Global| May 20 2021

Global| May 20 2021UK Manufacturing Heats Up as Global Trade Gets Back in Gear

Summary

CBI overview and Orders The Confederation of British Industry (CBI) survey for the industrial sector in the UK saw its total orders reading push up to a +17 net reading in May. This net index (a plus/minus diffusion index) is at its [...]

CBI overview and Orders

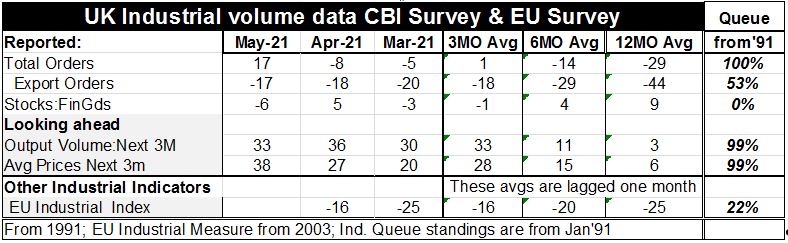

The Confederation of British Industry (CBI) survey for the industrial sector in the UK saw its total orders reading push up to a +17 net reading in May. This net index (a plus/minus diffusion index) is at its highest value since 1991. Most of the performance of the total index is on the back of orders in the domestic economy. Export orders edged slightly higher in May to -17 from -18. This gain put them in the 53rd queue percentile of data ranked back to 1991. Obviously domestic orders are driving the strength for total orders in the UK economy since the rank standing for the total is at 100%.

CBI overview and Orders

The Confederation of British Industry (CBI) survey for the industrial sector in the UK saw its total orders reading push up to a +17 net reading in May. This net index (a plus/minus diffusion index) is at its highest value since 1991. Most of the performance of the total index is on the back of orders in the domestic economy. Export orders edged slightly higher in May to -17 from -18. This gain put them in the 53rd queue percentile of data ranked back to 1991. Obviously domestic orders are driving the strength for total orders in the UK economy since the rank standing for the total is at 100%.

Stocks Stocks of finished goods slipped to -6 in May from +5 in April. That brings the stock entry to its lowest point since 1991. It appears that orders are spurting and stocks have been drawn down and that replenishing supplies may be becoming an issue in the UK as we are seeing in the US as supply chain issues manifest themselves globally.

Volume outlook Looking ahead, output volume for the next three-months saw its response drop to 33 from 36. Not to worry; this is not weakness, just a tailing off from an all-time high reading. The reading on expected output volume has been in its ‘30s’ since March. It rose from a level of -24 in January to -2 in February then took off to this new much higher plateau of readings in the 30s in March. The outlook and expectations of industry have really transformed themselves over the last five months.

Other surveys The expected output response is even much stronger than the move up in the EU Commission’s industrial output index for the UK. That metric is up to date through April and has a queue standing (on data back to 2003) in its 22nd percentile. It is, of course, a current response not a forward-looking response. The Markit PMI gauge (also a current response) for manufacturing ranked back to December of 2016 shows a diffusion value of 60.9 as of April and a rank standing in its 98th percentile; it is at its high point on this reduced time line.

The UK come-back The UK is coming back strongly in the wake of the virus and a second shutdown. It is of course also in the post Brexit environment and so the UK economy is dealing with circumstances that have been jarred significantly by two very different sorts of events.

The Baltic Dry Index and trade prospects

The Baltic Dry Index is an index of non-liquid shipping volume. This metric is coming back strongly and has moved up sharply as 2021 has progressed. The gain in this index offers the hope that the sorts of distortions that we have seen in prices and in product availability will be a thing of the past as trade volumes get back to normal. But there is still log jam at ports and the UK has some special problems as firms get accustomed to new regulations involving trade with the EU. However, even in the US where there is no special change in trade rules ports have lingering issues and significant backlogs as a result of issues that arose under the covid-19 lockdowns. The UK is experiencing a build-up of containers at its ports that is worse than for most other ports in Europe.

The Baltic Dry Index and trade prospects

The Baltic Dry Index is an index of non-liquid shipping volume. This metric is coming back strongly and has moved up sharply as 2021 has progressed. The gain in this index offers the hope that the sorts of distortions that we have seen in prices and in product availability will be a thing of the past as trade volumes get back to normal. But there is still log jam at ports and the UK has some special problems as firms get accustomed to new regulations involving trade with the EU. However, even in the US where there is no special change in trade rules ports have lingering issues and significant backlogs as a result of issues that arose under the covid-19 lockdowns. The UK is experiencing a build-up of containers at its ports that is worse than for most other ports in Europe.

The outlook There are also lingering Covid-19 issues as developing countries are much less inoculated than developed countries. India is experiencing a terrible onset of Covid-19 infection and deaths. Singapore and Taiwan, two countries that had looked like poster children of covid-19 success, have since been hit by a wave of infection. These experiences raise questions about how optimistic we should be. Experts argue about how much of a population must be inoculated in order to offer herd immunity benefits. Even so, now there are some high profile cases of infections spreading among groups that have been well inoculated despite the inoculation. I cannot pass judgment on these as a health expert but as an economist trying to handicap the future I can admit that it all gives me some pause. This virus has been hard to track, to stop, to contain, and to predict. Now it is creating more variants and some look to be more lethal or at least more highly infectious. It looks as though we will be operating in an environment of some uncertainty for a significant period of time ahead – and yes, I am purposely vague about how long that might be, because I do not know what I do not know… .

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief