Global| May 20 2014

Global| May 20 2014UK Inflation Trends Cruise Just Below 2%...Finally

Summary

Inflation in the United Kingdom is finally starting to settle down. The harmonized price index for April rose 0.2% after a 0.1% increase in March. The three-month inflation rate is 1.7% at an annual rate compared to 1.5% over six- [...]

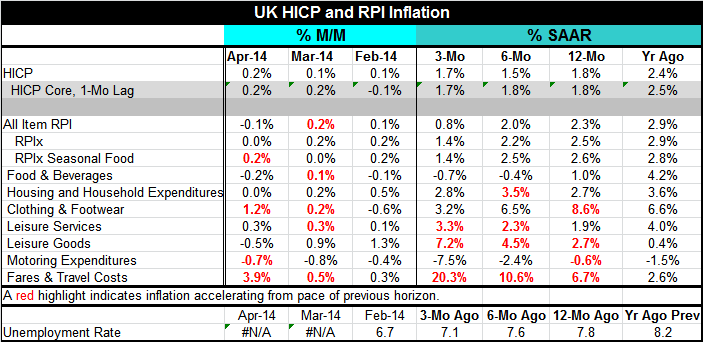

Inflation in the United Kingdom is finally starting to settle down. The harmonized price index for April rose 0.2% after a 0.1% increase in March. The three-month inflation rate is 1.7% at an annual rate compared to 1.5% over six-months; the 12-month inflation rate is 1.8%.

Inflation in the United Kingdom is finally starting to settle down. The harmonized price index for April rose 0.2% after a 0.1% increase in March. The three-month inflation rate is 1.7% at an annual rate compared to 1.5% over six-months; the 12-month inflation rate is 1.8%.

Year-over-year inflation in the previous 53 months has been in excess of 2% in 49 of those months; it has below 2% in each of the last four months. The year-over-year inflation rate has finally fallen below 2%. The Bank of England, after a long and arduous period, has finally succeeded in getting inflation under control. Or so it seems.

Of course, one of the factors that contributed to inflation being over the top was an increase in the value-added tax, which increases final product prices and for a short period boosts the measured inflation rate.

During this long period, during which inflation has run over the top of the target, the UK has set and hit some strict budget targets. Fiscal policy has been geared to adjustment. Central bank ease did not simply accommodate a too loose fiscal stance: quite the opposite. Because the central bank was willing to be flexible and not tighten policy when inflation was boosted over the top by VAT policies, the UK economy has been permitted to grow. The central bank and the government worked together. The UK now appears to have emerged on the other side of its inflation bubble with both growth and inflation intact. That's more than you can say for the European Monetary Union.

The EMU, mostly because of its structure, took a very approach. Monetary policy was kept tight, with few attempts at accommodation, while fiscal policy was tightened everywhere. The results for the euro area are not nearly as good as in the UK. The EMU is only considering some sort of broad asset purchase program- very late in the game and still amid divisiveness.

The Bank of England, however, still has its work cut out for it. BOE Governor Mark Carney has been outspoken on the role of the housing market as being a danger for UK policy. Deep seated problems in housing are posing economic risk to the economy, Governor Carney said. The problem is that there are not enough houses being built; that has pressured prices higher. Low interest rates have helped to keep housing affordable as house prices have risen. But this is a dangerous game and one that will end.

The UK also continues to nurture a damaged banking system in the wake of the financial crisis. All in all, the central bank's policies have been very effective, although in some cases that has involved kicking the can down the road as the banking sector problems have lingered and the housing sector problem has deepened. Still, by comparisons with the EMU countries, the UK's problems are few.

Over the past seven-plus years, inflation has averaged 3.2%, well over the BOE's target, of 2%. The central bank seems to have retained credibility, however. Markets seem to have bought the idea that the special factors were responsible for inflation being higher during much of this period as the BOE Governor has been careful to document in his inflation letters. Now inflation has come back down into the bank's target with the economy still growing. It is a remarkable feat.

However, none of this has been done without missteps. Governor Carney had tried to employ forward guidance, but just like the US Federal Reserve, he found the UK unemployment rate fell much more sharply through what was to be his threshold rate for interest-rate forbearance, leading him to scrap the policy. The UK unemployment rate has fallen to 6.7% in February from 7.8% 12 months ago and 8.2% 24 months ago. The step up and the progress on the rate of unemployment has accelerated and yet the banks policy continues to exercise forbearance and the inflation rate has continued to move down into the bank's target and to stay there.

Of the seven categories in the RPI whose detail we use in the table, only three of them show inflation accelerating month-to-month in April. Four of them had accelerated month-to-month in March. While none of them had accelerated month-to-month in February. Over three-months, inflation was accelerating in three categories with strong pressure in fares and travel costs. Four categories show increasing pressure over six-months compared to 12-months. Four show pressure over 12-months compared to the previous 12-months. Still, headline inflation has continued to ramp down in RPI terms to 0.8% at an annual rate over three months from 2% over six months and 2.3% over 12 months. RPI inflation has run a bit hotter than HICP inflation, but now it is cooling faster.

The Bank of England is trying to exhibit forbearance in its interest-rate behavior still. Yet, growth in the UK economy is looking very steady while inflation has settled down. There can be little doubt, but the legacy of over-the-top inflation will make the BOE motivated to raise interest rates when it feels the economy is on truly steady footing. Given the dynamics of the housing market, it's pretty clear that a rate rise will destabilize the housing industry to some extent. That may keep the BOE on the sidelines a bit longer, but not too much longer. The economy seems be mending faster than in the US. The BOE would seem to be a step or two ahead of the Fed in terms of its preparedness to raise rates.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief