Global| May 19 2015

Global| May 19 2015ZEW Makes Sharp Backtrack As German Job Growth Slows

Summary

The German ZEW index for May shows a step back in the current index and a sharp drop in expectations. The expectations reading fell by 11.4 points in May, marking it as a drop that has been larger only 13.5% of the time. The current [...]

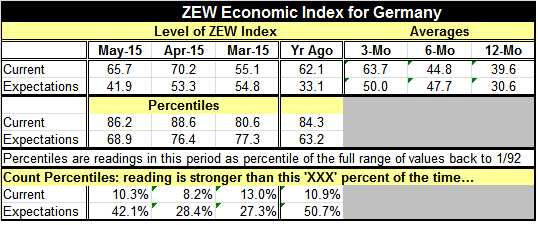

The German ZEW index for May shows a step back in the current index and a sharp drop in expectations. The expectations reading fell by 11.4 points in May, marking it as a drop that has been larger only 13.5% of the time. The current index fell by a more modest 4.5 points. The drops leave the current ZEW index in about the top 10% of its queue of data historically; still an exceptionally strong reading despite the month's set back. However, the expectations index has fallen to a position where it has been higher 42% of the time. This is still above its median value and is still a `constructive' level. However, the new level marks a much less robust standing for expectations than before.

The German ZEW index for May shows a step back in the current index and a sharp drop in expectations. The expectations reading fell by 11.4 points in May, marking it as a drop that has been larger only 13.5% of the time. The current index fell by a more modest 4.5 points. The drops leave the current ZEW index in about the top 10% of its queue of data historically; still an exceptionally strong reading despite the month's set back. However, the expectations index has fallen to a position where it has been higher 42% of the time. This is still above its median value and is still a `constructive' level. However, the new level marks a much less robust standing for expectations than before.

The chart chronicles quarterly German, U.S. and EMU employment growth since 2004. New German figures, just released today for Q1 growth, reveal the weakest German quarterly job gain since Q1 2010. Prior to this gain in Q1 2015, a gain of 21,000 jobs, the weakest quarterly growth since Q1 2010 had been 30K in Q1 2013 and 42K in Q4 2013. Over the last seven quarters, German quarterly growth had been averaging 87K to 95K. This is a demonstrable slowdown for German job creation.

Despite a still very weak euro, German job creation has slowed and the ZEW expectations index has turned sharply lower. Still, in other data released to today, we see the EMU trade surplus is widening even as import growth picks up since export growth has hit double digits. The unadjusted trade surplus in the EMU has grown from 16.1 billion euros one year ago to 23.4 billion euros in March 2015. The combination of restrained imports and faster exports has done a lot to boost EMU growth. Even so, PMI readings of the EMU and German manufacturing sectors have been well short of robust.

As the most competitive country in the EMU, we would expect Germany to be benefitting in this environment of such a weak euro. But German factories are not performing well. In fact, the German services sector is outperforming the German manufacturing sector despite the tail wind for manufacturing of a too-low exchange rate.

The ZEW financial experts rate banks, insurance companies and utilities with poor profit expectations as they have for many months. But over the last five months these ratings have gotten progressively worse. Services and telecoms have a rating rise over the period but by only small amounts. The remaining sectors have seen huge positive changes in expectations over five months. But now, in May, the worm seems to be turning. Despite some huge five month gains, profit expectations for vehicles and chemicals are turning lower along with electronics, machinery, and consumption. In May, construction, services and info-techs have held their ground. The drop in ZEW expectations has come with a parallel drop in profit expectations across a broad swath of German industry.

Perhaps against that background, it is not surprising the European Central Bank is ramping up its QE program. The ECB describes this as a front-loading of some liquidity ahead of a typically low liquidity period in the summer. Executive Board member Benoit Coeure has described this policy by saying that liquidity may also be back loaded in September when liquidity normally returns to the markets. Really? Markets have reacted as if this is a real change in policy and a speed up of QE, not as if it is merely a technical shift in liquidity provision timing. At this point, we can either take the ECB at its word or speculate that it is a disguise of a step up in QE. The change in injection strategy comes after a significant back up the bund market that put the bund curve at its steepest in five months.

As we can see, the ZEW experts, the ECB and the markets all are grappling with an increasingly uncertain future. It seems for each economic report that comes in better than expected another comes in worse. The German and EMU economies still produce ragged results. Japan, after its jump out of the gate in the wake of the announcement of Abenomics (and then after the imposition of a sales tax hike, of course), has cooled too. While U.S. job growth is still the global gold standard, recent reports suggest that growth is ratcheting down too. The problem is that none of these policies have given a lasting boost to domestic demand anywhere. And demand is still what is scarce. The problem with all the exchange rate devaluation strategies we have seen is that in this environment these policies are no more than a beggar-thy-neighbor approach to growth. A low exchange may permit a country to take more of a neighbor's domestic demand but that is zero sum economics not any global stimulus. And that is the problem. Even in the EMU, with Germany as the best performing economy, Germany's performance has not done much to spread growth to the rest of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief