Global| May 28 2010

Global| May 28 2010UK Consumer Confidence Is Challenged By Electioneering

Summary

According to the Nationwide Building Society’s measure, U.K. consumer confidence fell in March by the most since July 2008 as the election due within weeks fueled Britons’ doubts about the economy. Small surprise that is: so much for [...]

According to the Nationwide Building Society’s measure, U.K. consumer confidence fell in March by the most since July 2008 as the election due within weeks fueled Britons’ doubts about the economy. Small surprise that is: so much for politicians shoring up a feeling of hope and security. Increasingly elections are about making the opponent seem worse than you are. The consumer confidence polls seem to have picked up on this, with the obvious consequences. The index of sentiment fell 9 points from February to 72, erasing the gains in confidence seen so far this year. A gauge measuring expectations for the economy in the next six months fell 11 points to 105.This fall disappointed as the market consensus level was a reading of 81.

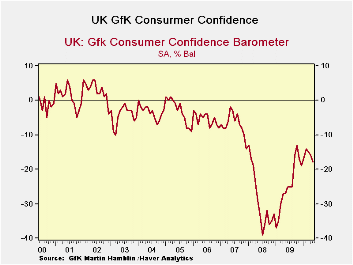

We contrast this result with the GfK survey above. It seems to show less of hit from the electioneering effect but it does demonstrate some backsliding in the assessment of the economy; plenty of raw nerves here for the politicians to tap into. The household financial situation eroded in March as did people’s assessment of their savings. Both lower and higher income respondents saw a worsening.

Looking ahead, fears of unemployment have been rising. The general economic situation is seen as poorer and households expect their financial situation to deteriorate further. There are increased concerns about savings adequacy and growing concerns about inflation.

With this as a back-drop there is plenty of fodder for election politicking to push all the consumers’ buttons. This appears to be in train. Still consumer confidence in the GfK measure is in the 92nd percentile of its two-year range showing considerable progress has been made, but that compares to a standing of just 60% in its 10_year range which emphasizes a bit more how far there is to go. Clearly the UK consumer remains challenged and will find his and her senses assaulted in this election season. May the least worse man win.

| GFK Consumer Survey | ||||||

|---|---|---|---|---|---|---|

| Of 2Yr | Of 10Yr | |||||

| May-10 | Apr-10 | Mar-10 | Feb-10 | Range | Range | |

| Consumer Confidence | -18 | -16 | -15 | -14 | 80.8% | 55.3% |

| Current | ||||||

| Household Fin Sit | 16 | 17 | 18 | 18 | 25.0% | 18.2% |

| Major Purchases | -21 | -20 | -17 | -16 | 71.0% | 36.7% |

| Last 12 Months | ||||||

| Household Fin Sit | -13 | -14 | -15 | -13 | 43.8% | 29.2% |

| General Econ Sit | -45 | -47 | -49 | -50 | 94.9% | 53.6% |

| CPI | 72 | 79 | 72 | 63 | 26.9% | 40.6% |

| Savings | -5 | -7 | -13 | -6 | 37.7% | 29.9% |

| Next 12-Months | ||||||

| Household Fin Sit | -3 | 2 | 4 | 6 | 62.5% | 46.9% |

| General Econ Sit | -9 | -1 | 0 | 4 | 76.8% | 76.8% |

| Unemployment | 36 | 33 | 36 | 31 | 11.1% | 27.3% |

| Major Purchases | -26 | -27 | -28 | -31 | 82.4% | 56.0% |

| Savings | 2 | 1 | 5 | 7 | 29.4% | 19.2% |

| CPI | 71 | 67 | 63 | 60 | 60.8% | 60.8% |

| By Income | ||||||

| Lower | -24 | -22 | -21 | -18 | 77.8% | 50.0% |

| Upper | -11 | -8 | -5 | -3 | 72.4% | 55.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief