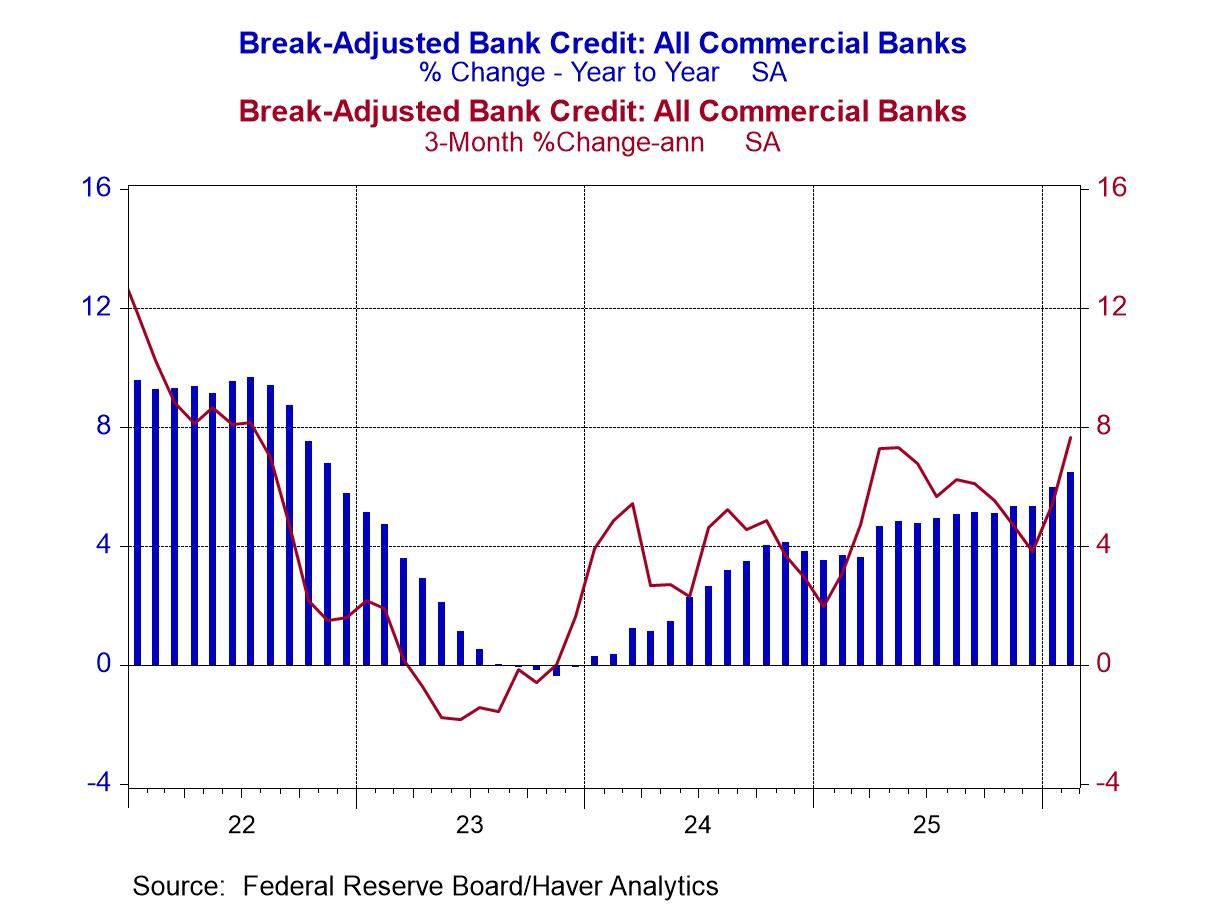

Speaking of money, more accurately, credit, commercial bank credit growth, the largest component of thin-air credit, is picking up. Year-over-year in February 2026, commercial bank credit growth was 6.46%. In the three months ended February 2026, commercial bank credit grew at an annualized pace of 7.65%. (See Chart 4.) This is the fastest growth in commercial bank credit since the inflationary days of 2022. Why would the Fed even consider lowering the federal funds rate with commercial bank credit growing solidly?

Chart 4

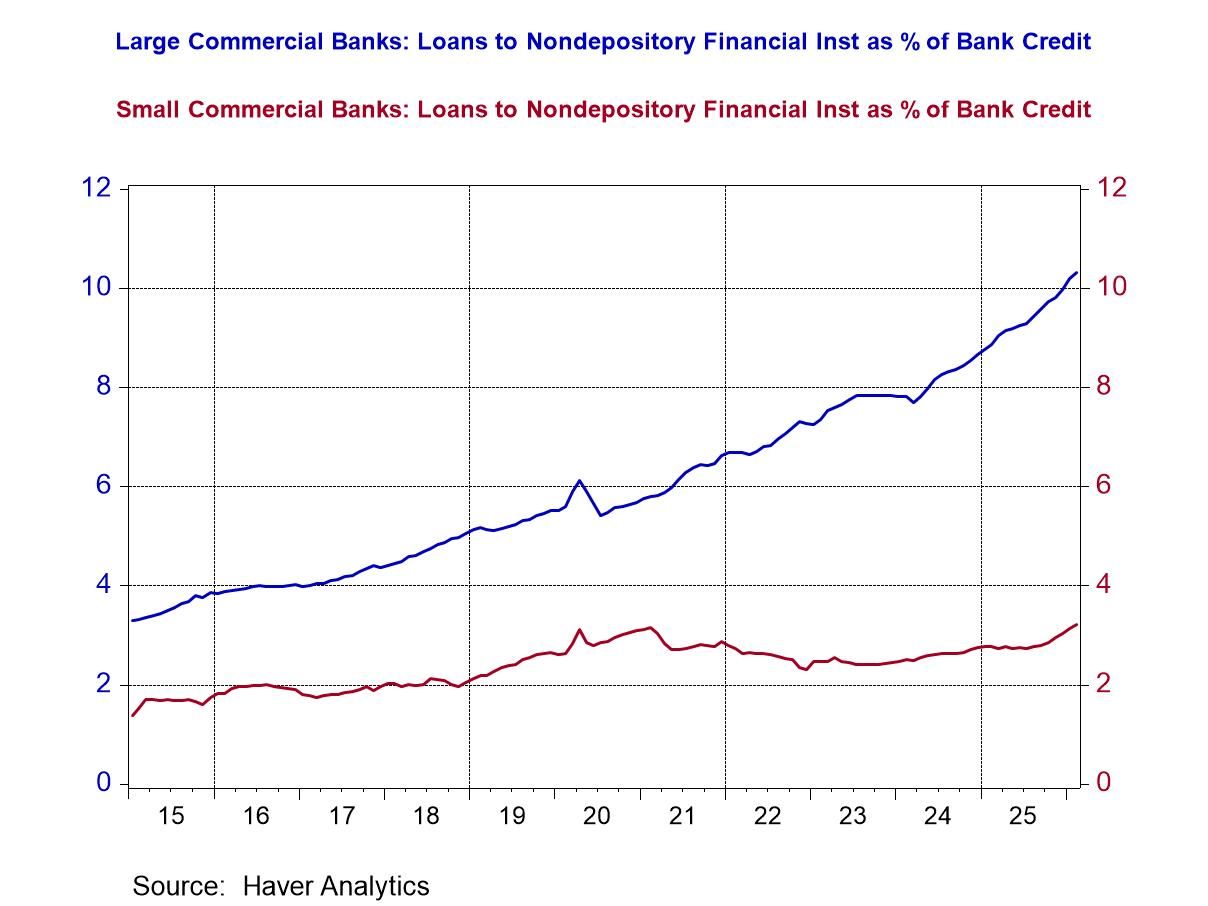

One of the categories of bank credit that is helping drive the faster growth in the total is Loans to Nondepository Financial Institutions. As can be seen in Chart 5, loans to nondepository financial institutions have been steadily rising as a percent of total bank credit for large commercial banks, especially so in the past two years. As of February 2026, these loans accounted for 10.3% of large commercial bank total bank credit, but only 3.2% for small commercial banks. What might these loans to nondepository financial institutions be for? My bet is that large banks are trying to get into the private-credit lending game indirectly by funding the institutions that are directly lending in the private credit market. In recent months, credit-quality problems have emerged in the private credit market.

Chart 5

At the same time that large commercial banks have greater exposure to a deteriorating private credit market, the Fed’s Vice Chair of Supervision, Michelle Bowman, is recommending that capital requirements be relaxed for large commercial banks. (As an aside, Ms. Bowman’s banking experience consists of six years as a vice president and director at her family’s bank, Farmers & Drovers Bank, where she was involved in compliance and trust activities. Farmers & Drovers Bank is located in the thriving metropolis of Council Grove, Kansas, which has a population of 2,101 folks. The bank, which had total assets of $219.7 million as of 01/30/2026, is renowned for its building, constructed in 1892 and now listed as a U.S. National Historic Place. Subsequent to Ms. Bowman leaving the historic Farmers & Drovers Bank, she was nominated in late 2016 by then Kansas Governor Sam Brownback to become the Kansas banking commissioner, presumably because of the banking acumen she gained at the family-owned Farmers & Drovers Bank. In April 2018, President Trump nominated Ms. Bowman to fill the Federal Reserve Board of Governors seat vacated by MIT economics PhD Stanley Fischer.) Relaxing capital requirements of large commercial banks at a time of developing credit-quality problems in an estimated $3 trillion market reminds me of the 1999 repeal of the Glass-Steagall Act. What could go wrong? But again, I am a congenital pessimist.

Paul L. Kasriel

AuthorMore in Author Profile »Mr. Kasriel is founder of Econtrarian, LLC, an economic-analysis consulting firm. Paul’s economic commentaries can be read on his blog, The Econtrarian. After 25 years of employment at The Northern Trust Company of Chicago, Paul retired from the chief economist position at the end of April 2012. Prior to joining The Northern Trust Company in August 1986, Paul was on the official staff of the Federal Reserve Bank of Chicago in the economic research department. Paul is a recipient of the annual Lawrence R. Klein award for the most accurate economic forecast over a four-year period among the approximately 50 participants in the Blue Chip Economic Indicators forecast survey. In January 2009, both The Wall Street Journal and Forbes cited Paul as one of the few economists who identified early on the formation of the housing bubble and the economic and financial market havoc that would ensue after the bubble inevitably burst. Under Paul’s leadership, The Northern Trust’s economic website was ranked in the top ten “most interesting” by The Wall Street Journal. Paul is the co-author of a book entitled Seven Indicators That Move Markets (McGraw-Hill, 2002). Paul resides on the beautiful peninsula of Door County, Wisconsin where he sails his salty 1967 Pearson Commander 26, sings in a community choir and struggles to learn how to play the bass guitar (actually the bass ukulele). Paul can be contacted by email at econtrarian@gmail.com or by telephone at 1-920-559-0375.