Global| May 14 2013

Global| May 14 2013Zew Index Notches Down the Heat as Pew Poll Turns it Up

Summary

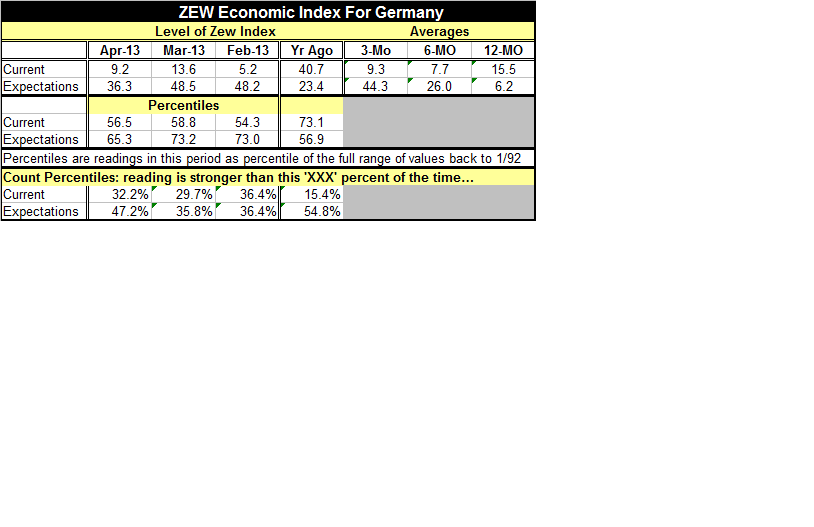

The Zew index that surveys financial experts in Germany moved lower in April compared to March for both its current and its expectations readings. The current reading notched down to a 9.2 net reading from 13.6 in March. The [...]

The Zew index that surveys financial experts in Germany moved lower in April compared to March for both its current and its expectations readings. The current reading notched down to a 9.2 net reading from 13.6 in March. The expectations reading notched down to 36.3 in April from a level of 48.5 in March. These are substantial moves in the monthly indices but how significant are they?

The Zew index that surveys financial experts in Germany moved lower in April compared to March for both its current and its expectations readings. The current reading notched down to a 9.2 net reading from 13.6 in March. The expectations reading notched down to 36.3 in April from a level of 48.5 in March. These are substantial moves in the monthly indices but how significant are they?

The percentile readings at the bottom of the table give us a way to assess how different the monthly metrics really are. In the case of the 'current conditions' index it is stronger than its April reading 32% of the time whereas it was stronger than its March reading about 29% (nearly 30%) of the time. These are not vastly different assessments. For expectations: expectations are stronger than their April level 47% of the time while compared to March levels, expectations are stronger only about 35% of the time. The drop in the expectations metric is more significant.

With expectations stronger than this about 47% of the time, we are also saying that the expectations metric is pretty near its median value (where that reading would be 50% instead of 47%). Meanwhile, the current index is relatively stronger even though its level seems to be relatively weaker. In fact the average reading for the current index is negative at -22.2 (its median is -20.8). For expectations the average reading is 25.5 (its median is 23.4). You can understand the differences in the relative positions of the two readings a lot better after seeing what the readings are for the two series' averages/medians. At first blush one would think that the expectations series is stronger. Its absolute number is higher but, in fact, it is at a much weaker position relative to its own history and tendencies.

What the Zew index tells us is that current conditions remain fairly strong while expectations have moved from what has been a consistently strong position to one that is considerably more neutral as conditions in the Zone continue to be touch-and-go. The table shows that current macroeconomic conditions have moved up very sharply as the financial crisis abated and recession was put behind the global economy; that reading has been gradually, but not completely steadily, moving lower. Expectations moved up sharply very early in the process of recovery and then as current conditions improved sharply expectations declined. This is (in some sense) nearly automatic because the closer the current conditions get to '100' (or the best that they can be) the more likely that expectations for the future have to diminish since there so little room for improvement. Still, as current conditions began to erode, expectations began picking up although expectations still have not gotten back to a level that is particularly strong. We regard expectations currently as somewhere between 'firm' and 'normal.'

The recent G7 meeting seems to have shifted the balance in Europe away from its focus on austerity. Austerity has not been jettisoned, but the G7 directive mentions that countries will be trying to balance their need for austerity against an agenda for growth. That's an easier sentence to write than it is a thing to do.

A recent Pew study has found that the contrast between how Germans see Europe and the rest of the European Community sees Europe is quite stark --

- For example, Germans feel better about the economy by about 66 points more than the EU median.

- Germans feel better about the personal finances by about 26 points more than the EU median.

- Germans feel better about the future by about 12 points more than the EU median.

- Germans feel better about the European Union by about 17 points more than the European Union median.

- Germans feel positive about European integration by about 28 points more in the European median.

- And the Germans feel better about their own leadership by about 48 points more than the European median study.

Against that backdrop, not surprisingly, the Pew study also reports that, "No European country is becoming more dispirited and disillusioned faster than France."

Anyone who pays the slightest attention to European economic statistics is well aware that the performance of the German economy is quite a bit different and quite a bit better than most other economies in the European Union and in the European Monetary Union. However, whenever analysts say that the imbalances in the Union are too big, too burdensome, too difficult, or too painful to fix, they are told that they miss the salient point which is that these Unions are political unions, as much if not more than, economic unions. They have been constructed to create political stability within Europe. And so maybe a non-European, like myself, misses the boat in looking at numbers and making decisions about what they mean. And maybe not... The numbers reflect real differences and point at some tough decisions that need to be made and keep getting put off.

Meanwhile, those who assert that Europe is a political union, constructed for political stability, need to confront the fact that the union has been destabilizing economically and it has stoked conflict and animosity among its members rather than having given them a sense of common purpose.

At some point this European view of the European Monetary Union as a political entity will have to confront the reality that The Union as it exists has increased intra-European tensions and conflicts. It has brought several member states at opposite ends of the feel-good economic spectrum into direct conflict and has fanned the flames of discontent and of resentment.

This may be a normal part of the growing together process, analogous to what an ordinary individual might experience in his or her adolescence, on the way to being a reasoning adult. But Europe has yet to deal with this in a reasonable way or to express how it is going to solve its panoply of economic problems that scatter across the zone, problems that are made more difficult to solve because of the countries being in a common currency area. .

The G7 meeting seems to be saying that the age of austerity is over. This was certainly not the German view coming into that meeting nor, I suspect, is this the German view now. Formally, austerity has not been jettisoned, but once it has been diminished we are in a different part of the game. And the countries experiencing austerity still have a long way to go. If they let up now it's not clear if they will stay on the path or go back to their old ways. It certainly is true that they are in dire need of more growth. But they are still in need of policies of temperance when it comes to their government spending. And they are need of substantial fixes in the private sectors to remedy competitiveness deficiencies. If the dose of austerity is to be cut what medication will take its place? Growth is good for health but by itself does not replace what austerity does.

I continue to contend that currency devaluation is the best and most efficient way for these countries to restore their competitiveness. But of course, if the Zone stays together this will not happen. The Pew study may be useful in getting Europeans to actually look at what their system is doing to them rather than to keep them focused on the ideal of what they might be. Can they simply 'tough-it-out' to get there? Or, do they need some further period of attitude readjustment to go their own way for a while?

It's entirely possible for the Zone to be deconstructed and then reconstructed. And that may be a more likely result than to think that countries that have left the path of hard-core austerity will continue to stay close enough to it to eventually solve their problems. But that's essentially what the judgment is for the future of the e-Zone.

I keep calling this the age of denial. Europe is in denial about the nature of its problems. The US is in denial about its need to grapple with its runaway future entitlements; and it's not alone in that. China and other countries that have leaned on their export-led growth strategy fueled by currency manipulation have been in denial about how their strategies, while successful for them, a put other nations in a more precarious position and created blow-back for them. All of these denials are leading these countries to pursue policy changes to fix what they have denied was wrong.

Denial is a coping mechanism it is not an economic strategy. And as a coping mechanism it may lead a country or a region to be able to continue to operate and to move in a certain direction long after it has become unwise to do so. And, in that sense, the use denial is also a decision (tacit or otherwise) to make things worse. Kicking the can down the road is simply an excuse for not bending down, picking it up, and disposing of it and its problem immediately.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief