Global| Jan 22 2019

Global| Jan 22 2019ZEW Assessments Almost Universally Fall...Almost...

Summary

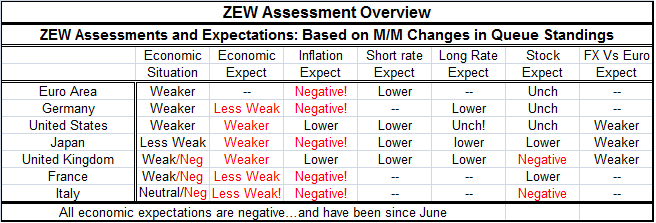

The ZEW indexes each month center on Germany where the survey occurs and where the financial experts reside. The focus is on Germany's economy but also with a global outlook. We have shifted our attention to monitor the global outlook [...]

The ZEW indexes each month center on Germany where the survey occurs and where the financial experts reside. The focus is on Germany's economy but also with a global outlook. We have shifted our attention to monitor the global outlook recently as the global situation seems the most interesting and relevant. In view of that, the day's headlines for ZEW are presented in the press peculiarly. The ZEW survey has always been a focus on the expectations readings and this month 'surprisingly' the German expectation index 'improved' to -15 from -17.5, hardly a shocking shift, but that has 'grabbed the headlines. And it's a mistake.

The ZEW indexes each month center on Germany where the survey occurs and where the financial experts reside. The focus is on Germany's economy but also with a global outlook. We have shifted our attention to monitor the global outlook recently as the global situation seems the most interesting and relevant. In view of that, the day's headlines for ZEW are presented in the press peculiarly. The ZEW survey has always been a focus on the expectations readings and this month 'surprisingly' the German expectation index 'improved' to -15 from -17.5, hardly a shocking shift, but that has 'grabbed the headlines. And it's a mistake.

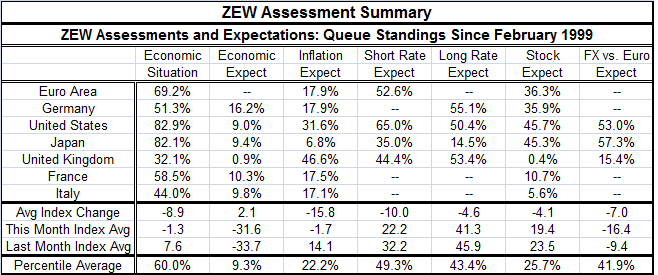

The improvement was a 'surprise' but is that all that significant? I think as analysts we need to get away from the notion that it is the surprise that is important and more important than the fundamental reading. 'Surprise' though it was, does it make a difference? I think the answer pretty clearly is NO! The queue percentile standing for that ZEW reading for Germany improved from its lower 14.2 percentile to its still low 16.2 percentile. The expectations readings for the United States, Japan and the United Kingdom worsened. In France, expectations improved from a low 9% queue standing to a still miserable 10.3 percentile standing. In Italy, there was a substantial improvement in terms of the raw diffusion reading, but that only moved Italy from a stunningly abysmal 2.1 percentile queue standing up to a 9.8% standing, in line with France, Japan and the U.S. If these were betting odds, would Italy's shift from 2.1% to 9.8% cause you to want to bet more on their chances?

On balance, while expectations did improve on a number of European nations the improvements did not in fact count for much. On the other hand in other weakening data, there appears to be more significant harbingers of change. The current situations for all countries but two deteriorated and deteriorated significantly. The two exceptions were Italy where conditions were unchanged (at their 44th percentile) and Japan with a marginal gain from its 80th to its 82.1 percentile. Current readings have been more robust than expectations for some time. But in the EMU the current index fell by 4.7 percentile standing points; in Germany it fell by 14.1 points; in the U.S. it fell by 6 points; in the U.K. it fell by 7.7 points; and in Japan it fell by 10.7 points. These shifts amount to real changes in conditions.

The (unweighted) economic percentile standing is 60% compared to expectations at 9.3%. It strikes me that the 8.9 point deterioration in actual economic conditions was bigger news than the fact that expectations rose by 2.1 points – even though the later was a surprise.

In addition, we have to account for changed inflation expectations where the (unweighted) average diffusion reading fell by nearly 16 points on the month; thus, bringing the unweighted inflation expectation reading down to its 22nd percentile. In the EMU, there was a 19-point drop in inflation expectations (the raw diffusion reading) that took them from +6 to -13.3, a very significant shift. That shift seems much more 'compatible' with the deteriorated economic reading that with some improvement in expectations (note that we do not get an expectations reading directly for the EMU, just for a few large EMU economies and there were somewhat improved expectations in Germany, France and Italy). Inflation expectations have a queue standing close to their median (median at a queue standing of 50) only in the U.K. at a reading of 46.6. The U.S. is next with a lower one-third standing (31%). In the EMU and its large economies, inflation expectations are below their 20th percentile historically and are negative in raw diffusion terms (up minus down diffusion).

As a result of all this or at least in the same mix are vastly lower short-term interest rate expectations. For the EMU where rates already are extremely low, there is little impact as the queue standing that drops from its 55.4 percentile to its 52.6 percentile. In the U.S., rate expectations fall some 14-percentile points to a 65th percentile standing. In Japan, where zero rate targeting is in place, expectations drop by 3.6 percentile points to a 35th percentile standing. In the U.K. where the BOE is data dependent and a Brexit watcher, the percentile standing fell by nearly 25-percentile points to its 44.4 percentile. Long-term rate expectations fell as well and they did so in less sweeping fashion and were quite varied on a country by country basis. In the U.S., for example, despite a large drop in inflation expectations and substantial drop in short-term interest rate expectations, long-term rate expectations hardly budged.

The summary table contains county by country details on percentile standing and some of the overall data on changes based on unweighted averages by category. I think a good deal of the story this month is told by the unweighted percentile averages which show moderate (60th percentile) growth conditions prevailing, very weak (9.3 percentile) growth expectations, and far below average (22.2 percentile) inflation at a time that inflation is already quite tame and generally below target everywhere. Even so short-rate expectations are near normal (their 49.3 percentile standing is very near their median which occurs at a rank standing of 50) and long-term rate expectations (at 43.4) are barely consistent with such weakness for inflation and growth. In fact, expected inflation and actual inflation are so low; it's hard to understand the thought process at central banks apart from representing super sensitive inflation vigilance. Stock market performance expected is at its 25 percentile mark, clearly being held back by all these unusual conditions. What central bankers see as appropriate stock markets see as excessive and restraining.

It seems clear that central bankers are skeptical of the weakness in growth and of the outlook for weaker growth. Their expected posture on short rates belies the weak current situation and expectations for future weakness. Central bankers would appear to be still fighting the last war on inflation. While they guard the front door against inflation, weakness is going to creep in the back door and take them by surprise. Such is the lot of a central banker with only one sort of concern on his mind in a multidimensional world he is handicapped. One can't be successful having a singular focus in a multidimensional world… except by accident.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief