Global| Mar 18 2014

Global| Mar 18 2014ZEW Expectations Take a Geopolitical Hit as EU Car Sales Zoom

Summary

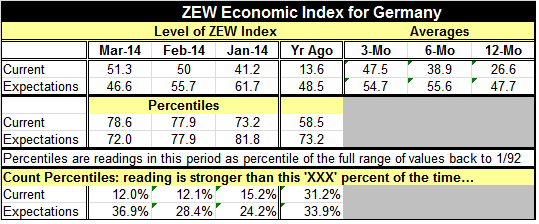

In the wake of off-putting geopolitical news in Crimea, the ZEW German expectations index for March fell sharply to 46.6 from 55.7. Its current component continued to advance but did so very slowly. The current index moved up to 51.3 [...]

In the wake of off-putting geopolitical news in Crimea, the ZEW German expectations index for March fell sharply to 46.6 from 55.7. Its current component continued to advance but did so very slowly. The current index moved up to 51.3 from 50.0 after jumping nearly nine points the month before.

In the wake of off-putting geopolitical news in Crimea, the ZEW German expectations index for March fell sharply to 46.6 from 55.7. Its current component continued to advance but did so very slowly. The current index moved up to 51.3 from 50.0 after jumping nearly nine points the month before.

Assessing these two indicators in the context of their past performance, we find the current index is stronger than its March level only about 12% of the time while expectations are stronger than their March reading about 37% of the time. The current index's proportionate standing is about the same as it was in February. But for expectations there is a substantial shift as the February reading had been higher only 28% of the time. The setback in expectations has taken the expectations reading much farther down the queue of historic experience. Both measures one year ago were in the low 30th percentiles of their respective ranges. Compared to that, the current situation is much stronger; because of a large one-month slip, expectations are weaker.

Increased wariness by the ZEW survey participants shows itself in their expectations for the stock market. In the previous months, sectors have broadly been improving. But in February ZEW participants saw improvement in only one of the sectors compared to their previous assessment while in March there's improvement in only four sectors among the 13 sectors that the ZEW participants assess.

While the ZEW index is definitely upbeat and while the expectations and the current indices each are substantially above historic averages and medians, there is also a significant backtracking in expectations for March that is a warning for the future.

So far, the sanctions over its incursion into Crimea being imposed on Russia by Europe and the United States are targeted more toward key individuals in the Russian economy. But the ruble has fallen. The Russian stock market is well off its peak. The Russian economy shows signs of floundering and most experts are looking for recession by around midyear. There could be further knock on effects from this possibly even including further moves by Russia that could complicate or darken the outlook - or broaden the geopolitical conflict. We are still in the early stages of this situation and it's still difficult to tell exactly how far it will go. The recent rhetoric from Russia is that Crimea is part of Russia it always has been and now it will continue to be such. The rhetoric from the US, at least, is that Russia needs to pull back from this act. While the Russian economy is taking this badly, the actions by the West in terms of sanctions so far are relatively tepid.

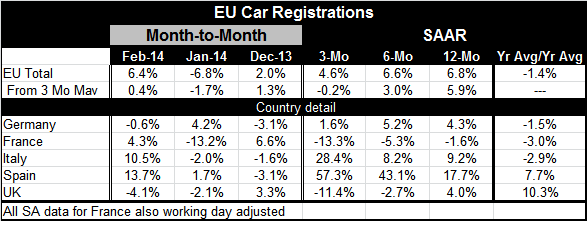

However, as the chart shows, as the ZEW index begins to pull back, auto registrations and sales in Europe have begun to solidify. In all of the European Community, growth rates are positive over three months, six months and 12 months. Although growth rates on the same horizons calculated from three-month moving averages show a slight dip over the recent three months, that take on growth is encouraging as well.

All the countries in the table except Italy and France have year-over-year auto sales improving in all months since October of last year. Italy shows a string of improving car sales that is only two months long. While France's string of car sales improving goes back to October 2013, like the rest of the countries in the table, except it has posted a year-over-year decline for its newest figure in February. The UK has been the leader of auto registration trends. UK registrations have grown year-over-year in every month since March 2012. However, the UK may be losing momentum. Its most recent year-over-year gain is only 4% which is low compared with the past string of increases. In addition, it's showing a decline over six months and an accelerated decline over three months. Those trends possibly indicate that UK car sales and registrations are going to stop driving growth the way to have in the past.

The ZEW data for Germany and the car registration data for Europe underline some mixed trends in the EU. The car registration trends show us that there has been ongoing improvement in this important consumer durable item. Furthermore, these trends show that improvement has been spread to some extent across the EU. While the ZEW figures show us that the German economy is still performing well and its current conditions are still among some of the best that the German economy has seen, expectations have fallen rather sharply. These expectations are still at a relatively healthy level; however, when expectations undergo a significant drop, it's always a good time to take pause and to reassess.

Events in Crimea are a risk for the European economy. Much has been written about the codependence of Europe and Russia on energy sales. Russia needs the revenue and Europe needs the energy. It may be that because of these two equal and opposite needs the energy will continue to flow. However, some European countries also have Russia as an important counterparty in trade. For them, there will be knock-on effects from Russia's ongoing slowing and its likely fall into recession later this year. Europe is already in a rather delicate situation with its recovery having taken hold but not taking hold with the vigor that it has had historically. Variations within the European Monetary Union further complicate the task of setting monetary policy and of keeping recovery in gear. The situation in Crimea complicates an lready somewhat fragile situation. Stock markets to date are mostly oblivious to the risks.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.