Global| Dec 14 2004

Global| Dec 14 2004U.S. Trade Deficit a Deeper Than Expected Record in October

by:Tom Moeller

|in:Economy in Brief

Summary

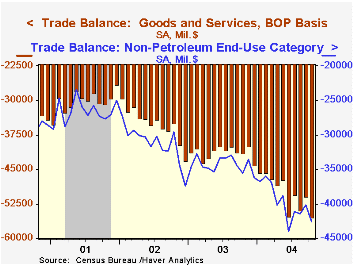

The U.S. foreign trade deficit deepened sharply to $55.5B in October, $4.5B deeper than September which was revised slightly shallower. Consensus expectations had been for a deficit of $52.4B. The latest deficit set a new record and [...]

The U.S. foreign trade deficit deepened sharply to $55.5B in October, $4.5B deeper than September which was revised slightly shallower. Consensus expectations had been for a deficit of $52.4B. The latest deficit set a new record and was $3.6B deeper than the average in 3Q.

Total exports rose just 0.6% following an upwardly revised 1.3% gain in September. Goods exports inched up 0.3% (13.4% y/y) following a 1.7% September surge. Nonauto consumer goods exports fell 0.1% (+16.1% y/y) on the heels of two sizable monthly gains. Capital goods exports rose 0.3% (10.3% y/y).

Total imports reversed the prior month's decline and rose 3.4% due to higher petroleum imports, up 16.9% (+66.8% y/y) reflecting an 11.1% m/m rise in crude oil prices to an average $41.79/bbl. Since then crude oil prices have fallen roughly $12/bbl.

Imports of non-petroleum goods jumped 2.5% (12.4% y/y), driven by a 5.4% (10.5% y/y) surge in nonauto consumer goods. Capital goods imports edged 0.3% (16.7% y/y) higher following a 1.6% rise in September.

The US trade deficit with China deepened to another record of $16.8B ($124.1B in 2003). Exports to China rose 3.0% (5.9% y/y) but imports rose 7.3% (19.8% y/y). The US trade deficit with Japan eased to $5.9B ($66.0B in 2003) but the deficit with the Asian NICs deepened to $2.5B ($21.2B in 2003). The US trade deficit with the European Union deepened to $9.3 B ($97.9B in 2003).

"Offshoring in the Service Sector: Economic Impact and Policy Issues" from the Federal Reserve Bank of Kansas City cab be found here.

| Foreign Trade | Oct | Sept | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Trade Deficit | $55.5B | $50.9B | $41.5B (10/03) | $496.5B | $421.7B | $362.7B |

| Exports - Goods & Services | 0.6% | 1.3% | 11.3% | 4.6% | -3.1% | -6.0% |

| Imports - Goods & Services | 3.4% | -1.1% | 18.5% | 8.5% | 2.1% | -5.5% |

by Tom Moeller December 14, 2004

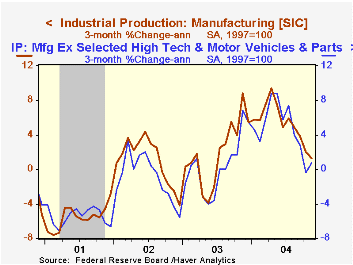

Industrial production rose 0.3% in November following a downwardly revised 0.6% rise the prior month. Consensus expectations had been for a 0.2% rise.

Production in the factory sector rose 0.3% (4.7% y/y). Slower increases recently pulled the three month gain in factory sector production down to 2.0% (AR) versus this year's peak of 8.6% in April. And the slowdown has been broad based. Factory sector output excluding motor vehicles & high tech rose 0.3% in November and the three month growth rate fell to 0.8%.

Though November output in the high tech sector rose a firm 1.1%, the three month growth rate fell to 9.0% versus the peak of 38.2% in August 2003. Excluding high tech, factory output rose 0.3% last month and the three month growth rate fell to 1.2% from this year's peak of 8.2%.

Motor vehicles output fell 0.7% in November but output of appliances, furniture & carpeting rose 1.2% (-0.8% y/y). Clothing output was unchanged m/m and down 2.6% y/y)

Total capacity utilization rose to 77.6% from a downwardly revised October. Capacity grew 1.6% y/y.

"Ringing In the New Year with an Investment Bust?" from the Federal Reserve Bank of St. Louis can be found here.

| Production & Capacity | Nov | Oct | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Industrial Production | 0.3% | 0.6% | 4.2% | 0.3% | -0.6% | -3.4% |

| Capacity Utilization | 77.6% | 77.5% | 75.7% (11/03) | 74.8% | 75.6% | 77.4% |

by Tom Moeller December 14, 2004

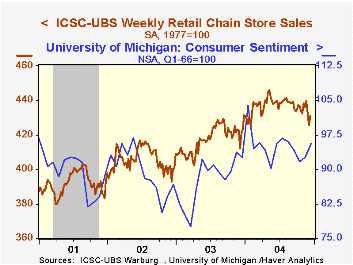

Chain store sales recovered 1.2% during the first full week of December following two weeks of sharp decline, according to the International Council of Shopping Centers (ICSC)-UBS.

Despite the rise, sales so far in December are 1.9% below November.

The leading indicator of chain store sales from ICSC slipped another 0.2% in the latest week for the fourth decline in the last five.

During the last ten years there has been a 60% correlation between y/y change in chain store sales and the change in non-auto retail sales less gasoline.

The ICSC-UBS retail chain-store sales index is constructed using the same-store sales reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

| ICSC-UBS (SA, 1977=100) | 12/11/04 | 12/04/04 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 430.9 | 425.6 | 2.4% | 2.9% | 3.6% | 2.1% |

by Tom Moeller December 14, 2004

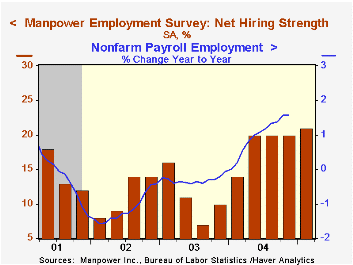

The Manpower Employment Outlook Survey indicated continued improvement in U.S. hiring intentions in 1Q05. A seasonally adjusted net 21% of 16,000 employers expect to increase hiring activity and that was the highest level in four years.

Not seasonally adjusted, 24% of employers planned to raise employment versus 20% in 1Q04 while 10% planned to decrease the number of jobs versus 13% a year ago.

Since 1980 there has been a 74% correlation between the Manpower index and the y/y change in non-farm payrolls.

The latest press release from Manpower Inc. covering global employment prospects can be viewed here..

| Manpower Employment Survey | 1Q '05 | 4Q '04 | 1Q '04 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| All Industries - Net Higher (SA) | 21 | 20 | 14 | 19 | 11 | 11 |

by Tom Moeller December 14, 2004

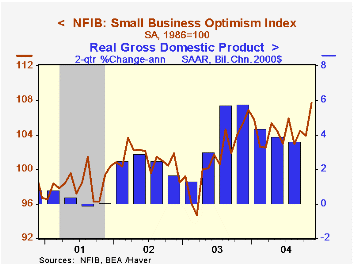

The Small Business Optimism Index for November published by the National Federation of Independent Business (NFIB) surged 3.7% to 107.7 in November, the highest level in twenty years.

During the last ten years there has been a 68% correlation between the level of the NFIB index and the two quarter change in real GDP.

The percentage of firms expecting the economy to improve ballooned to 47%, the highest level since last year and the percent of firms planning to raise employment rose to 19% near last year's high. During the last ten years there has been a 63% correlation between these hiring plans and the three month growth in nonfarm payrolls.

An elevated 35% of firms expected higher real sales in 6 months. The net of firms expecting higher earnings this quarter was stable at -7 and sustained the recent sharp improvement.

The percentage of firms raising average selling prices fell to 18%, well below the averages for 2Q & 3Q.

About 24 million businesses exist in the United States. Small business creates 80% of all new jobs in America.

| Nat'l Federation of Independent Business | Nov | Oct | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Small Business Optimism Index (1986=100) | 107.7 | 103.9 | 2.3% | 101.3 | 101.2 | 98.4 |

by Tom Moeller December 14, 2004

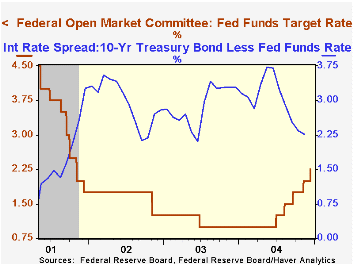

The Federal Open Market Committee raised the target rate for federal funds by 25 basis points to 2.25%, as expected. The discount rate also was raised 25 basis points to 3.25%.

The decision was unanimous.

Today's press release from the Fed continued to contain a comment suggesting that rates could be raised again. "The Committee believes that, even after this action, the stance of monetary policy remains accommodative and, coupled with robust underlying growth in productivity, is providing ongoing support to economic activity."

For the complete text of the Fed's latest press release please click.

"Will the U.S. Productivity Resurgence Continue?" from the Federal Reserve Bank of New York can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief