Global| Mar 13 2014

Global| Mar 13 2014Unemployment in Europe Is Stubborn...and Telling

Summary

There is no comparison between the drop in the US unemployment rate and the slow downward crawl of the unemployment rate in Europe. Of course, the US recovery has been ongoing while the European recovery is nascent. But that is part [...]

There is no comparison between the drop in the US unemployment rate and the slow downward crawl of the unemployment rate in Europe. Of course, the US recovery has been ongoing while the European recovery is nascent. But that is part of the point.

There is no comparison between the drop in the US unemployment rate and the slow downward crawl of the unemployment rate in Europe. Of course, the US recovery has been ongoing while the European recovery is nascent. But that is part of the point.

Even now, when the European recovery is supposed to be stepping up and more noticeable in terms of ongoing improvements in industrial production, increases in manufacturing and service sector PMI gauges, and more, the unemployment rate in Europe is still stuck.

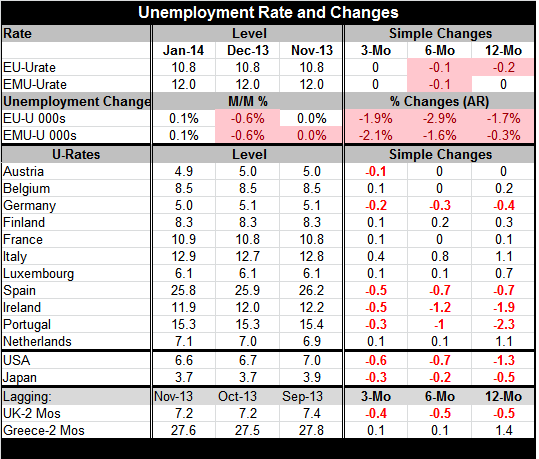

The number of unemployed continues to fall but the rate itself is stuck. In the economic union, the number of unemployed is down at a 1.9% pace over three months compared to dropping at a 2.1% pace over three months in EMU. These statistics refer to the number of people unemployed. Over six months and 12 months, both the EU and the EMU definitions show the number of people unemployed continues to contract. Generally, the contraction has been greater for the European Union (EU) although recently the European Monetary Union (EMU) decline has stepped up and its rate of decline has slightly outpaced that for the EU, at least over three months. In the current month (January), the number of unemployed has ticked up for both the EU and EMU definitions of the number of unemployed.

However, when you look at the unemployment rate which assesses unemployment relative to the size the labor force, we find that the progress in Europe is still halting. Both the EU and the EMU unemployment rates are unchanged over three months; each of them has declined but by just 0.1% over six months. Over 12 months the EU rate is down by 0.2 percentage points while the EMU rate remains dead flat. Are these the trappings of an area experiencing a true recovery?

Looking at the country experience, out of the 11 countries in the table the unemployment rate over three months has fallen in five of them. It's falling relatively sharply in Spain and in Ireland. It has fallen moderately sharply in Portugal and in Germany while the rate has ticked down in Austria. Meanwhile Belgium, Finland, France, Luxembourg and the Netherlands show slight upticks in the unemployment rates. Italy shows a sizable increase of 0.4 percentage points over three months. Looking at six-month changes, five countries have declines in their unemployment rates compared to four having increases and three being unchanged. Even over the broad 12-month period, only four countries show declining unemployment rates with six experiencing rising unemployment rates. Europe is still far from having every country on board in terms of labor market progress. And it's hard to have real economic recovery without labor market progress.

We compare the results in Europe with the real thing in the US; there is no comparison. Even cherry picking the best European statistics over 3-months, 6-months and 12-months, Europe is barely able to keep up with what the US been doing overall. The US rate has fallen by 6-tenths of a percentage point over three months, by 7-tenths over six months, and by 1.3 percentage points over 12 months. Japan also shows declines over all of those horizons.

Greek statistics lag those of the rest of the Community. But Greece continues to show a rise in its unemployment rate. The UK, an EU country with some of the best recent economic performance, shows unemployment declining at all the horizons with the maximum drop of 0.5% over 12 months.

By comparison Greece, a member of the Monetary Union, has a rise in its unemployment rate of 1.4% over its most recent 12-month period. The Netherlands has an increase of 1.1% on that horizon as does Italy. Only Germany, Spain, Ireland, and Portugal show steady declines in the unemployment rates on all these horizons.

While many people think that Europe has passed the difficult point of being under extreme pressure but having member countries decide to stay together, that may not have been the true litmus test of unity. Staying together during the financial crisis may have been the best port in that storm but more bad weather still lies ahead. George Soros already has intimated that Europe may find it impossible to stay together. The problem simply is that as Europe gets away from its crisis and into a recovery, many member countries won't experience recovery. There are going to be further tensions within the EMU as these divergences grow. Unless the Union reforms and tries to implement a more uniform fiscal policy - something the Community lacks at the moment and is not considering reforming- it's hard to see the lagging countries continuing to reap any benefits from being in the euro area.

However, there are new problems and risks emerging in the Ukraine. There may be new political reasons for European countries to want to stay together as part of the single unit. However, the economic benefits of being in the EMU are looking like a hardscrabble find for many of the smaller countries that are members. Having to keep up competitiveness with a country like Germany, whose population seems willing to not distribute productivity increases to labor in the form of compensation, makes it hard for fellow EMU members to keep up with Germany's model and its competitiveness.

The lowest rates in EMU: Austrian and German unemployment rates right now are the lowest in the EMU at 5% or just under 5%.

One percentage point up: Next is Luxembourg at 6.1%. But Luxembourg is a special country that's very small and basically makes its bones being a financial center.

One more percentage point up: After Luxembourg we jump up another percentage point to 7.1% in the Netherlands. The next closest to the Netherlands is Finland at 8.3%. Then there's Belgium any 8.5%. After that, we move up to much higher unemployment rates.

The next five percentage point range: France is at 10.9%. Ireland is at 11.3%. Italy posts a 12.9% level. Portugal is at 15.3%.

Ten percentage points above the upper bound of the last range: In Spain unemployment hits 25.8%. Greece's statistics lag, but its most recent rate is at 27.6%. Note that in this high cohort lies the fourth largest country in the EMU, Spain.

There's nothing in these statistics to suggest that these countries are part of a single union. Germany shares a geographic border with France yet its rate of unemployment is less than half of the French rate. With true labor force mobility, it would be hard for pockets of unemployment such as these to persist. But we all know that these differences in unemployment rates have persisted and do persist. This is the simplest evidence possible that European labor market integration has a very long way to go.

Can the Union endure with a policy of separate but unequal? It is a currency union or the book Animal Farm in action?

Because of these obvious internal segmentations, Europe is going to continue to see differential rates of growth across the euro area. So long as the same countries continue to lag, and it's likely that they will, pressures within the euro area are going to continue to build. This is why despite the fact that we see ongoing recovery in Europe, we continue to be wary of the tensions and pressures inside that could create difficulties.

Currently, Europe is working on rules for back-stopping versus resolving banks in a financial crisis. The Union continues to have a very hard time with this notion partly because there continues to be tension between the control that local countries want to have versus the need to secede some of that responsibility to a centralized authority. Yet there is distrust of what that centralized authority might do and who might dominate its control.

In the financial crisis there were very sharp differences between the Germans and the other countries, particularly those that were struggling under financial distress. The German prescription that the already struggling countries should undergo austerity, greatly hammered economies that were already floundering. That policy dictate has not made Germany a lot of friends in the rest of the euro area. The forbearance exhibited by the European Central Bank came with a non-German at the helm and the Bundesbank fought Draghi's attempts at forbearance every step of the way.

Whether the German policy prescription of austerity works where it has been applied, depends upon the ability of the countries that have on undergone austerity and will continue to undergo some degree of austerity to stick with it over the long haul. A faster rate of growth in Europe overall would help them a lot. But that does not seem to be in the cards. Their continued toeing of the fiscal line will be a very tough job if there isn't any monetary union-wide method of relieving the pain locally. The notion that a single currency can work magic has been thoroughly debunked by this experiment. Are the participants willing to take another step for the sake of continued unity or will the EMU's cohesiveness be tested again?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.