Global| Feb 18 2014

Global| Feb 18 2014ZEW German Expectations Back Off

Summary

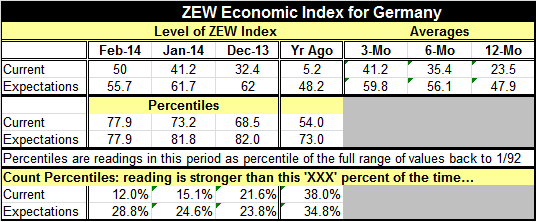

The ZEW German index for February shows a significant climb in the current index as expectations were set back for the second month in a row, this time substantially. The current index rose to 50 this month from a level of 41.2 in [...]

The ZEW German index for February shows a significant climb in the current index as expectations were set back for the second month in a row, this time substantially. The current index rose to 50 this month from a level of 41.2 in January. Expectations fell to 55.7 from 61.7. While the economy continues to improve, expectations are starting to be pulled back. This is not a good development.

The ZEW German index for February shows a significant climb in the current index as expectations were set back for the second month in a row, this time substantially. The current index rose to 50 this month from a level of 41.2 in January. Expectations fell to 55.7 from 61.7. While the economy continues to improve, expectations are starting to be pulled back. This is not a good development.

The current index and the expectations index each, coincidentally, sit at the 77.9 percentile of their respective high-low ranges. However, looking at the current and expectations index levels as a percentile in their respective historic queues, we find that the current index is higher only 12% of the time; expectations are higher about 28% of the time. On this metric, the current index is relatively stronger than the expectations index.

German financial experts continue to give pause and to offer a negative outlook reading on bond investing. However, the reading for February is slightly less negative than it was in January, but it is still worse than the assessment from December. In fact, excepting the January reading, the bond rating by Germany's financial experts was last weaker in February 2013.

As for the stock market, ZEW financial experts reduced the outlook for stocks every single sector except for info-tech in February compared to January.

The encroaching weakness in expectations has its roots in concerns about the likelihood of better growth in the European Monetary Union. While, just last week, the EMU region posted a positive GDP growth statistic, the gain in GDP was weak. The outlook continues to be for challenging times.

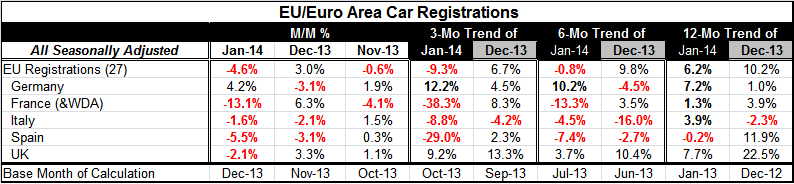

We can show some of the reason for the German uneasiness in the behavior of automobile registrations in Europe just reported today.

Auto registrations, that had been moving up so nicely, took a substantial step lower in January. German registrations alone among the large countries of the European Union (EU) moved higher in January. German registrations advanced by 4.2% month-to-month compared to an overall EU loss of 4.6%.

Registrations in Germany are up to 7.2% year-over-year ahead of the 6.2% figure for the whole of the European area. However, for Germany, the gain compares to a 1% year-over-year increase in December whereas for the EU figures show that 6.2% year-over-year gain in January compared to December's reading when that gain was 10.2% higher year-over-year. Germany improved its year-over-year gain in January while the EU saw a setback.

In January, auto registrations in France fell 13.1%, in Italy they fell 1.6%, in Spain they fell 5.5%, and in the UK they fell by 2.1%.

Year-over-year figures for the other countries show that France has registrations up by 1.3% over 12 months in January compared to 3.9% in December. Despite its monthly drop, Italy's year-over-year registrations have improved, showing a gain of 3.9% instead of the drop 2.3% reported in December. Spain's registrations in January were down by 0.2% over 12 months but had been up by 11.9% over 12 months back in December. The UK's auto registrations are strong with 12 month gains of 7.7% year-over-year, but that is much weaker than year-over-year gains which were up by 22.5% in December. In addition, all countries in the table show negative growth rates over 3-months and 6-months except Germany, of course. Germany is doing fine; it's the rest of the euro area where conditions are worrisome. That is reflected in the ZEW survey, especially in the outlook.

Despite the fact that the euro area is turning a corner in terms of the growth, substantial challenges remain. Various member countries are traveling at different speeds and their economic needs are diverse. Still, the European monetary system allows for only a single monetary policy. Although there still are separate fiscal policies, generally the countries that need the stimulus the most are still under pressure to reduce government spending and fiscal deficits.

The situation in Europe continues to be in a state of flux. Weather has been battering the US and Europe. The UK has experienced unusual amounts of rain and flooding. Weather is undoubtedly one culprit in Europe's weakness. But ongoing weakness and the inability to draw from the European Union's strengths in the realm of fiscal policy are hampering greatly the European recovery. It's fair to say that past mistakes are a separate issue in that under the Union some great and persistent inflation differences built-up in the euro zone leaving it with an uneven playing field for its members when it comes to competitiveness. The Union may have gotten exchange rates right when the Union was formed, but subsequent inflation differentials within the very union itself have undermined that initial achievement. Europe still has a long ways to go. The European Monetary Union may have escaped a lethal attack but it is still besieged. This time the danger is not a battering ram at the gates but termites in the woodwork. The Union needs to amend its structural relationships and put the whole of the Union on solid footing, not just Germany.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief