Global| Dec 19 2007

Global| Dec 19 2007UK CBI Retail Survey Continues to Deflate Messy-nomics

Summary

It’s telling when an organization like the CBI says that the expected January reading of -5 still corresponds to an annual volume increase of 2.5%. But the result of December is the weakest in a bit over one year (since Nov 2006). The [...]

It’s telling when an organization like the CBI says that the

expected January reading of -5 still corresponds to an annual volume

increase of 2.5%. But the result of December is the weakest in a bit

over one year (since Nov 2006). The expected sales for January are the

weakest since April of 2006. This is not Draconian weakness but then a

look at the plots in this report and an application of the

ever-reliable straight-edge forecast rule gives an idea of where we

might yet be headed. Then again, straight edge forecasts are always

wrong at some point, the only question is: when? Soon or later on? For

the moment, momentum is gone and financial fragility – or even turmoil

- is still with us. The BOE is worried enough to have cut rates even

with a forecast that sees an inflation overshoot into 2008. In an era

when the central banking mantra is "cement and anchor inflation

expectations", this is indeed a bold step by the central bank. Of

course the times are odd since there is even talk from the PM himself

that doesn't rule out a nationalization of Northern Rock. The times

they are a-changin’, aren’t they?

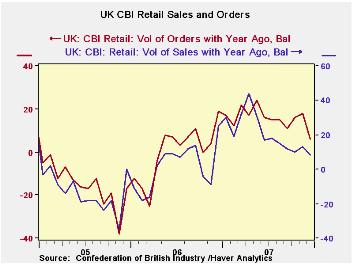

The level of the readings in the chart make a telling

comparison with where they have been in the previous two years and THE

LEVELS speak of current strength -- or better put -- current momentum.

But the steadiness of the slippage is yet another signal and it forms a

dark side of that momentum that sounds a warning for the times ahead.

The expectations for sales and orders in January are off sharply from

December and in truth it is hard to know what to pencil in for February

and that is the number that policy must look to at the moment to sort

out the mess. Is January a rogue and outsized drop? Will February

reverse it? Will February worsen on trend? These are things we do not

know, and as Inspector Clouseau of Pink Panther fame reminds us: ‘we do

not know what we do not know’. So policy must have its hunch and make

its deal with the devil. The question is, of course, which devil? The

CBI report is decidedly mixed and the trend is a call to action. But it

is not clear that the BOE has the wherewithal to answer it, despite

having cut rates once already. It is also far from clear what action is

called for.

| UK Retail volume data CBI Survey | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Reported: | Jan-08 | Dec-07 | Nov-07 | Oct-07 | 12Mo Avg | Pcntle | Max | Min | Range |

| Sales/Year Ago | -- | 8 | 13 | 10 | 21 | 47% | 57 | -35 | 92 |

| Orders/Year Ago | -- | 6 | 18 | 16 | 16 | 55% | 42 | -38 | 80 |

| Sales:Time/Yr | -- | -5 | -3 | 0 | 5 | 41% | 41 | -37 | 78 |

| Stocks: Sales | -- | 24 | 18 | 13 | 13 | 80% | 30 | 0 | 30 |

| Expected: | |||||||||

| Sales/Yr Ago | -5 | 11 | 15 | 16 | 17 | 25% | 49 | -23 | 72 |

| Orders/Yr Ago | -9 | 10 | 12 | 16 | 12 | 35% | 38 | -34 | 72 |

| Sales:Time/Yr | -16 | 3 | 2 | -9 | 4 | 22% | 29 | -29 | 58 |

| Stocks: Sales | 24 | 11 | 12 | 5 | 10 | 100% | 24 | 3 | 21 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief