Global| Sep 06 2007

Global| Sep 06 2007UK IP on Extended Fading Growth Trend

Summary

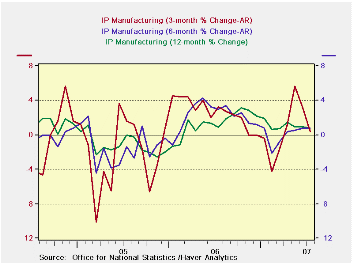

UK industrial production trends are not uniform. Consumer durable and nondurable goods output has been steadily - and in the recent period - strongly expanding. That makes the UK unlike most EMU countries with its strong consumer [...]

UK industrial production trends are not uniform. Consumer durable and nondurable goods output has been steadily - and in the recent period - strongly expanding. That makes the UK unlike most EMU countries with its strong consumer sector (actually France has done OK in this regard, too). Intermediate output also has been gaining momentum. Capital goods output, on the other hand, has been fading. Obviously, consumer durables is being driven by the strength in vehicles output. Textiles output is slowing. Food production has picked up after some past weakness. Mining has also seen output pick up its pace and hold it. (These comments look at 1-year to 6-month to 3-month trends across July, they do not refer to the monthly patterns which are too volatile to explain). Note that the story based on these sequential growth rates across June is quite different. But we are trying to get in touch with newer trends and to understand what is unfolding in Q3.

| Saar except m/m | M/M | Jul-07 | Jun-07 | Jul-07 | Jun-07 | Jul-07 | Jun-07 | |||

| UK MFG | Jul-07 | Jun-07 | May-07 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo | Q-3-Date |

| MFG | -0.3% | 0.1% | 0.3% | 0.4% | 3.2% | 0.8% | 0.8% | 0.8% | 1.0% | -0.8% |

| Consumer | ||||||||||

| Durables | 0.0% | 3.7% | -1.1% | 10.9% | 2.7% | 5.3% | -2.2% | 3.1% | 1.3% | 13.2% |

| Nondurables | 0.4% | -0.5% | 0.4% | 1.2% | 1.2% | -0.2% | -2.8% | -0.1% | -0.5% | 1.2% |

| Intermediate | 0.2% | 0.0% | 0.8% | 4.3% | 3.9% | 2.6% | 4.1% | 1.3% | 0.6% | 3.0% |

| Capital | -1.2% | -0.1% | 0.3% | -4.0% | 4.9% | 0.0% | 2.8% | 1.0% | 2.7% | -6.7% |

| Memo: Detail | 1-Mo% | 1-Mo% | 1-Mo% | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo | Q-3-Date |

| Food Drink & Tobacco | 0.6% | -0.2% | 0.0% | 1.6% | -1.2% | -1.0% | -4.0% | -0.4% | -1.7% | 2.8% |

| Textile & Leather | 0.1% | 0.9% | -0.7% | 1.4% | 3.3% | 3.1% | 0.9% | 2.7% | 1.3% | 3.1% |

| Motor Vehicles & Trailer | 1.9% | 2.8% | 0.6% | 23.2% | 21.2% | 15.4% | 16.5% | 9.2% | 6.7% | 26.3% |

| Mining and Quarry | 1.2% | -0.8% | 1.3% | 7.0% | 7.1% | 7.4% | 11.1% | 2.8% | 0.7% | 6.7% |

| Electricity, Gas & Water | 0.2% | -0.6% | 2.3% | 7.7% | 1.7% | -0.4% | 0.0% | -0.1% | -0.8% | 3.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief