Global| Feb 11 2021

Global| Feb 11 2021Unemployment Steadies in EMU

Summary

Covid-19 has turned the labor market upside down and inside out by jettisoning some of the basic rules on which labor markets operate. Governments have taken on such a large role in the labor market that it is hard to tell sometimes [...]

Covid-19 has turned the labor market upside down and inside out by jettisoning some of the basic rules on which labor markets operate. Governments have taken on such a large role in the labor market that it is hard to tell sometimes what the true underlying conditions really are. Governments have imposed lockdowns making working impossible, they have outlawed some businesses or restricted the number of persons that a business can accommodate and governments have defined how labor can be treated. In the U.S., government programs provide a major backstop to the labor market.

Covid-19 has turned the labor market upside down and inside out by jettisoning some of the basic rules on which labor markets operate. Governments have taken on such a large role in the labor market that it is hard to tell sometimes what the true underlying conditions really are. Governments have imposed lockdowns making working impossible, they have outlawed some businesses or restricted the number of persons that a business can accommodate and governments have defined how labor can be treated. In the U.S., government programs provide a major backstop to the labor market.

In Europe, firms largely have retained workers and in some cases put them on short time. This has greatly stabilized unemployment rates in Europe. And while such an arrangement protects workers economically, it may also provide some disincentives for firms to grow and to hire more labor as the conditions improve. In the U.S., workers were largely let go and allowed to collect unemployment insurance. They saw that unemployment payments were ‘topped up’ with some additional federal payouts. There is also a payroll protection program that funnels monies to employers who keep workers on their payrolls; that program provides a buffer for the unemployment rate. Affected workers in the U.S. fall under one of these two schemes.

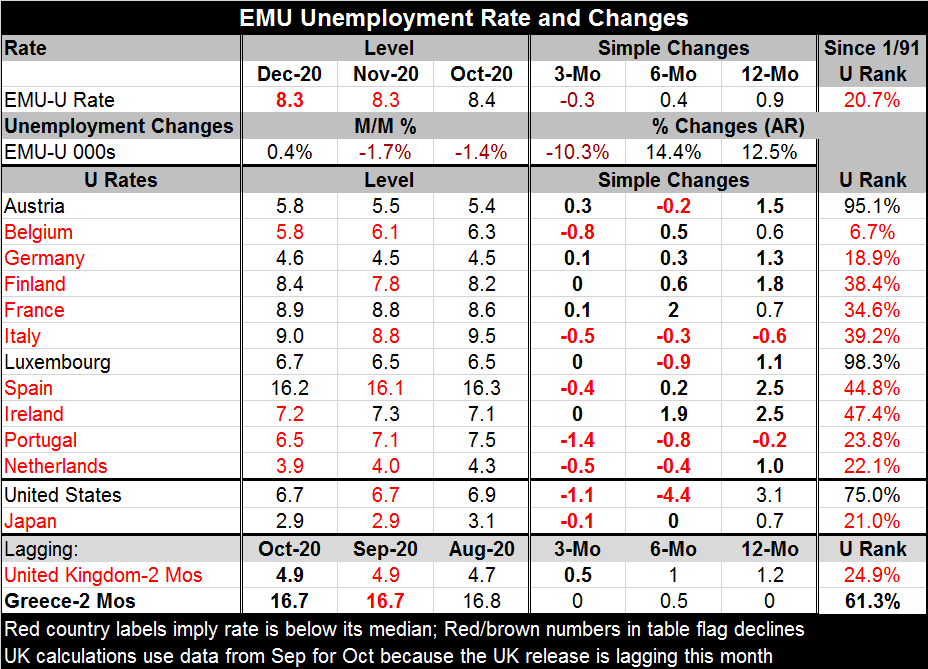

The U.S. and European approaches have very different impacts on the rate of unemployment. The rate in the U.S. spiked sharply when pandemic first hit; it rose by much more than the rate in Europe. However, the U.S. unemployment rate since has fallen very sharply. It now resides below the rate in the EMU. However, the year-over-year change in the EMU unemployment rate is just 0.9 percentage points compared to 3.1 percentage points in the U.S. The U.S. on balance still has more dislocations than Europe in the aftermath of Covid-19, at least on the face of it. But Europe will have more workers on short-time programs too.

In December, the unemployment rate fell in 4 of the 11 EMU members recorded in the table with timely unemployment data (this reference excludes Greece). Unemployment rates had fallen for six of them last month. Year-on-year, however, unemployment rates are still largely higher on balance. Year-on-year unemployment rates are higher in all but two EMU members in the table (Italy and Portugal are exceptions).

However, unemployment rates across Europe are still to be regarded as low. The rate for EMU overall stands in the lower 20th percentile of its queue of ranked data. Only two EMU members (Austria and Luxembourg) have rank standings for their unemployment rates above their historic medians (above 50%). And while the U.S. unemployment rate is below the EMU rate, the rank standing of the U.S. rate is in its 75th percentile, well above the 20th percentile standing for the EMU. On that relative comparison, the EMU is doing much better than the U.S.

The upshot is that the U.S. treatment of the unemployed has been much harder on them that it has been on the unemployed in Europe. On top of that, these statistics do not report on the proportion of American workers that lost heath care when they became unemployed. That remains as an extra burden for many of them.

The graphic is clear that the virus struck and worsened conditions for employment. And while there has since been some improvement, labor on balance is worse off. The virus is still spreading. Vaccinations are being employed and the virus is mutating; mutation is making the vaccine less potent in some places around the world. All of this confuses the options for policy and the outlook.

There continues to be a great deal of uncertainty about the future. The EU has just cut its outlook. In its interim winter forecast, the EMU region now is projected to advance by 3.8% instead of the 4.2% that previously had been expected for 2021. However, this downgrade to 2021 also resulted in an upgrade of the 2022 forecast to 3.8% from 3%. And, of course, forecasts are still sort of flailing around in the dark since there is no way to really pin down what growth will be or how well it will evolve.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief