Global| Sep 16 2014

Global| Sep 16 2014ZEW Expectations Drop By Less Than Expected

Summary

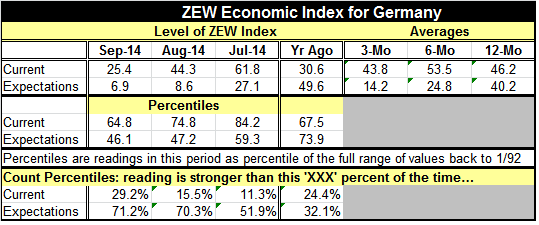

The ZEW index in September fell to a level of 25.4 from the August level of 44.3. This drop means that current conditions have been stronger than this 29% of the time, instead of 15% of the time as was the case last month. The [...]

The ZEW index in September fell to a level of 25.4 from the August level of 44.3. This drop means that current conditions have been stronger than this 29% of the time, instead of 15% of the time as was the case last month. The assessment of current conditions has taken a big hit this month.

The ZEW index in September fell to a level of 25.4 from the August level of 44.3. This drop means that current conditions have been stronger than this 29% of the time, instead of 15% of the time as was the case last month. The assessment of current conditions has taken a big hit this month.

The expectations reading in September fell to 6.9 from a level of 8.6 in August. This index had been expected to fall further. However, we have to evaluate these two indices - current and expectations - together. Expectations are formed from a base of current perceptions of current conditions. Since current conditions fell sharply between September and August, it's not surprising that expectations, while lower, didn't fall as much as had previously been expected. The relatively small drop in expectations, a drop of 1.7 points month-to-month, suggests that expectations may be coming into line with the level of current conditions. Even so, expectations continue to be quite weak as they are higher 71% of the time.

This month the ZEW experts' assessment of the stock market fell to a reading of 3.0 from 4.1 in August. The assessment for bonds improved slightly to -0.4 from -6.7 the month before. Neither of these assessments is particular strong.

The sector assessments are split this month with the ZEW financial experts giving higher readings to seven out of 13 stock market sectors. However, there is a substantial cut to the consumption and trade expectation which has fallen to the 72nd percentile of its range from the 81st percentile - and was last lower in June 2013. The construction sector assessment also dropped sharply to a 70.8 percentile of range standing from its 80.5 percentile standing in August; it was last lower in October 2013. On the upside, there were no dramatic moves, for the most part, just small increases. The stock market, judging from the standing of its individual sectors, had is weakest reading since June 2013.

The ZEW data are another black eye for European growth prospects. The German current conditions index fell sharply and it's too soon to say that expectation deterioration is really out of the woods. Uncertainties continue to overhang the outlook for Europe and Germany, as the cease-fire in Ukraine is still in force but continues to produce significant violations. Ukraine is offering some independent decision-making to its rebel provinces. Meanwhile, Europe is still at risk to the Scottish secession referendum. Reports from Russia continue to show a withering economy as the latest news is that General Motors is reducing staff at its Opel plant in Russia. The weaker the Russian economy gets, the more dangerous Russia becomes. Meanwhile, general world conditions continue to produce a great deal of uncertainty about political and economic outcomes.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief