Global| Sep 19 2018

Global| Sep 19 2018UK Inflation Perks Up Unexpectedly

Summary

The UK inflation rate rose unexpectedly in August headline inflation zoomed to a 2.7% annual rate, up from 2.5% just last month. The rise in inflation was unexpected. Core inflation lags the release of headline inflation. Core [...]

The UK inflation rate rose unexpectedly in August headline inflation zoomed to a 2.7% annual rate, up from 2.5% just last month. The rise in inflation was unexpected.

The UK inflation rate rose unexpectedly in August headline inflation zoomed to a 2.7% annual rate, up from 2.5% just last month. The rise in inflation was unexpected.

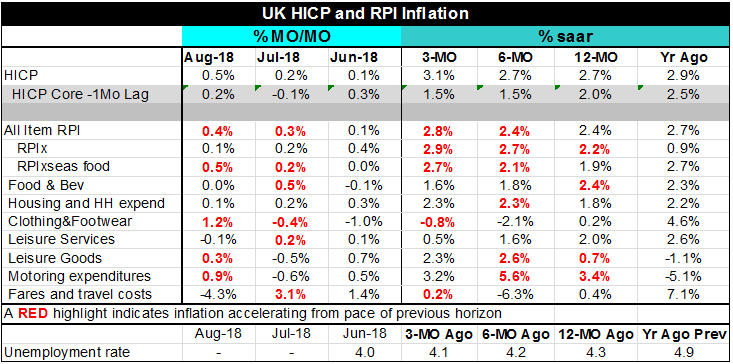

Core inflation lags the release of headline inflation. Core inflation ticked lower to 2.0% from 2.1% in July. Core inflation had peaked around 2.8% in December of last year in this cycle. Since then its pace has been dissipating. That undoubtedly helped to feed the view that inflation overall was on a downswing in the UK. Headline inflation had been expected to continue its erosion and to post a gain of just 2.4% in August. The 2.7% print on the headline was a surprise to say the least.

The RPI gauge has been declining but the RPIx had already had plateaued. Its pace accelerated in May from April and again in June from May and again in August when its year-on-year pace rose to 2.2% from 1.9%.

Energy prices are still an issue here. True, Brent crude oil prices have fallen for three-months running. But year-over-year the oil market pressures peaked in this cycle in June with a gain of close to 60%. Brent has not been in sync with the inflation cycle but that does not mean it isn’t a factor. In December for example when the overall HICP was peaking, Brent was rising by 16% year-on-year. The UK has been fighting off several potential inflation forces ranging from a once sharply weakened pound sterling, rising oil prices and an extremely low rate of unemployment. Western countries as a rule have not been experiencing inflation in this cycle from a low domestic rate of unemployment. So despite extreme lows in the British rate of unemployment there has been less focus on that as an inflation source. Even now with the benefit of hindsight it is hard to pin down exactly what is elevating inflation, beyond a simple taxonomy of weighted effects.

Among seven major product groups UK inflation is higher in only three of them month-to-month.in August. They are (1) clothing & footwear, (2) Leisure goods, and (3) motoring expenditures (with a fuel component). The headline HICP for the UK shows 12-month inflation at 2.7% with the 6-month pace at 2.7% and 3-month pace up to 3.1%. It accelerates on only one horizon.

Presented as a one month offset the core inflation rate falls from 2% over 12-months (as of July) and with its corresponding 3-month a 6-month paces at 1.5%. Inflation is not clearly accelerating according to the core. Inflation is not clearly doing anything to trend. But inflation currently clearly is creating confusion.

Over 3-months compared to six months, inflation is higher in two of seven categories in 6-months compared to 12-months; it is higher in three of seven categories; in 12-months compared to 12-months ago it is higher in three of seven categories. This is hardly a sweeping force of inflation. Even so the headline RPI and RPIx-seasonal food both accelerated in three-months compared to six-months and in six-months compared to 12-months. And the RPIx accelerates in 3-months, over 6-months and in six months compared 12-months and in 12-months compared to 12-months ago. So inflation may not be sweeping across all categories but it is infectious relative to the various RPI categories and their implicit weighting schemes even if the HICP only accelerates over 3-months compared to 6-months in this time-line.

Inflation has several dimensions. It is about the pace compared to the central bank’s target. It is also about the momentum, whether it is accelerating or decelerating, And, finally, it is about breadth, whether it is driven by a special category or two that have special potentially reversible pressures in tow (such as due to oil prices or food). Motoring expenses show accelerations over 3-months and 12-months and note that the 12-month rise of 12-months ago shows the annualized rate of inflation for motoring expenditures was -5.1%. So compared to that, there is a big shift in the year-on-year rate for that category.

In addition there is the future to worry about that brings Brexit into the picture. Theresa May either thinks she is close to sealing deal with the EU or seeks to pressure the EU to change its stance on a part of the negotiations on which they are stalemated by saying how close they are. And that speaks to the treatment of Northern Ireland as the sticking point. Brexit has contributed to the inflation back ground since the unsolved Brexit future has left UK investment in limbo and an economy starved of investment will both wither and will create inflation.

Chronicling and describing the inflation trends as I do above does not really bring us that much closer to understanding their root cause this month. Perhaps that will be clarified when the Core HICP is released. It seems to me that the UK inflation pick-up is more likely to be a one-off event. I do not see the forces of inflation welling up or consolidating. I do not think inflation is emanating from the labor market. And I would expect inflation to go back down but the real key to the UK is not what I think. It is what the BOE thinks… and where the BOE sees the balance of risk lying? Is it more worried about the onset of Brexit and the loss of UK business to the continent or to rising inflation?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief