Global| Jun 20 2019

Global| Jun 20 2019UK Retail Sales Backtrack Again But Maintain Forward Momentum

Summary

The UK economic and political drama continues to play out and, as it does, retail sales are withering. Boris Johnson is a step closer to being named Prime Minister. At the BOE meeting, policy was kept on hold as the bank cuts its [...]

The UK economic and political drama continues to play out and, as it does, retail sales are withering. Boris Johnson is a step closer to being named Prime Minister. At the BOE meeting, policy was kept on hold as the bank cuts its outlook for GDP growth from 0.2% to flat for the second quarter. The BOE has seen growth propped up recently by stock building as businesses have accumulated inventories of goods in case the Brexit plan leads to a situation in which border delays are created. The BOE now thinks that businesses have built stocks sufficiently; the boost to growth from stock-building is over. Of course, that also means that sometime ahead those stocks will be drawn on and, at that point, consumer spending will not be stimulating GDP rather it will be accommodated by drawing down stocks. Stock building is better thought of a shifting growth from one period to the next rather than stimulating it.

The risk from Brexit stock-building However, all this is in train as UK retail spending is in a period of slippage. Having weakening retail spending and stocks built in anticipation of border issues at the same time could make the UK economy vulnerable. Together these two events could completely neutralize stimulus efforts by the BOE in the period ahead. If spending slows or backtracks at the same time stocks are high to service demand, the BOE might find a stimulative rate cut to have no impact on growth as any revival in consumer spending would only draw down inventories and businesses would not be eager to replace stocks that had been elevated artificially.

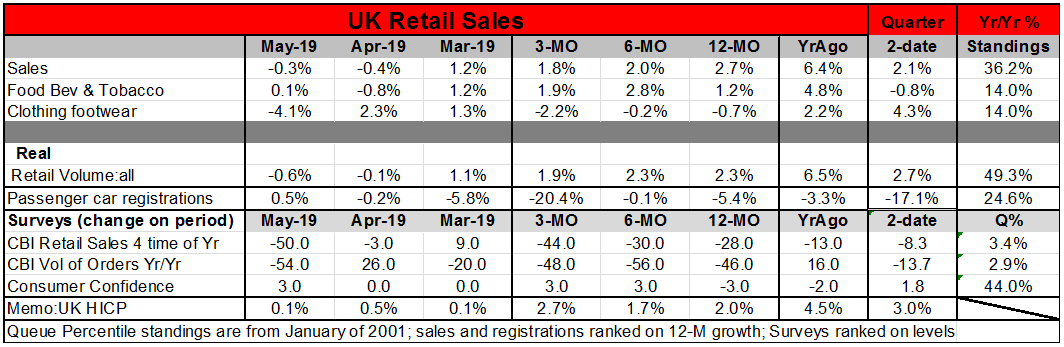

Retailing trends Nominal retail trends show a slowing from a 12-month –growth rate of 2.7% to 2.0% over six-months to 1.8% over 3-months. Retail sales volumes show a slight erosion with six- and 12-month trends at a 2.3% pace and three-month sales at an only slightly weaker 1.9% pace.

Quarter-to-date performance Because of a spurt in sales in March at the end of Q1 that elevated the level of retail sales just before the start of Q2, the two mild sales declines in March and April still leave retail sales and-sales volumes- expanding in the second-quarter to date (QTD). The QTD calculation looks at the two-month average for sales, positioning it correctly to calculate its growth over the Q1 base. Unlike a three-month growth calculation the base for this calculation will not shift when June data are available. The Q2 growth rate will change because of the effect of adding the now-unknown June retail sales result to the current two month average. So the QTD gives us a good read how growth is evolving in Q2 compared to Q1 and a notion of what comes next. Sales seem poised to rise in Q2.

Momentum However, sales momentum is not strong. We have already presented the sequential growth rates for nominal and real sales. We can also present rankings of the year-on-year pace in historic profile. For nominal sales the ranking is only in its 36th percentile. For sales volume the ranking is better and closer to neutral with a 49.3 percentile standing. The median for both of those ranking calculations occurs at the 50th percentile mark.

Vehicle registrations Despite this firmness in retail sales, passenger car registrations are slipping. Registrations rose by 0.5% this month after two months of declines. Registrations have fallen month-to-month half the time over the past year. However, year-on-year registrations are lower in eight of the last nine months. Registrations are falling over 12-months over 6-months and over three-months but there is no steadiness to the path of contraction. In the QTD sales are lower at a 17.0% annualized rate. The year-on-year growth rate ranks as lower since March of 2002 only about 25% of the time.

Mixed message in sales data While UK retail sales are generally putting up growth figures based on trending data despite recent nominal and real declines it is clear that sales are struggling. The weakness in the big-ticket item vehicle registrations is another negative factor. CBI survey data in fact show sales for the time of year at a 3.4% ranking, rarely weaker. The CBI volume of orders year-over-year have been weaker only 2.9% of the time. However, in May UK consumer confidence rose by 3 points to a still-below median 44th percentile standing.

The economy is holding up well considering that Brexit has been up in the air for so long and that Tories are changing Prime Minister in mid-stream of the negotiations. The UK side expects to be able to be able to reopen negotiations on Brexit, while the EU has looked at the matter as settled. Perhaps if Mr. Johnson wins the position as is expected the EU will give him a listen if he has anything new to say.

Johnson: OUT!! Johnson has been clear that the UK must be "out" by Halloween if it is to have credibility. He also is of the point of view that hard Brexit should be on the table and it is increasing looking as though it may also wind up being underfoot. The UK economy and Brexit circus will remain in full swing for some time to come but seems destined to conclude by end October.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief