Global| Feb 16 2021

Global| Feb 16 2021ZEW Assessments Step Up in February Despite the Virus

Summary

The ZEW financial experts have regained their optimism in February. Despite a spreading virus and lockdowns (just ending in Germany) and new variants of the virus (some of which spread faster and more lethal and some of which are [...]

The ZEW financial experts have regained their optimism in February. Despite a spreading virus and lockdowns (just ending in Germany) and new variants of the virus (some of which spread faster and more lethal and some of which are vaccine resistant), the ZEW experts have faith that government efforts will prevail. Bravo!

The ZEW financial experts have regained their optimism in February. Despite a spreading virus and lockdowns (just ending in Germany) and new variants of the virus (some of which spread faster and more lethal and some of which are vaccine resistant), the ZEW experts have faith that government efforts will prevail. Bravo!

This week Japanese finance minister Taro Aso said that most G7 members such as Japan, Britain, the United States and France agreed that now is not the time to withdraw fiscal support for their coronavirus-hit economies. This kind of sentiment is growing and the existence of vaccines and redoubled efforts to deploy them are causing expectations to rise that these efforts will succeed.

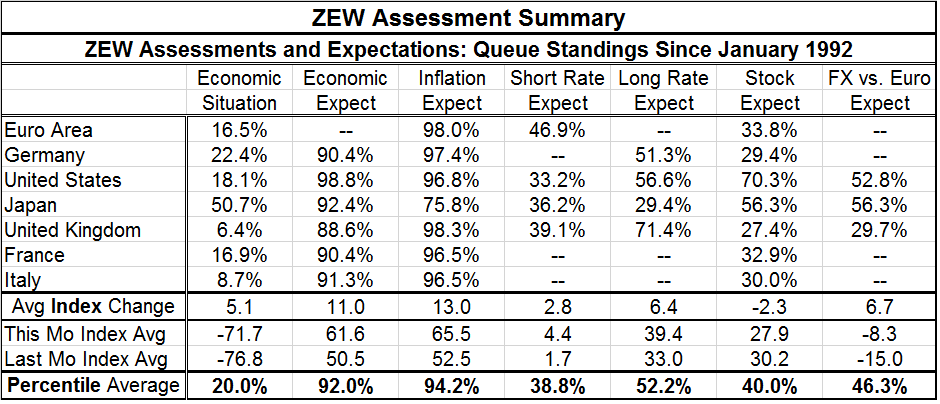

We can see this optimism in the ZEW assessments. The economic situation improved by just 5.1 points on average in February, but economic expectations improved by an average of 11 points. While the economic situation's average standing is only in its lower 20th percentile, expectations now average a 92nd percentile standing across the group. Over three months, the diffusion readings or expectations have risen by an average of 35 points across these countries ranging from a ‘small' improvement of 27.7 diffusion points in the U.K. to 39.2 diffusion points in Italy.

As growth expectations ratchet higher, inflation expectations also ratchet higher. Inflation expectations for the group are up by 13 diffusion points this month driving the average standing to its 94.2 percentile, an extremely high reading. Clearly inflation is coming to be expected as the ZEW experts see fallout from the stimulus being applied. It is surprising that economic conditions have improved so little; yet, fear of inflation has mushroomed as much as it has.

Perhaps some of the reason for this is that as expectations for growth and inflation have improved. Short-term interest rate expectations are higher by only 2.8 diffusion points this month with longer term expectations up by just 6.4 points. Since interest rates are expected to be kept down, fears have risen that government stimulus will over-do it. And monetary policy will lag, on purpose, causing inflation rise. As part of this scenario, we can see that long-term rate expectations (rates controlled by markets) have in fact risen more than short-rate expectations (rates mostly effected by central bank policies). Still, we see a 38.8 percentile standing for short-rate expectations with long-rate expectations rising to a neutral 52.2 percentile reading, very near its historic norm.

Despite all the ‘enthusiasm' for growth and fear of inflation, stock expectations fell by 2.3 points in February on an outlook that is slightly less varied across countries than the overall current macro situation. Stock price expectations have a high of the 70% percentile in the U.S., cling to the 56th percentile in Japan then cluster from the 27th percentile to the 34th percentile across other countries and economic units in the table. The average 40th percentile standing is twice the standing for the economic situation but less than half the standing for economic expectations and inflation. ZEW experts seem confused about what to do with the stock market outlook.

On balance, maybe the ZEW experts will be right. Maybe there is too much stimulus in the pipeline. One problem is how to analyze the generation of all this stimulus while output is being hampered especially in the services sector. One thing we are seeing is that despite ongoing service sector impairment, manufacturing continues to do quite well even as the virus spreads and lockdowns are initiated. Demand has nowhere to go but to the goods sector and that will revive growth in other countries as imports will step up to fill the gap that domestic production can't fill especially as supply chain problems linger. This will also tend to support international trade volumes. Eventually when confidence returns, when there are enough people vaccinated and when there is enough herd immunity, the services sector will normalize. But there will also be more permanent changes, scarring and a transition problem to deal with. It is hard to handicap all that and the end result may not be inflation.

Since unemployment rates (or underemployment rates) are elevated and this stimulus is really a palliative, not really classical extra-stimulus, I am wary about it having such a powerful effect on inflation as well as wary on the lasting impact on growth. The baton handoff from government stimulus to organic growth may not be so smooth. The fact that governments now are still mostly ‘pedal to the metal' and bold about their view of the future does not mean they will stay that way. As much as government stimulus as helped and is still out helping, there are still some special government treatments that are helping to keep people afloat apart from firms retaining workers they do not need or from special broadened or topped up unemployment payments. Whatever the government scheme, and this differs across countries, people whose livelihoods are affected by the virus by and large are not being made whole by government efforts. Surveys in the U.S. (at least) show people have drawn down 401k balances and taken other steps to survive. Some still face heightened liabilities when normalcy returns. I do not think using the standard economic model in this case makes any sense. But that is what just about everyone is doing. And when they do that, they see more growth and more inflation. Maybe it will evolve that way, but I am not convinced and I remain wary of the transition from such government support to the revival of the private sector and the return of capitalism and confidence. In the U.S., at least, efforts are being made to severely undercut capitalism, so it is unclear how fast or fully it will come back there.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief