Global| Nov 13 2009

Global| Nov 13 2009U.S. Trade Deficit Increases DueTo Higher Oil Costs, Improved Economy

by:Tom Moeller

|in:Economy in Brief

Summary

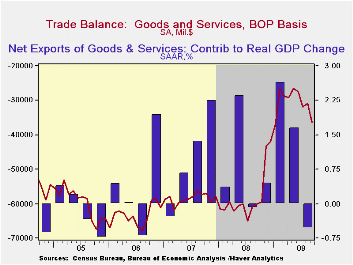

Following months of shrinkage due to lower oil prices and a poor economy, the September U.S. trade deficit widened significantly. The deficit of $36.5B followed a little-revised August figure of $30.8B and the m/m deterioration [...]

Following

months of shrinkage due to lower oil prices and a poor economy, the

September U.S. trade deficit widened significantly. The deficit of

$36.5B followed a little-revised August figure of $30.8B and the m/m

deterioration greatly exceeded Consensus expectations for a deficit of

$31.6B. The latest figure was the deepest trade shortfall

since January. The rise in oil prices is evident in the trade deficit

figures adjusted for inflation. The m/m deterioration in the real

deficit was just under half that for nominal. However, offsetting that

was the improved economy which also lifted the inflation-adjusted

deficit as real imports jumped 6.2% m/m and by 10.1% over the last

three months.

Following

months of shrinkage due to lower oil prices and a poor economy, the

September U.S. trade deficit widened significantly. The deficit of

$36.5B followed a little-revised August figure of $30.8B and the m/m

deterioration greatly exceeded Consensus expectations for a deficit of

$31.6B. The latest figure was the deepest trade shortfall

since January. The rise in oil prices is evident in the trade deficit

figures adjusted for inflation. The m/m deterioration in the real

deficit was just under half that for nominal. However, offsetting that

was the improved economy which also lifted the inflation-adjusted

deficit as real imports jumped 6.2% m/m and by 10.1% over the last

three months.

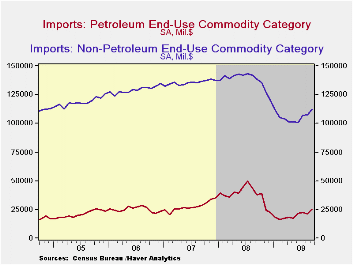

During

September, petroleum imports jumped 20.9% after

having risen by over one-half since February. Higher prices prompted

that increase as crude oil costs rose to a September average of $68.17

per barrel versus the February low of $39.22. Since then crude oil has

risen even further to roughly $75 per barrel. The firmer economy raised

real imports of petroleum products by 6.9% during September and by 7.7%

over the last twelve months. That rise compares to declines of between

one and four percent during each of the last three years.

During

September, petroleum imports jumped 20.9% after

having risen by over one-half since February. Higher prices prompted

that increase as crude oil costs rose to a September average of $68.17

per barrel versus the February low of $39.22. Since then crude oil has

risen even further to roughly $75 per barrel. The firmer economy raised

real imports of petroleum products by 6.9% during September and by 7.7%

over the last twelve months. That rise compares to declines of between

one and four percent during each of the last three years.

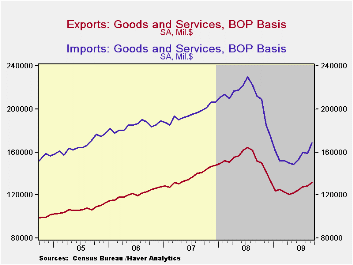

Economic recovery also was apparent in real nonoil imports which rose 4.2% during September and 11.3% during the last three months. These gains lessened the y/y decline to 14.8% from its worst of 24.6%. Real non-auto capital goods imports rose 2.5% (-18.9% y/y) and by 6.7% during the last three months. Real nonauto consumer goods rose 1.9% and 5.5% since June. Both of these increases are turnarounds from sharp declines through June. Real automotive vehicles & parts imports also turned higher by 11.4% (-12.1% y/y) in September and by nearly one-half since June. Despite the lower value of the dollar, economic recovery is further suggested by better travel figures. Imports of services have recently risen, with travel imports strong during three of the last four months as more U.S. residents went abroad.

Reflecting

the competitive value of the dollar, real

merchandise exports during September rose 4.4% (-9.5% y/y) following

three months of 7.0% increase. That's a turnaround from 20% rates of

decline this summer. The chained dollar value of real capital goods

exports led the September increase with a 5.2% gain (-14.3% y/y) which

reversed an August drop. Non-auto consumer goods exports also rose 3.6%

and the y/y decline eased to 5.6% from the peak of -15.7%. Auto exports

were strong for the fourth straight month and the y/y decline of 26.2%

was half its worst reading. Exports of services also have been strong

of late.

Reflecting

the competitive value of the dollar, real

merchandise exports during September rose 4.4% (-9.5% y/y) following

three months of 7.0% increase. That's a turnaround from 20% rates of

decline this summer. The chained dollar value of real capital goods

exports led the September increase with a 5.2% gain (-14.3% y/y) which

reversed an August drop. Non-auto consumer goods exports also rose 3.6%

and the y/y decline eased to 5.6% from the peak of -15.7%. Auto exports

were strong for the fourth straight month and the y/y decline of 26.2%

was half its worst reading. Exports of services also have been strong

of late.

The international trade data can be found in Haver's USECON database. Detailed figures are available in the USINT database.

Trade, Globalization and the Financial Crisis from the Federal Reserve Bank of Dallas is available here.

| Foreign Trade | September | August | July | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| U.S. Trade Deficit | $-36.5 | $30.8B | $31.9B | $60.1B (9/08) | $695.9 | $701.4 | $760.4 |

| Exports - Goods & Services | 2.9 | 0.2% | 2.5% | -13.2% | 11.2% | 13.2% | 13.3% |

| Imports - Goods & Services | 5.8 | -0.4% | 4.9% | -20.6% | 7.6 | 6.0% | 10.8% |

| Petroleum | 20.9 | -5.4% | 3.3% | -31.9% | 37.0% | 9.4% | 20.1% |

| Nonpetroleum Goods | 4.4 | 0.3% | 6.4% | -19.2% | 1.5% | 4.8% | 9.1% |

Michigan Consumer Sentiment Sags Once Again

by Carol Stone November 13, 2009

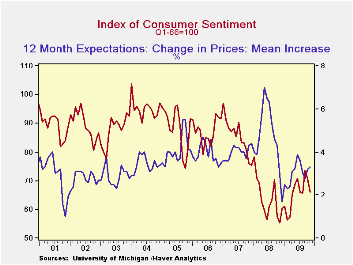

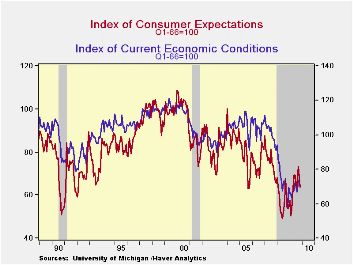

Consumer

sentiment declined again in early November, falling from October's 70.6

to 66.0, measured by the Reuters/University of Michigan Index of

Consumer Sentiment. Forecasters had looked for only a

marginal decrease to 70.0.

Consumer

sentiment declined again in early November, falling from October's 70.6

to 66.0, measured by the Reuters/University of Michigan Index of

Consumer Sentiment. Forecasters had looked for only a

marginal decrease to 70.0.

The reading on expectations for mid-November was down 4.9 points to 63.7 from October's 68.6. The primary weakness came in survey participants' outlook for business conditions over the next year. That had leaped to 88 in September and then fell back in October to 81 and now to 67. This move seems to show that the nice rise in September was a temporary blip, reversed last month and again now. Indeed, November's expectations for "times" to be "good" fell by 7 points and those for "times" to be "bad" increased by 7 points from October's amounts. Expected personal finances were also less optimistic, decreasing by 6 points in this survey round after a 2-point uptick last month. The latest move was related to a rise in the number of people who expect their income to fall during the coming year.

The

reading of current economic conditions also fell; it went

down 4.1 points from October to mid-November. People's

assessments of their current financial condition and business

conditions in general both moved adversely. In particular,

more respondents indicated that current "bad times" make this a "bad

time" to buy large consumer items. At 21, this reading was up

3 points in the month and returned to its level back at the beginning

of this year. The record high for this negative indicator is

24, reached in August 2008. Prior to this cycle, the record was 17 in

October 1992.

The

reading of current economic conditions also fell; it went

down 4.1 points from October to mid-November. People's

assessments of their current financial condition and business

conditions in general both moved adversely. In particular,

more respondents indicated that current "bad times" make this a "bad

time" to buy large consumer items. At 21, this reading was up

3 points in the month and returned to its level back at the beginning

of this year. The record high for this negative indicator is

24, reached in August 2008. Prior to this cycle, the record was 17 in

October 1992.

Expected price inflation during the next year amounted to 3.3% in this mid-November survey, according to the mean of participants' estimates, edging up from October's 3.2%. In contrast, the median of those estimates ticked down from 2.9% to 2.8%, suggesting that people see little overall change in price pressures this month.

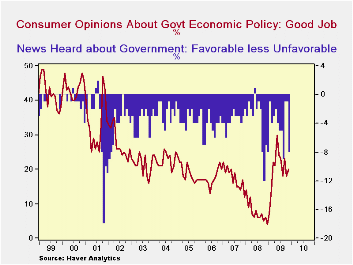

Respondents'

views on government

policy, which may eventually influence economic expectations, showed

mixed developments in this current survey. The number

expressing a favorable opinion rose from 86% in October to 88%,

reflected in a like increase in the number believing government is

doing "a good job" in November. At the same time, the

open-ended query about news reports people have heard gave a negative

spin to their impressions of government; the number hearing favorable

news about government fell from 6% last month to 3% and the number

hearing unfavorable news increased from 7% to 11%. While this

latter "news" reading has hardly ever been positive on a net basis, the

current -8 is well above averages between -3.5 and -4. So

people are clearly uneasy about the news they're getting on government

even though they're feeling marginally better about how government is

working in the economy.

Respondents'

views on government

policy, which may eventually influence economic expectations, showed

mixed developments in this current survey. The number

expressing a favorable opinion rose from 86% in October to 88%,

reflected in a like increase in the number believing government is

doing "a good job" in November. At the same time, the

open-ended query about news reports people have heard gave a negative

spin to their impressions of government; the number hearing favorable

news about government fell from 6% last month to 3% and the number

hearing unfavorable news increased from 7% to 11%. While this

latter "news" reading has hardly ever been positive on a net basis, the

current -8 is well above averages between -3.5 and -4. So

people are clearly uneasy about the news they're getting on government

even though they're feeling marginally better about how government is

working in the economy.

The Reuters/University of Michigan survey data are not seasonally adjusted. The reading is based on telephone interviews with about 500 households at month-end. These mid-month results are based on about 320 interviews. The summary indexes are in Haver's USECON database with details in the proprietary UMSCA database.p

| University of Michigan | Mid-November | October | September | Oct y/y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 66.0 | 70.6 | 73.5 | 18.2% | 63.8 | 85.6 | 87.3 |

| Current Conditions | 69.6 | 73.7 | 73.4 | 21.0 | 73.7 | 101.2 | 105.1 |

| Expectations | 63.7 | 68.6 | 73.5 | 20.4 | 57.3 | 75.6 | 75.9 |

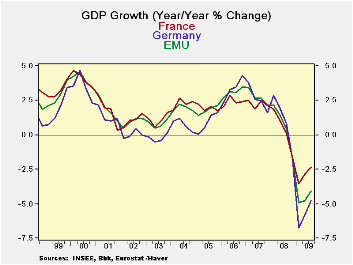

European GDP Turns Higher-But Disappoints

by Robert Brusca November 13, 2009

European GDP turned higher in Q3 but the results were

generally less than expected. Among the early ‘flash’ GDP reporters

France posted a small rise but it was the second rise in a row for

France. Greece with always volatile results posted the strongest rise

followed by Austria. Italy and The Netherlands have the largest Yr/Yr

declines in this group; the EMU Yr/Yr drop is of 4.1%. Greece is lower

Yr/Yr by just 1.6% Austria but just 2.2%. Germany the largest e-Area

economy is off by 4.8% Yr/Yr even though it has two quarters in a row

of solid growth under its belt.

Flash reports do not provide any GDP detail but the various

authorities do offer some account of their results. Both Germany and

France cited the role of exports in pushing growth ahead. In Germany

investment demand was also described as a key factor.

Paragon of strength or parasite of growth?

-- An unfolding theme in the Area is that exports, external demand, is

driving the European recovery. In France domestic demand was flat in

the quarter despite a ton of ongoing stimulus that has left France

unable to get its fiscal budget gap in line as soon as the EU

Commission wants it to. Hungary, in its GDP release today, complained

that exports were weak and that was sapping GDP strength. The largest

industrial economies would seem to be good candidates to spur world

growth with their own domestic demand instead of relying on the demand

increases elsewhere. Chancellor Merkel has defended Germanys ‘right’ to

be a leading exporters, Japan always seeks a surplus to ‘defend’

against the country’s lack of oil and dependence on oil and other

natural resource imports. China’s trade surplus grew larger last month.

How can ‘everyone’ have export led growth? How can the US (whose

current account deficit surged in November) get its deficit in line if

major competitor countries insist on running trade surpluses, spurring

exports and maintaining weak domestic demand at home? This is something

the G-20 has been completely unable to sort out.

These sorts of structural imbalances helped to lead to the

last financial crisis. Such flows underpinned the 1973-78 oil boom-bust

cycle. Factors that put persistent surpluses sand deficits in play are

dangerous and the G-20 has not plan to sort it out. At the weaker

dollar works to mitigate the US imbalance problem even if it is playing

with fire.

| European Growth for Selected Flash GDP Results | ||||||

|---|---|---|---|---|---|---|

| Q/Q Saar | Yr/Yr | |||||

| Q3-09 | Q2-09 | Q1-09 | Q3-09 | Q2-09 | Q1-09 | |

| Austria | 14.0% | -3.7% | -13.8% | -2.2% | -5.4% | -4.8% |

| France | 1.1% | 1.1% | -5.5% | -2.4% | -2.9% | -3.5% |

| Germany | 2.9% | 1.8% | -13.4% | -4.8% | -5.8% | -6.7% |

| Greece | 17.6% | 32.7% | -29.8% | -1.6% | -1.2% | -0.5% |

| Italy | 2.4% | -1.9% | -10.5% | -4.6% | -5.9% | -6.0% |

| Netherlands | 1.7% | -4.0% | -9.4% | -4.0% | -5.1% | -4.2% |

| EMU | 1.5% | -0.7% | -9.6% | -4.1% | -4.8% | -4.9% |

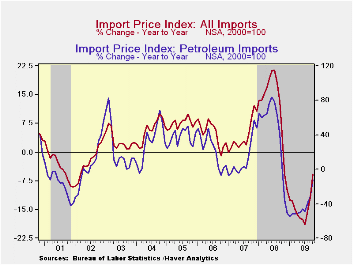

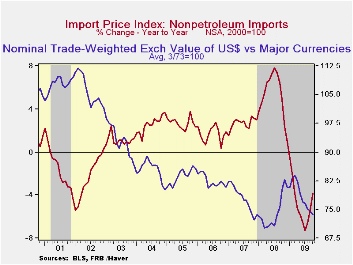

U.S. Import Prices Rise, Both Oil & Nonoil

by Tom Moeller November 13, 2009

The U.S. economy is strengthening, so suggests price pressures

in the foreign trade accounts. Overall import prices rose 0.7%, though

the gain fell short of Consensus expectations for a 1.0% increase. The

rise was led by a 0.9% increase in petroleum prices which reversed a

like decline in September and promises to be followed by another strong

gain this month. The report indicated that non-oil import prices rose

0.7%, which was the strongest monthly increase since June of last year.

Moreover, on a three-month basis, these prices have risen at a 5.7%

annual rate after declining at a 13.6% rate as of last December.

(During the last ten years, there has been a negative 81% correlation

between the nominal trade-weighted exchange value of the US dollar vs.

major currencies and the y/y change in non-oil import prices.)

Import prices break down as follows: Chemical import prices

were quite strong and posted a 2.9% increase but they still were down

16.1% from last year. Iron & steel prices also were strong, up

2.4% m/m, but down by one-third from a year ago. Food prices increased

0.1% and at an 8.0% rate during the last three months. Capital goods

prices similarly posted a modest gain after five months of no change.

Prices for nonauto consumer goods rose 0.3% lifting the three-month

gain to 1.2% versus its weakest reading of -2.6% in January. Durable

consumer goods prices rose 0.4% (-0.9% y/y) but prices of household

goods slipped (-1.9% y/y) and furniture prices fell as well (-1.2%

y/y). Apparel prices were unchanged for the third month (-0.5% y/y).

Petroleum prices reversed their prior month's decline with a 0.9%

increase during October. This month crude oil prices have found further

strength with a rise to $76.94 yesterday from the October average of

$75.82 per barrel.

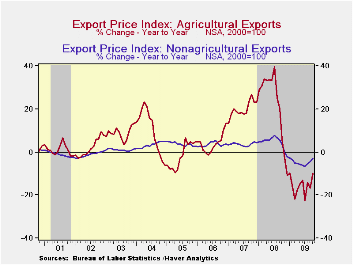

Total export prices resumed increasing modestly. The 0.3% rise was led by a 0.3% gain in nonagricultural export prices, down 2.7% y/y. Agricultural export prices actually fell 1.0% (-10.0% y/y).

The import and export price series can be found in Haver's USECON database. Detailed figures are available in the USINT database.

| Import/Export Prices (NSA, %) | October | September | August | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Import - All Commodities | 0.7 | 0.2 | 1.6 | -5.7 | 11.5 | 4.2 | 4.9 |

| Petroleum | 0.9 | -0.9 | 7.7 | -12.2 | 37.7 | 11.6 | 20.6 |

| Nonpetroleum | 0.7 | 0.4 | 0.3 | -3.8 | 5.3 | 2.7 | 1.7 |

| Export - All Commodities | 0.3 | -0.2 | 0.6 | -3.4 | 6.0 | 4.9 | 3.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief