Global| May 09 2008

Global| May 09 2008U.S. Trade Deficit Narrowed Unexpectedly in March

by:Tom Moeller

|in:Economy in Brief

Summary

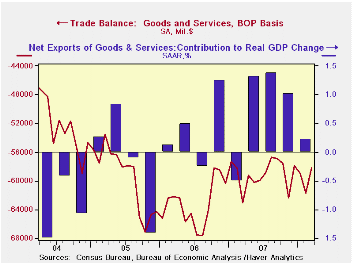

The U.S. foreign trade deficit narrowed unexpectedly to $58.2B in March from $61.7B in February, revised slightly shallower. Consensus expectations had been for a March deficit of $61.2B. So far this year the deficit has averaged [...]

The U.S. foreign trade deficit narrowed unexpectedly to $58.2B in March from $61.7B in February, revised slightly shallower. Consensus expectations had been for a March deficit of $61.2B. So far this year the deficit has averaged $59.6B, slightly deeper than during all of last year.

The weaker U.S. economy, along with the sagging value of the

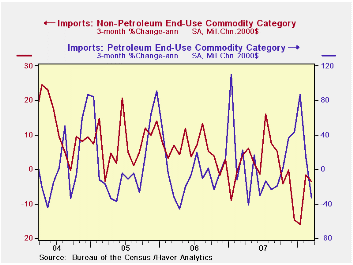

dollar continued to weigh on imports. A 2.9% month to month decline

reflected a 2.7% drop in imports of nonpetroleum products. Measured in

chained 2000 dollars these imports fell 3.6% pulling the year to year

change down to -3.8%. Also in chained dollars, imports of capital goods

reversed all of the February rise with a 2.2% (+3.0% y/y) decline. The

3.2% shortfall in chained imports of nonauto consumer goods was the

third drop in four months and it left them down 4.7% y/y. Real imports

of automotive vehicles & parts fell 9.4% (-10.3% y/y).

Higher oil prices and the weaker U.S. economy together worked to lower the quantity of energy-related petroleum imports by 1.0% (-14.1% y/y) after a 12.8% February drop. The nominal value of petroleum product imports rose 5.7% (41.9% y/y) as crude oil prices rose 6.0% (69.5% y/y) to an average $89.85 per barrel.

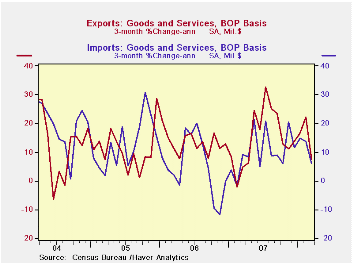

U.S. exports in March gave back their February rise with a

1.7% decline, but the relative strength of foreign economies lifted the

year to year gain to 15.5%. But that firm trend has weakened recently.

Goods exports fell 2.7% in March but in chained dollars they fell by

4.4% (+6.0% y/y). Chained dollar exports of nonauto consumer goods fell

5.7% (+3.3% y/y) after a 1.2% February decline. Exports of industrial

supplies & materials also fell a sharp 4.5% (+10.2% y/y).

Exports of capital goods were down for the fourth month in the last

five, by 3.2% (+6.8% y/y). Exports of civilian aircraft recently have

wobbled. In March they fell 31.9% (+6.1% y/y) for the fourth decline in

the last five months. Exports of computers also fell a sharp 10.5%

(+16.2 y/y). Finally, chained dollar exports of nonauto consumer goods

fell 5.7% (+3.3% y/y) while real automotive exports fell 9.2% (-4.5%

y/y).

The U.S. trade deficit in goods with China improved sharply m/m to $16.1B, the smallest deficit in two years. Imports from China fell 7.0% (-1.3% y/y) for the fourth sharp decline in five months while March exports to China, conversely, rose 10.0% (16.0% y/y). The trade deficit with Europe deepened to $74.5B as exports rose 4.4% y/y and imports rose 2.6%.

Exports of services slipped 0.1% (+15.9% y/y) as travel exports fell 0.1% (+23.0% y/y) and passenger fares rose 1.8% (23.3% y/y).

Services imports fell 0.2% (+12.1% y/y). Travel imports nudged up 0.2% (6.4% y/y) and passenger fares fell 0.4% (+16.9% y/y).

Macroeconomic interdependence and the international role of the dollar from the Federal Reserve Bank of New York can be found here

| Foreign Trade | March | February | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| U.S. Trade Deficit | $58.2B | $61.7B | $63.0B (3/07) | $708.5 | $758.5 | $714.4B |

| Exports - Goods & Services | -1.7% | 1.8% | 15.5% | 12.6% | 12.7% | 10.9% |

| Imports - Goods & Services | -2.9% | 2.6% | 7.9% | 6.0% | 10.4% | 12.9% |

| Petroleum | -5.9% | -5.9% | 40.9% | 9.5% | 20.1% | 39.6% |

| Nonpetroleum Goods | -2.7% | 5.0% | 0.9% | 4.6% | 9.1% | 10.3% |

by Robert Brusca May 9, 2008

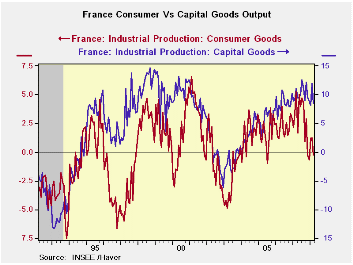

France remains a quintessential e-Zone economy. Its consumer

sector has gone slack but capital goods output is still churning up a

storm. Still capital goods is lagging sector. Its output can tend to

stay strong as its industries turn out goods that are legacy of strong

demand earlier in the cycle; it can lag in recovery as well, as demand

for new equipments waits on the moment that new capital constraints are

encountered. Capital goods is lagging sector in the economy. For this

reason I do not take its ‘enduring strength’ as sign that it will

bootstrap the rest of the economy into expansion.

The chart above shows the longer term relationship between

consumer goods and capital goods output trends in France. History also

tells us that the weakness in the consumer sector is something to be

wary of – the sector tends to be a harbinger.

The banking sector problems in Europe and in France, the

strong euro exchange rate, the slippage in various domestic surveys,

give us even more reason to be wary of what has been ongoing strength

in the capital goods sector. It seems to have become a sector with

increasingly poor fundamentals despite its resilience.

| French IP Excluding construction | |||||||

|---|---|---|---|---|---|---|---|

| Saar except m/m | Mar-08 | Feb-08 | Jan-08 | 3-mo | 6-mo | 12-mo | Quarter-to-date |

| IP total | -0.8% | 0.5% | 0.4% | 0.0% | 2.1% | 1.0% | 1.4% |

| Consumer | -0.8% | 0.2% | 1.7% | 4.4% | -2.3% | -1.6% | 2.1% |

| Capital | -1.1% | 2.0% | 0.0% | 3.7% | 5.2% | 4.9% | 4.7% |

| Intermed | -1.7% | 0.4% | 1.2% | -0.4% | 0.4% | -1.1% | 2.0% |

| Memo | |||||||

| Auto | -2.9% | -2.1% | 1.1% | -14.6% | 2.8% | -1.0% | -1.0% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief