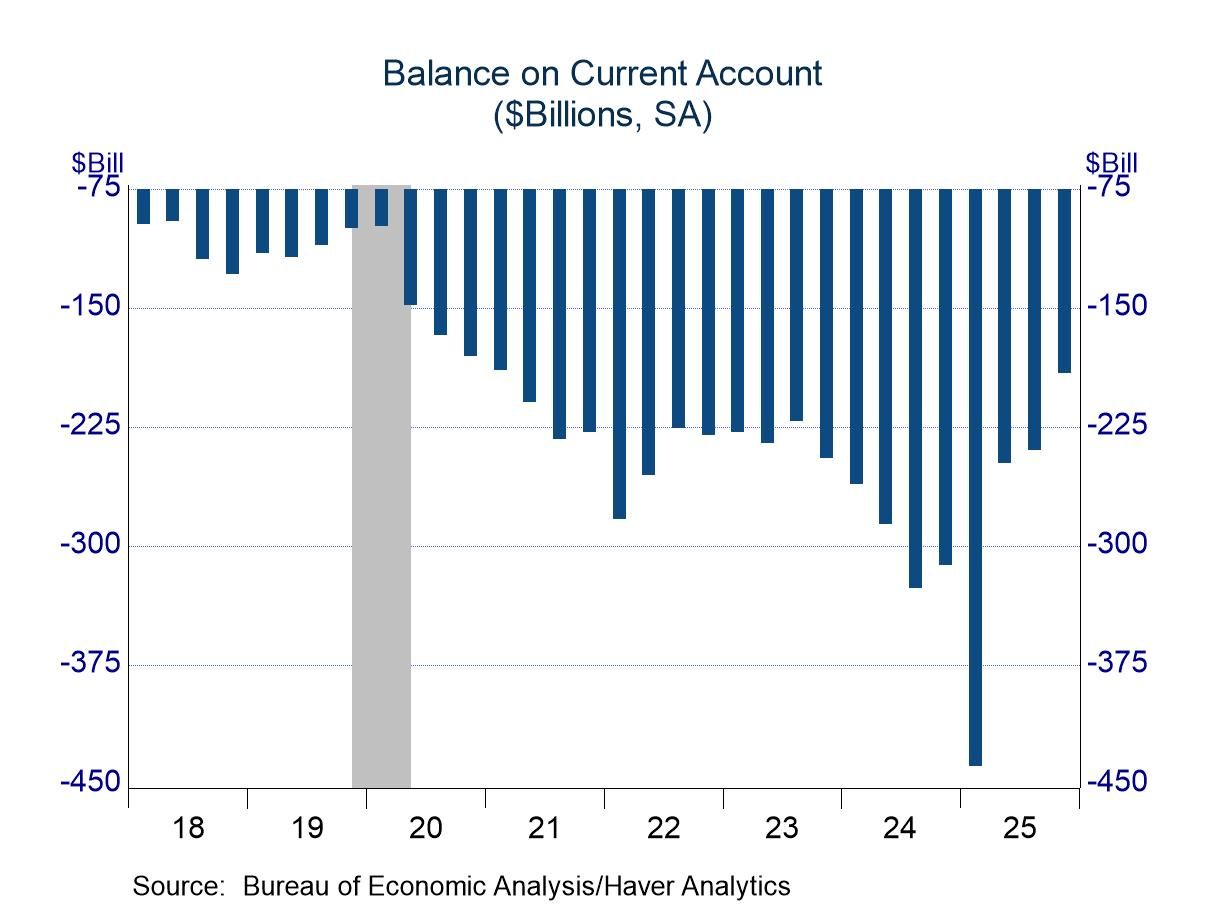

Current Account: Notable Improvement in Q4

Summary

- Firm exports boosted the trade component.

- Primary income flows rebounded from soft showings in prior quarters.

The current account measures the economic interactions of the US with foreign economies. It could be viewed as a cash flow statement, showing receipts into the US economy and payments to foreign entities. Two broad categories are involved: trade in goods and services and income flows.

The US typically runs a deficit in the current account, registering a shortfall in every quarter since 1991-Q3; it last recorded an annual surplus in 1981. Current account deficits moved to striking levels the past two years, although the results were less alarming when measured as a share of GDP (4.0% in 2024 and 3.6% in 2025 versus the record of 5.9% in 2006). Moreover, hints of improvement have emerged recently.

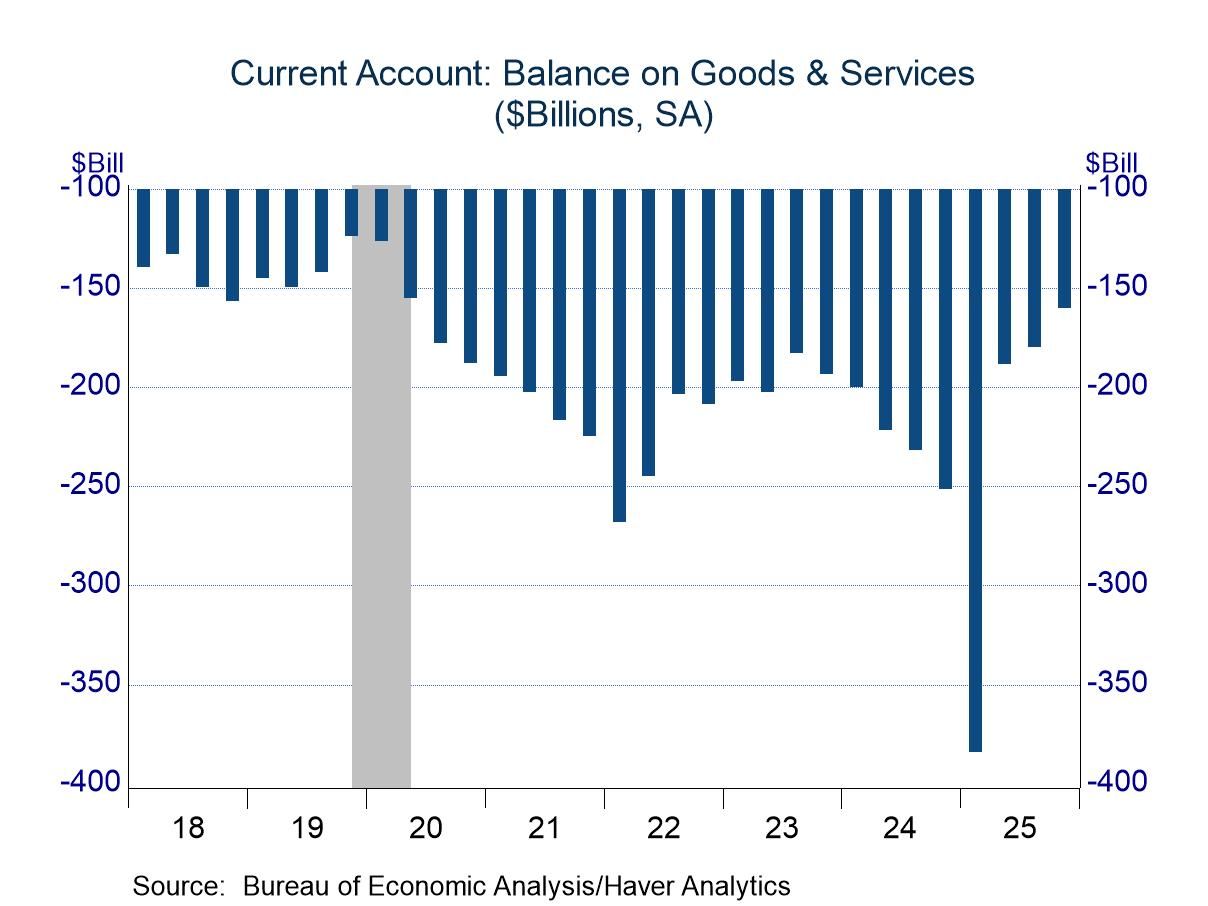

Last year involved considerable volatility in the trade portion of the current account, as President Trump’s tariff threats led to a burst in imports in Q1. The import surge was largely offset in the second quarter, leading to a narrower deficit, but the trade shortfall continued to improve in the third and fourth quarters. Dips in imports of goods in the third and fourth quarters suggest some residual offset to the Q1 increase, but solid growth in exports throughout 2025 after slow results in 2024 suggested that fundamentals might be turning in favor of the US. By the fourth quarter, the deficit in goods and service trade was not far out of line with readings before the pandemic.

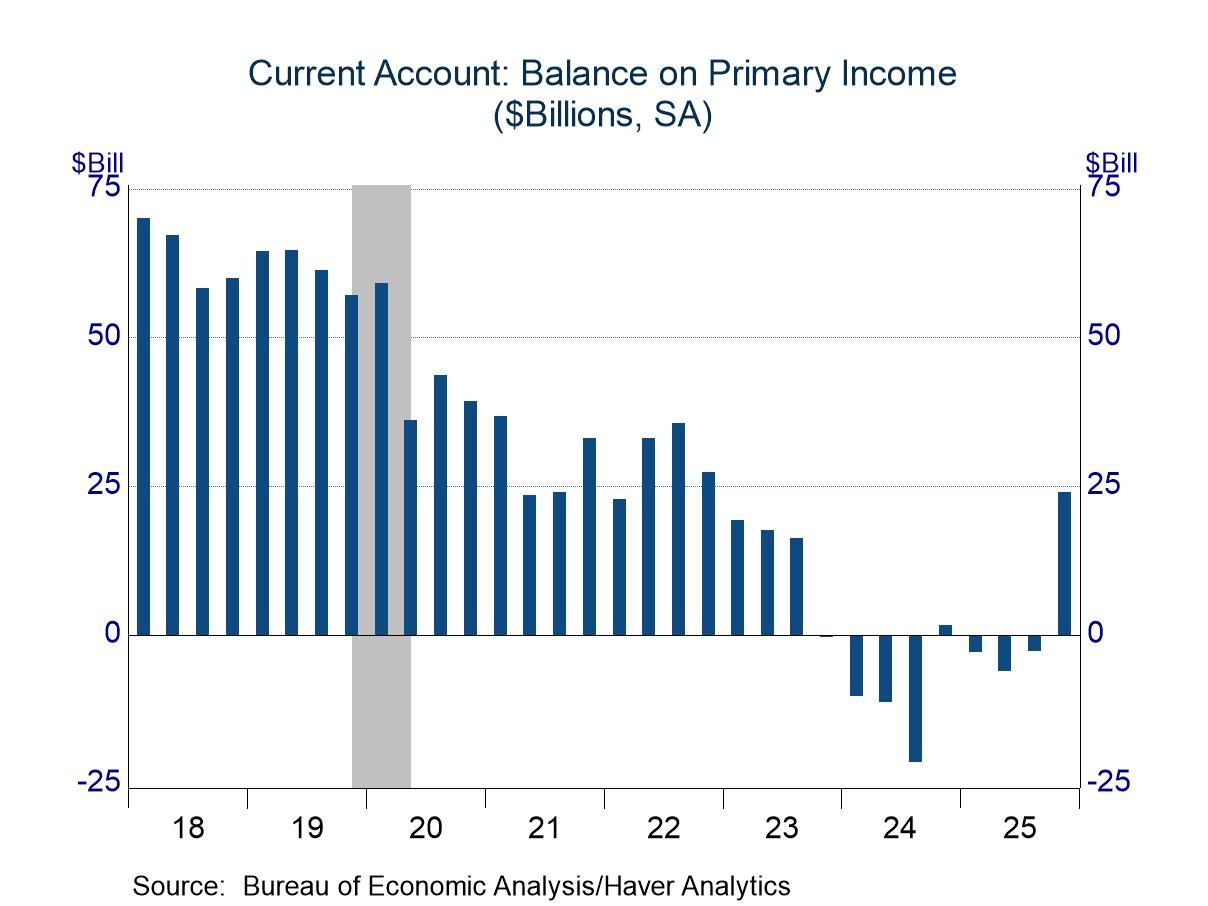

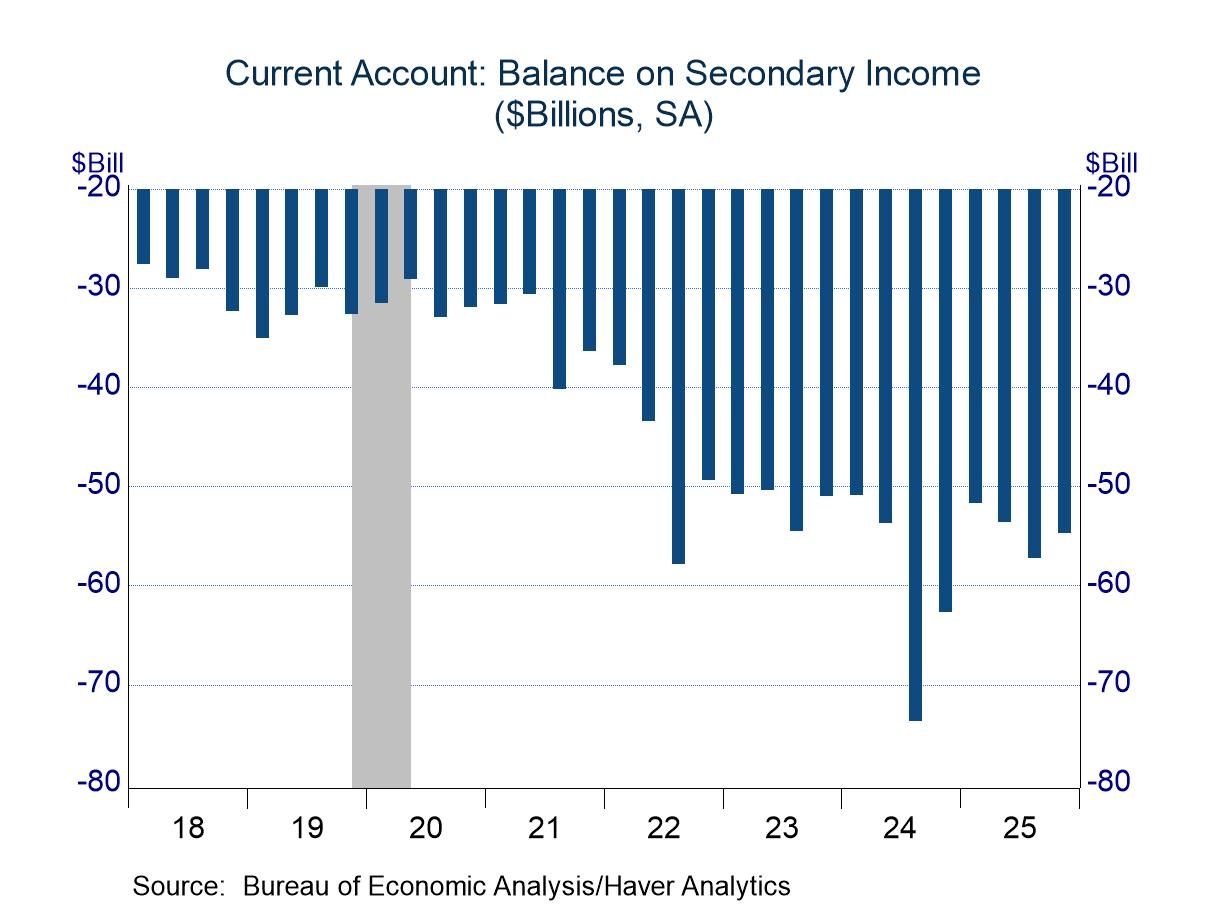

The income portion of the current account also showed signs of improvement in the fourth quarter. This section of the current account has two subcomponents: primary income and secondary income. Secondary income covers transfer payments, which are advances for which no goods or services are received in return for the outlay. Examples include personal remittances, pension payments (including Social Security), casualty insurance settlements, and charitable donations. Secondary income flows changed little in Q4.

However, primary income flows jumped in the final months of last year. Historically, the US registered a healthy inflow of primary income, which includes investment income, labor compensation, and miscellaneous items. Primary income, led by the investment component, began to soften around the time of the pandemic, and it moved into negative territory during much of 2024 and 2025. The fourth quarter, though, brought a notable rebound, pulling it into the plus column. The improvement was the result of returns on direct investment rather than on portfolio income, and the new total was far above other recent readings. One wonders about random volatility or a one-time gain, but for now it represents a welcome development.

Balance of Payments data are in Haver’s USINT database, with summaries available in USECON. The expectations figure is in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

Global

Global