Global| Oct 01 2007

Global| Oct 01 2007UK MFG Drops Off but Remains in a Growth Profile

Summary

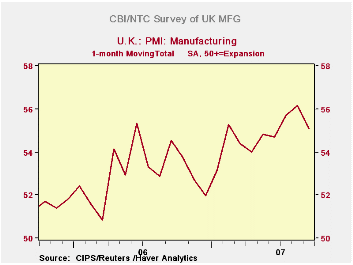

The UK manufacturing sector was weaker than expected in September but output price pressures rose to a record high, according to the latest Chartered Institute of Purchasing and Supply/NTC survey. The headline UK September [...]

The UK manufacturing sector was weaker than expected in September but output price pressures rose to a record high, according to the latest Chartered Institute of Purchasing and Supply/NTC survey. The headline UK September manufacturing index posted a level of 55.1, down from the now weaker 56.1 level registered in August. The reading still marks small gains on the three-month, six-month and year-over-year horizons for comparison (see table). Output prices rose to 57.8 in September from 56.0 in August, hitting their highest level since records began in 1999. The Bank of England has identified inflation as an upside inflation risk in the economy. This latest CIPS/NTC survey suggests that manufacturers are managing to push through price hikes. Nonetheless input prices eased to 62.3 from 63.8 in August, their lowest level since February. The pressure off input prices suggests that output price pressure should abate in the months ahead, possibly assuaging any concerns the BOE might have about the output price pressures. The decline in the headline activity index reflected a fall in the new orders index to 55.5 in September from 56.8 in August. Orders are now at their lowest level since January. Current output also fell to 58.2 from 60.5 in August. Moreover export orders plunged to 52.9 in September from 56.1 in the previous month. Other EU countries have been showing erratic readings for export strength. This slowing is part of a broader European pattern.

| MFG PMI CIPS/NTC | ||||||||

|---|---|---|---|---|---|---|---|---|

| Monthly readings | Change over: | percentile | ||||||

| Sep-07 | Aug-07 | Jul-07 | 3MO | 6MO | 12MO | of range | ||

| MFG | 55.08 | 56.15 | 55.71 | 0.38 | 0.68 | 0.55 | 69.4 | |

| Range since January 1992 | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief