Global| Oct 05 2020

Global| Oct 05 2020World Economy at a Crossroads?

Summary

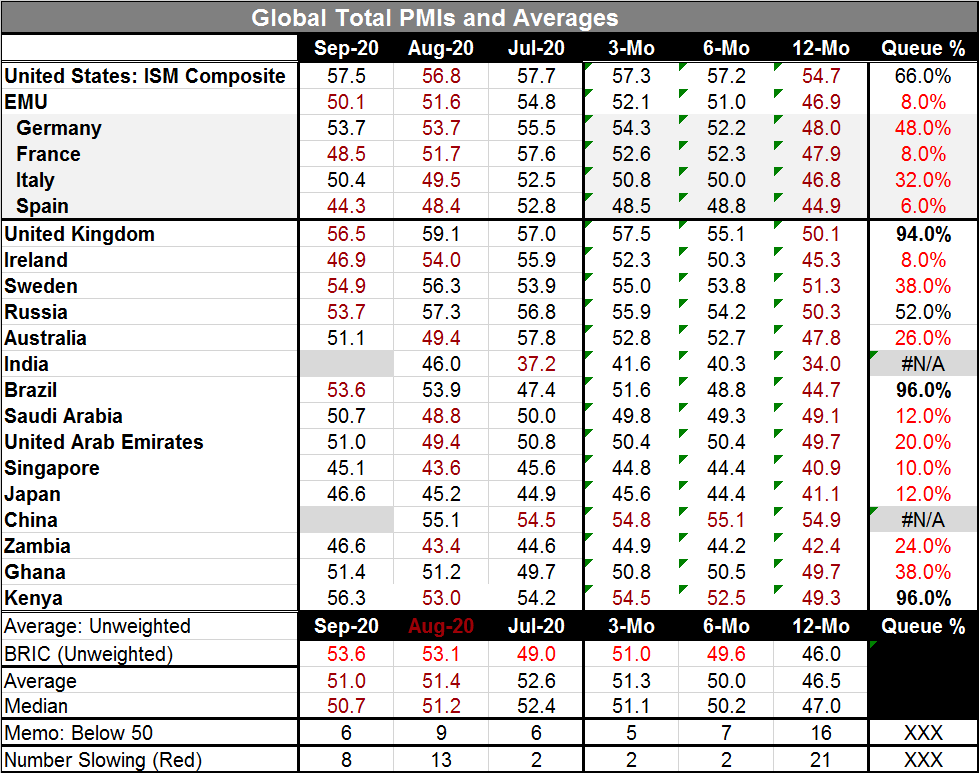

The composite PMIs in September (manufacturing and services or nonmanufacturing) show more improvement month-to-month. There are fewer countries with PMI values below 50 indicating contraction, but both the averages and medians [...]

The composite PMIs in September (manufacturing and services or nonmanufacturing) show more improvement month-to-month. There are fewer countries with PMI values below 50 indicating contraction, but both the averages and medians decline month–to-month (average and median calculation are executed without India and China). So there are still somewhat mixed signals this month.

The composite PMIs in September (manufacturing and services or nonmanufacturing) show more improvement month-to-month. There are fewer countries with PMI values below 50 indicating contraction, but both the averages and medians decline month–to-month (average and median calculation are executed without India and China). So there are still somewhat mixed signals this month.

The global economy continues to dig out from under its covid-19 response-generated recession. But this is not like a dig out from a past and now concluded event. It is more like bailing a boat that was sinking and water is still coming in. The covid-19 virus continues to circulate. And while the setback from the initial attack was severe worldwide, the lingering effects can have significant impact as well. It is unclear if this reinfection is a reflux or a second wave, but Europe in particular is seeing a significant welling up of infections again more or less across the continent and having to respond to that. Next month’s PMI readings are likely to be more affected. There are ongoing repercussions that are slowing growth and impeding recovery - or worse. We can see some of it in this month’s data.

Begin by noting the improvements. The starting point is the 12-month averages of the total (or composite) PMI readings all are lower than their 12-month averages of one year ago. And among the 21 observations in the table, 16 are below 50, indicating contraction. From there go to the six months averages where only 7 are below 50 and only 2 are weaker than their respective 12-month averages. Progress continues in comparing the three-month average to the six-month average as only five are below the neutral level of 50 over three months and only two show decelerations compared to their six-month average.

Moving on to the monthly data is where signs of backtracking seep in. The number of countries with readings below 50 stabilizes at 6. And the number slowing month-to-month is up to eight in September. Moreover, the values for the median and average for this set of countries falls from July to August to September

More broadly, the levels attained in this process of regeneration are still substandard. The queue rankings tell that. Three countries have rankings in the 90th percentiles: Kenya, Brazil and the United Kingdom. The United States and Russia have PMI values above their 50% marker which puts them above their 4.5-year median values. And all the rest have values below their historic medians – most of them by quite a lot.

There is talk about the shape of recovery and maybe the talk should be more about its length than its shape. To whatever extent, there has been a V-shaped recovery to this point it no longer seems to be in gear. And as momentum fades and growth slows and new risks from the virus impose themselves, what happens next? Monetary policy is already pedal-to-the-metal. Sure central banks can always pull another rabbit out of their hat; but these rabbits get increasingly scrawnier. Fiscal policies have been used in large measure to secure stability and promote growth. They have been used to such an extent there is growing reluctance to renew the sorts of things that already have been done. The U.S. is the prime example of this phenomenon.

Momentum and special stimulus have carried us to a strong four-month run from recession lows. But the trouble is that this is not a normal recession-recovery process. Recessions typically end and recoveries take hold building a bit at a time- some are faster, some are slower. But what is unusual here is that at the four-month mark of recovery, that thing that triggered recession is welling-up again. That is not normal yet that is exactly what is happening with the virus. It did not hit the economy once then leave it alone. It has hit the economies hard and it continues to linger and to mushroom. This is not an out-of-the-box cookbook recovery that is being experienced. Since the virus is new, there is little known about its tendency for reinfection or to foster a second wave. Even though it is not really a prolific killer, it is a prolific spreading disease because it is so hard to tell who has it when it is in its transmittable stage. And it kills enough people randomly-enough that few really want to take a chance at getting infected. It has shut down sectors of the economy that simply are not coming back as long as there is ‘social distancing.’ And there is no sense when these sectors or jobs will be coming back. That is another thing that limits economic recovery. Will the recovery be limited in its duration as well as in scope? That is becoming more of a real risk as things drag on at least until or unless a ‘real’ vaccine is developed.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief