Global| Mar 19 2019

Global| Mar 19 2019ZEW's Global Assessments Remain Weak

Summary

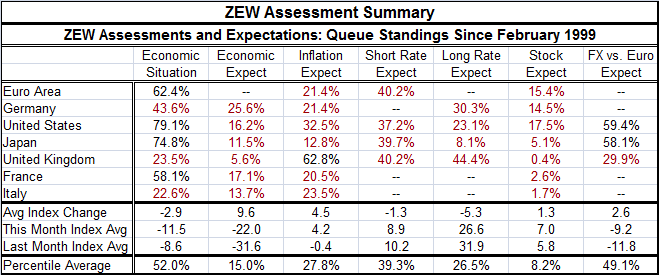

ZEW survey expectations curled higher this month but continued to stake out very weak readings. The average ZEW expectation change (unweighted) for the seven countries/regions in the table is a rise of 9.6 points. Even so, the average [...]

ZEW survey expectations curled higher this month but continued to stake out very weak readings.

ZEW survey expectations curled higher this month but continued to stake out very weak readings.

The average ZEW expectation change (unweighted) for the seven countries/regions in the table is a rise of 9.6 points. Even so, the average percentile standing for these countries is a bottom 15% standing; that implies that the group has been weaker historically only 15% of the time. Despite the upward revision in expectations, the outlook from the ZEW experts is still for growth that is poor.

The economic situation generally worsened in March despite the improvement in the outlook. The economic situation fell on average by 2.9 points and carries a negative reading of -11.5. The economics situation ranks at its 52nd percentile, a reading that admits that growth is still in gear at a pace above its historic median. Four of seven members showed outright percentile standings above their 50th percentile in rank. Such a standing implies a greater than normal expansion since the median for a historic rank occurs at a standing of 50. In terms of raw scores, however, five of seven countries reported negative numbers indicating contraction while only the United States (58.2) and Germany (11.1) posted positive raw diffusion readings (The raw diffusion numbers are not presented in the table). The height of the U.S. and German diffusion numbers dragged the average percentiles above the 50 mark even though most countries/areas in the table are contracting according to their individual diffusion metric for the economic situation.

Inflation expectations actually worsened this month with an average change of +4.5 logged. Last month the average inflation diffusion reading was negative. This month it is higher by 4.2 points. But the standing of the average inflation gauge is still only in its 27th percentile. Every country, except the United Kingdom, has an inflation standing that is below its 50th percentile putting it below its historic median. However, there are still positive inflation expectations in the U.S., Japan, and the U.K. Net declines are expected in the EMU region, Germany, France, and Italy. That is the EMU and its member are all assumed to be mired in disinflation or worse while the non-EMU members the U.S., Japan, and the U.K. are expected to experience net inflation increases although only the U.K. will experience increases larger than its historic median.

Today there are some interesting developments out of Germany. First, it looks as though Germany is not going to boost its pay-in to NATO but will continue to expect the U.S. to defend it while continues to focus on running fiscal surpluses. Germany appears ready again to eschew a 2% of GDP target for spending in NATO. Meanwhile, the Bundesbank does not see a quick turnaround for the weakened Germany economy. Moreover, the panel of economics experts known as the ‘wise men' cut their own outlook for growth to 0.8% from 1.5%, a pace they had projected in November. However, the wise men do see a pick up to a pace of 1.7% next year. The German economy continues to struggle and Germans continue to push back at U.S. policy desires ranging from NATO spending, to restrictions on telephone equipment to the treatment of Iran. Germany is asserting that it will go its own way even if it has to cut off its nose to spite its face.

ZEW expectations for interest rates both short and long are lower this month. The average percentile standing for short rates is in its 39th percentile while the average percentile standing for long rates is in its 26th percentile. The relatively lower standing for long rates speaks to the flat yield curve and to the contained nature of inflation.

The lowest average percentile standing in the table is for equities. Stocks average a percentile standing of just 8.2%. Even in the U.S., where growth is the best, the stock market expectation is only in its 17th percentile. In Germany where the economic expectations are at their relative best, the stock market expectation is only in its 14th percentile. Low inflation rate and improved expectations are supportive, but in the end stocks are about growth and expected growth and those things are still too weak to impress stock market investors.

On balance, while the ZEW expectations have been lifted a bit this month, there is still a lot of weakness left in place. The sense of improvement in expectations is made insignificant by the still abysmal level and ranking of expectations overall. There may have been some small improvement in prospects in the course of the month. However, as the German outlook from the Bundesbank and the wise men remind us, conditions are still extremely challenged and not going to change fast.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief