Global| Aug 11 2020

Global| Aug 11 2020ZEW Expectations Head for the High Ground

Summary

ZEW expectations have been high for several months. They were last negative in March then swung about 75 points in one month to hold to a positive reading in April. Despite different country and area experiences, the positive readings [...]

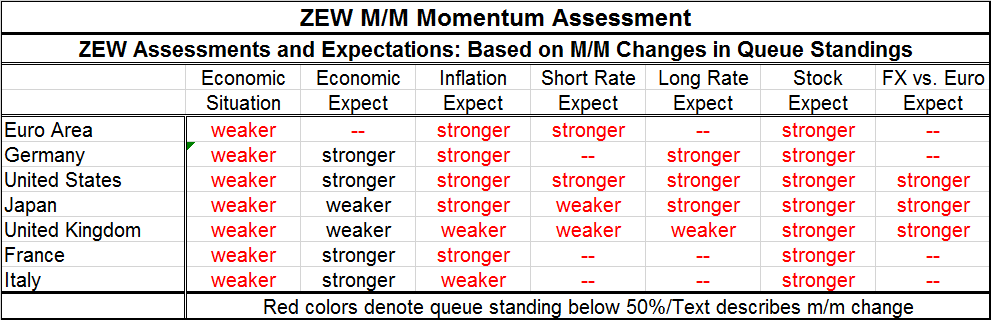

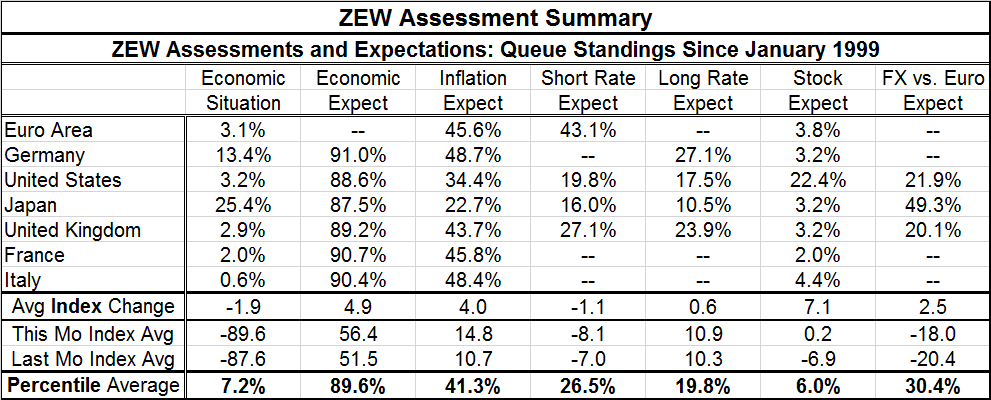

ZEW expectations have been high for several months. They were last negative in March then swung about 75 points in one month to hold to a positive reading in April. Despite different country and area experiences, the positive readings roughly doubled from April to May then rose by about 10 points or so (more or less across the board) in June. July saw a setback but now August sees a jump that is the largest for Germany while other metrics tend to show a simple advance in August. Japan and the United Kingdom are exceptions with some August backtracking; despite that, all expectation queue standings are in the top 87th percentile or better of their respective historic queue of values by country or region. That is an impressive result. And the color coding in the table below shows us that these are the only metrics in the summary table with standings above their 50th percentile that marks the median of the range for each measure.

ZEW expectations have been high for several months. They were last negative in March then swung about 75 points in one month to hold to a positive reading in April. Despite different country and area experiences, the positive readings roughly doubled from April to May then rose by about 10 points or so (more or less across the board) in June. July saw a setback but now August sees a jump that is the largest for Germany while other metrics tend to show a simple advance in August. Japan and the United Kingdom are exceptions with some August backtracking; despite that, all expectation queue standings are in the top 87th percentile or better of their respective historic queue of values by country or region. That is an impressive result. And the color coding in the table below shows us that these are the only metrics in the summary table with standings above their 50th percentile that marks the median of the range for each measure.

Expectations rose nearly everywhere as the economic situation deteriorated everywhere in August. Inflation expectations also rose broadly with the unweighted average of the various indexes rising by 4 points on the month. Stocks were the 'real mover' based on the average point change, but their average assessment is still very low. Short-term rate expectations were slightly lower on the month while long-term rate expectations were slightly higher.

But based on the percentile standings, nothing comes close to economic expectations that seem to be driving everything. Unweighted economic expectations average an 89th percentile standing with inflation expectations in second place at a 41st percentile standing. Short-term rates have an average standing in their 26th percentile with long-term rates in their 19th percentile, not far behind. The current situation and stock market have standings in their lower ten-percentile queue range. So much for the idea that stocks are forward-looking… Stock expectations are being marked to reality not to economic expectations.

In the real world, concerns about virus reinfections are real events that are intruding on policy and distorting expectations. Policy moves to help the various economies are still being implemented and formulated as this is an ongoing dynamic process. The EMU has a program that has been partly approved and is in progress while the U.S. is in the middle of formulating another jolt of assistance. And this assistance has been going on so long now that various countries and regions are seeing some political blowback even though more is clearly needed.

The novel coronavirus may still be 'novel' to scientists, but it has lost its novelty among a broad spectrum of the population. It is clear that globally economies have been impacted, unemployment has risen and continued government intervention will be called for if rioting and perhaps even revolution is to be avoided. When governments issue lockdown orders preventing people from earning a livelihood, government then takes on a unique responsibility for the care and welfare of any people affected by that approach. In the U.S., police forces (most recently in Seattle Washington) are being 'defunded' and rioting (last in Chicago) is again in train. There is rioting in Belarus over what are allegedly cooked books in an election. People are not rioting or protesting the virus, but the virus has contributed to a compilation of cooped up anger. The spread of Coivd-19 continues to stoke fears and heighten tensions wherever it goes. The outlook remains impossible although Russia claims it has a vaccine. Does it?

The West and China are still trying to develop vaccines. Will a real vaccine be developed? Will it be effective broad and trustable enough to help the at-risk population or not? Developing vaccines is tricky business and no one knows. No expert worth his or her salt is sticking a neck out with a real opinion. This is perhaps the one place in the covid-19 world where science is sticking to the science and not meddling in the politics with statements and policies unsupported by the facts on the ground. I can only wonder how Covid-19 will ever be conquered if governments cannot come to terms with what this disease is and what it isn't. Sweden stands alone as the country that has made the hard choices and now seems well on its way to developing herd immunity and to talking about its economy and future without making many special accommodations and certainly without being held hostage to the virus, its spread and the prospect of never ending lockdowns.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief