Global| Aug 04 2005

Global| Aug 04 2005Unemployment Insurance Claims Continue Downtrend

by:Tom Moeller

|in:Economy in Brief

Summary

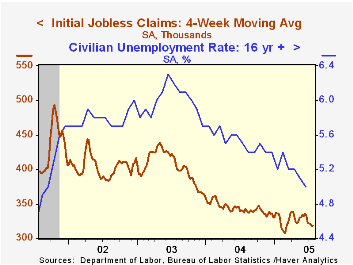

Initial claims for unemployment insurance ticked down to 312,000 last week from an upwardly revised 313,000 the prior week and contrasted to Consensus expectations for 315,000 claims. The four week moving average of initial claims [...]

Initial claims for unemployment insurance ticked down to 312,000 last week from an upwardly revised 313,000 the prior week and contrasted to Consensus expectations for 315,000 claims.

The four week moving average of initial claims declined to 316,750 (-7.5% y/y). The decline continued the minor downtrend in place since earlier this year when claims neared 350,000, and the major downtrend since early 2003 when claims touched 430,000.

Continuing claims for unemployment insurance fell 18,000 following a downwardly revised 28,000 increase one week earlier.

During the last ten years there has been a (negative) 75% correlation between the level of initial claims for unemployment insurance and the monthly change in payroll employment. There has been a (negative) 65% correlation with the level of continuing claims.

The insured unemployment rate remained at the four year low of 2.0% for the third straight week.

Payroll Employment Data: Measuring the Effects of Annual Benchmark Revisions from the Federal Reserve Bank of Atlanta can be found here.

| Unemployment Insurance (000s) | 07/30/05 | 07/23/05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Initial Claims | 312 | 313 | -8.8% | 343 | 402 | 404 |

| Continuing Claims | -- | 2,581 | -11.1% | 2,926 | 3,531 | 3,570 |

by Carol Stone August 4, 2005

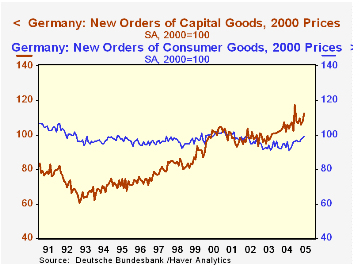

Manufacturers' new orders in Germany increased 2.4% in June, following a similar 2.3% gain in May. Forecasters had expected that after the good May rise, orders would be flat in June, so this was a pleasant surprise. This month, it was orders from domestic German customers that gave the push, while in May, foreign customers' orders had the lead. As seen in the table below, foreign orders have been particularly strong over the past year, although domestic orders have shown moderate growth as well.

Further encouragement to the German outlook came from the fact that capital goods orders had the greatest strength. These rose 4.2% in the month and stand 12.9% above a year ago. Among individual industries, the year-on-year pattern highlights this strength in electrical equipment and transport equipment. Consumer orders are also rising, but less vigorously.

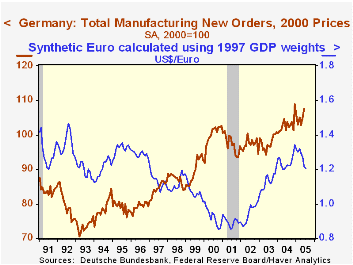

Press commentary today highlighted the decline in the euro so far this year as a factor supporting both domestic and foreign orders in the German factory sector. But the second graph doesn't seem to bear this out. Foreign orders turned higher before the currency value began to fall. Possibly the uptrend would have faded without the boost from a cheaper euro, but the currency value was not the initial force in the upturn. Rather, we would surmise that for both domestic and foreign orders the recent increases have come as the post-Y2K recession ran its course. Perhaps this performance will work its way into the consumer sector and help to improve the sluggish retail trade trends we discussed here yesterday.

| Germany % Changes, Months seas adjusted |

June 2005 | May 2005 | Apr 2005 | Year/ Year | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| Total | 2.4 | 2.3 | -2.2 | 9.0 | 6.4 | 0.6 | -0.3 |

| Domestic | 4.0 | 0.6 | -0.5 | 6.8 | 4.3 | -0.1 | -3.4 |

| Foreign | 0.8 | 4.9 | -4.6 | 11.1 | 8.9 | 1.5 | 3.5 |

| Capital Goods | 4.2 | 1.9 | -3.2 | 12.9 | 7.7 | 1.2 | -0.9 |

| Consumer Goods | 0.8 | 1.2 | 1.4 | 9.0 | 1.2 | -3.6 | -3.0 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief