Global| Sep 15 2009

Global| Sep 15 2009US Retail Sales Make Strong Gains...

Summary

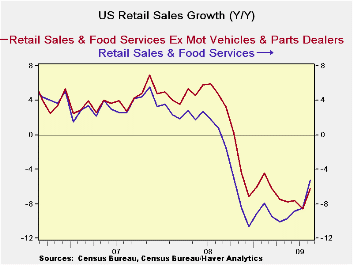

US retail sales rang up strong results in August. The cash for clunkers program aided auto sales to a greater extent that most economists had anticipated. Sales rose by 2.7% month-over-month boosted by vehicle sales which rose by [...]

US retail sales rang up strong results in August. The cash for

clunkers program aided auto sales to a greater extent that most

economists had anticipated. Sales rose by 2.7% month-over-month boosted

by vehicle sales which rose by 10.7% on the month. Most major

categories of sales rose in the month; furniture and electronics was a

minor exception dropping by 0.1% and building materials was a major

exception falling by an outsized 1.2% on the month. Stripping out

gasoline stations where sales rose 5.1% mostly on higher prices and

removing motor vehicles as well left retail sales up by 0.6% on the

month. That particular sub-group exhibits improving sequential growth

rates as well.

Year-over-year sales declines are still severe and that is a

legacy of the severity of the recession and its impact on the consumer.

Over 7miln jobs have been lost in the business cycle and that is a huge

loss of income and of spending power for those consumers. But while the

Yr/Yr drops are severe there are also some distortions. Nondurable

goods sales excluding gas stations are down by only 0.9% Yr./Yr.

Durables spending is down by 5.8% Yr/Yr on large declines in building

materials and in furniture. The boost to vehicle sales this month

leaves them lower Yr/Yr by just 1%.

The messages from this report are that the consumer sector has

been hit hard by recession. Cash for clunkers has boosted auto’s up

form weakness overall and has given those sales a huge boost in the

month- a boost that is likely not sustainable – that’s the bad news

looking ahead. Still, the August results leave sales in the new quarter

(Q3) expanding at an annual rate of 9.5%. Extracting the vehicle

component that growth rate comes down to 2.7%. Ex food and energy sales

are up at a pace of 8.5% in Q3 and estimating the inflation impact

leaves real core sales up at a pace of nearly 7% at an annual rate in

Q3 compared to Q2. This is the compounded growth rate for Q3, two

months into the quarter. But a drop off in auto sales is likely to trim

this impact of quarterly consumer spending on retail sales by the time

the quarter’s final numbers are in.

While it is good news for August and it the best news may be

that sales have spread beyond autos, and have done so without a

government help plan. The real question is how far will auto sales fall

when the cash for clunkers program ends? There will be a spillover of

some sales into September but Q4 will have to do what it can without

any boost from this special program. All that raises some questions

about the future, despite some nice improving fundamentals for the

economy. The downside of government support programs is that those

programs one day end… a second downside factor is that somebody has to

pay for them.

| Retail Sales Trends | |||||

|---|---|---|---|---|---|

| Mo/Mo | Seasonally Adjusted Annual Rate | ||||

| Retail Aggregates | 2009.Aug | 3-Mo | 6Mo | Yr/Yr | YrAgo:Y/Y |

| Retail & Food Service | 2.7% | 14.3% | 4.7% | -5.3% | 0.8% |

| Retail Excl MV&Parts | 1.1% | 5.1% | 0.1% | -6.2% | 4.7% |

| Retail Excl MV&Parts&Gas | 0.6% | 1.0% | -2.3% | -2.9% | 2.5% |

| Durables | 2009.Aug | 3-Mo | 6Mo | Yr/Yr | YrAgo:Y/Y |

| Totals | 5.9% | 32.1% | 10.8% | -5.8% | -10.1% |

| Building Materials | -1.2% | -13.6% | -9.5% | -13.6% | -2.0% |

| Motor Vehicles & Parts | 10.6% | 70.3% | 29.5% | -1.0% | -14.4% |

| MV Dealers | 11.9% | 83.3% | 35.0% | -0.8% | -15.9% |

| Furniture,electonics,etc | -0.2% | -4.5% | -15.9% | -11.6% | -5.0% |

| NonDurables | 2009.Aug | 3-Mo | 6Mo | Yr/Yr | YrAgo:Y/Y |

| Totals | 1.4% | 7.8% | 2.3% | -5.1% | 6.2% |

| Food&Bev | 0.5% | 0.9% | 1.9% | -1.1% | 6.8% |

| Health | 0.4% | 1.3% | 2.3% | 2.9% | 3.2% |

| Gasoline | 5.1% | 47.4% | 24.5% | -26.7% | 20.6% |

| Clothing | 2.4% | 1.2% | -4.8% | -5.1% | 0.6% |

| SportGoods | 2.3% | 12.8% | 0.4% | -0.4% | 0.6% |

| GenlMerch | 1.6% | 5.0% | -1.9% | -0.7% | 3.7% |

| NonStore Retailers | 0.1% | 9.7% | 2.5% | -2.6% | 4.0% |

| Misc Retail | 0.2% | 1.3% | 2.3% | 2.9% | 3.2% |

| NonDurables EXCL Gas | 0.8% | 3.2% | -0.4% | -0.9% | 3.8% |

| Services | |||||

| Food Service & Drinking | 0.3% | -0.5% | -1.7% | 0.7% | 3.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief