Global| Nov 18 2014

Global| Nov 18 2014ZEW Index Steps Back from the Brink

Summary

Germany's ZEW index for November saw its expectations component rise to 11.5 from -3.6 in October. The current index remained at a low level of 3.3, barely higher than a 3.2 reading for October. Since the previous ZEW release, Germany [...]

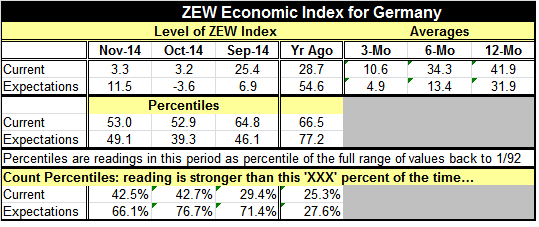

Germany's ZEW index for November saw its expectations component rise to 11.5 from -3.6 in October. The current index remained at a low level of 3.3, barely higher than a 3.2 reading for October.

Germany's ZEW index for November saw its expectations component rise to 11.5 from -3.6 in October. The current index remained at a low level of 3.3, barely higher than a 3.2 reading for October.

Since the previous ZEW release, Germany reported a positive GDP number for the third quarter. The recent fears that GDP could put in yet another negative quarter of growth were put to rest. In fact, the numbers for all of the European Monetary Union were slightly firmer than had been expected.

The sharp snap back in expectations by the ZEW financial experts is reassuring, not definitive. The 11.5 reading for November stands higher than its November reading fully 66% of the time, marking the November reading as on the borderline of the bottom third of its historic range. The current index is higher 42.5% of the time, marking it as above its historic median but hardly as strong.

The current expectations reading is one the weakest we have seen in some time from the ZEW respondents if we take the November in October figures together. To see the pair of responses as weak or weaker, we have to go back to the end of 2012.

ZEW experts have upgraded their outlook for stocks, however. Of the 13 stock sectors that the ZEW financial experts rate, only two of them were downgraded in November compared to October. The ZEW experts are somewhat more upbeat on the equity market potential for earnings than they were one month ago. The average reading for equities is only about a 54th percentile standing meaning that the rating is just a few points higher than the midpoint of the historic range that the ZEW financial experts have attached to equity ratings historically.

In other economic reports released today, there was some good news for Europe. European car sales accelerated. U.K. house prices also accelerated and Italy's trade account swung to surplus on its current account measure.

Still, the fate of Europe is not yet sealed nor was the fate of Europe or Germany, for that matter, saved by the last round of better-than-expected Q3 GDP reports.

Europe is still hostage to bad geopolitical news and on that front things appear to have worsened. Tuesday NATO Secretary General Jens Stoltenberg denounced what he termed a serious Russian military buildup both inside Ukraine and on the Russian side of the border. He urged Moscow to pull back its troops. Ukraine's President Petro Poroshenko said his country is ready for "total war" with Vladimir Putin's forces. These hardly are encouraging developments.

It is hard to tell how much of this talk is tough talk or mere hyperbole. But the risks in Ukraine are serious. Russia has been supplying the rebels and NATO continues to chastise Putin who continues to act as though modern surveillance is clueless about what he is doing. Putin attended the G-20 summit where he lied through his teeth about his actions in Ukraine. Everyone knows what is going on and that Putin continues to lie about it. None of this can be good for the potential for a diplomatic solution. We continue to believe that the more Russia's economy is hurt by economic sanctions the more it will want to get as its prize for its suffering. We see Ukraine at risk to Putin and we see the West as having done little to shore up Ukraine. Arguably Putin's denials have bought him time to amass his forces for an invasion. The West acts as though diplomacy will work. If it does not, the West has no fallback position. Righteous indignation will not help the people of Ukraine.

If Geopolitics continues to heat up, we think economic trends will again be put at risk. It's why we do not see the Q3 GDP reports from Europe as particularly reassuring, unlike the ZEW financial experts.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief