Global| Nov 10 2009

Global| Nov 10 2009U.S. Small Business OptimismImproves But Credit Remains Tight With Hiring Cautious

by:Tom Moeller

|in:Economy in Brief

Summary

Small business' optimism recently recovered from its recession low, but the latest readings indicate further, modest upside movement. The National Federation of Independent Business (NFIB) indicated that their small business optimism [...]

Small

business' optimism recently recovered from its recession low, but the

latest readings indicate further, modest upside movement. The National

Federation of Independent Business (NFIB) indicated that their small

business optimism index rose to 89.1 during October, the third

consecutive monthly gain. The latest level was the highest since

September '08. During the last ten years, there has been an

85% correlation between the level of the NFIB index and the two-quarter

change in real GDP.

Small

business' optimism recently recovered from its recession low, but the

latest readings indicate further, modest upside movement. The National

Federation of Independent Business (NFIB) indicated that their small

business optimism index rose to 89.1 during October, the third

consecutive monthly gain. The latest level was the highest since

September '08. During the last ten years, there has been an

85% correlation between the level of the NFIB index and the two-quarter

change in real GDP.

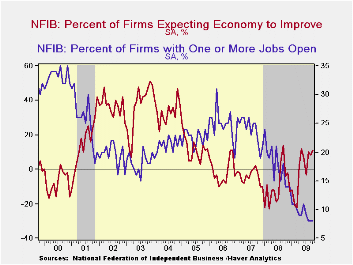

The

percentage of small businesses expecting the

economy to improve bounced back after earlier weakness to 11, the

highest since May. The percentage which thought that now was a good

time to expand the business slipped m/m to a still-improved 7, near the

highest level this year. Moreover, the percent reporting higher

net-earnings this quarter versus last year held at -40 m/m for the

third month, meaning fewer were reporting negative earnings versus last

year. It was the highest level since November.

The

percentage of small businesses expecting the

economy to improve bounced back after earlier weakness to 11, the

highest since May. The percentage which thought that now was a good

time to expand the business slipped m/m to a still-improved 7, near the

highest level this year. Moreover, the percent reporting higher

net-earnings this quarter versus last year held at -40 m/m for the

third month, meaning fewer were reporting negative earnings versus last

year. It was the highest level since November.

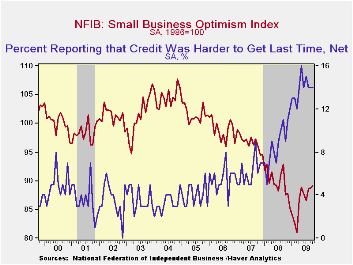

Tight credit conditions continued as 14% of firms indicated that it was harder to get credit. That was near the 1981 high of 15%. Perhaps because of these tight conditions, the recent improvement in business' sentiment has done little, if anything, to improve hiring intentions. The percentage of firms planning to raise employment remained in the net-layoff region and the percentage of firms with one or more job openings held at just 8% during October, the lowest level since 1982. During the last ten years there has been a 74% correlation between the NFIB employment percentage and the six-month change in nonfarm payrolls. Also to the downside, the percentage expecting credit conditions to ease slipped back to the February low.

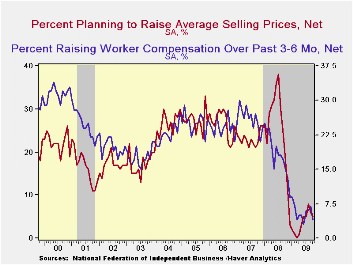

Pricing

conditions eased. The percentage of

firms actually raising prices improved to -17

(indicating deflation) and remained just above the record low. During

the last ten years there has been a 69% correlation between the

six-month change in the producer price index and the level of the NFIB

price index. The percentage of firms planning

to raise prices gave back the prior two months' improvement and fell to

a net 6, though that remained up from the March low of zero. Worker

compensation fell back to near its recent series' low.· The largest,

single most important problems seen by business were poor sales (33%),

taxes (22%, near the highest level since 2007), government requirements

(11%), insurance cost & availability (8%), competition from

large businesses (6%) and inflation (2%).

Pricing

conditions eased. The percentage of

firms actually raising prices improved to -17

(indicating deflation) and remained just above the record low. During

the last ten years there has been a 69% correlation between the

six-month change in the producer price index and the level of the NFIB

price index. The percentage of firms planning

to raise prices gave back the prior two months' improvement and fell to

a net 6, though that remained up from the March low of zero. Worker

compensation fell back to near its recent series' low.· The largest,

single most important problems seen by business were poor sales (33%),

taxes (22%, near the highest level since 2007), government requirements

(11%), insurance cost & availability (8%), competition from

large businesses (6%) and inflation (2%).

About 24 million small businesses exist in the United States. Small business creates 80% of all new jobs in America and the NFIB figures can be found in Haver's SURVEYS database.

Financial Regulation: Past and Future is the title of yesterday's speech by Fed Governor Daniel K. Tarullo and it can be found here here.

| Nat'l Federation of Independent Business | October | September | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Small Business Optimism Index (SA, 1986=100) | 89.1 | 88.8 | 1.8% | 89.8 | 96.7 | 98.9 |

| Percent of Firms Expecting Economic Improvement | 11 | 8 | -4 | -10 | -4 | -1 |

| Percent of Firms With One or More Job Openings | 8 | 8 | 14 | 18 | 24 | 25 |

| Percent of Firms Raising Avg. Selling Pric1es (Net) | -17 | -21 | 15 | 17 | 15 | 20 |

Inflationary Signals Abound;Gold& Oil Prices Strengthen While Dollar Weakens

by Louise Curley November 10, 2009

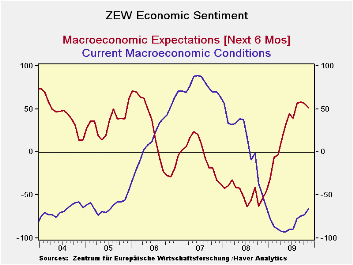

The

ZEW measure of confidence among German institutional investors and

analysts in the macroeconomic outlook six months ahead declined in

November to 51.1 from 56.0 in October. While the extent of

the decline was greater than expected, the optimists on the outlook

still outweigh the pessimists by 51.1%. A year ago the

pessimists outweighed the optimists by 53.5%. Moreover, the

current reading is well above the long term average of

26.9%.

The

ZEW measure of confidence among German institutional investors and

analysts in the macroeconomic outlook six months ahead declined in

November to 51.1 from 56.0 in October. While the extent of

the decline was greater than expected, the optimists on the outlook

still outweigh the pessimists by 51.1%. A year ago the

pessimists outweighed the optimists by 53.5%. Moreover, the

current reading is well above the long term average of

26.9%.

Although

there has been some improvement in the

appraisal of current conditions, the majority of investors and analysts

still view current conditions negatively. The excess of

pessimists over optimists among the respondents declined to 65.6% in

November from 72.2% in October. The first chart shows the two

indicators: the macroeconomic outlook and current

conditions.

Although

there has been some improvement in the

appraisal of current conditions, the majority of investors and analysts

still view current conditions negatively. The excess of

pessimists over optimists among the respondents declined to 65.6% in

November from 72.2% in October. The first chart shows the two

indicators: the macroeconomic outlook and current

conditions.

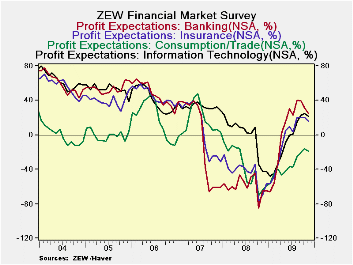

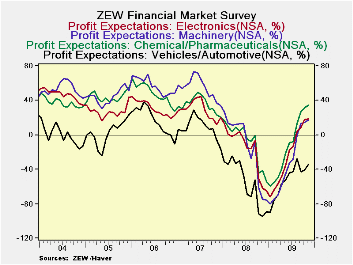

Some of

the reasons why the respondents have

become more cautious about the outlook may be found in their

appraisal of the profit prospects in the thirteen industries regularly

canvassed. In November, the respondents expected declines in

profits in seven of the industries and increases in six.

Declines in profits are expected in Banking, Insurance, Steel and

Metal, Consumption/Trade, Utilities, Telecommunication and Information

Technology. Increases in profits are expected in

Vehicles/Automotive, Chemicals/Pharmaceuticals, Electronics, Machinery,

Construction and Services. Selected industries where profits

are expected to decline are shown in the second chart and selected

industries where profits are expected to increase are shown in the

third chart. Profit expectations in the Banking and Insurance

industries have been declining since August and appear to have had the

biggest negative reappraisal.

Some of

the reasons why the respondents have

become more cautious about the outlook may be found in their

appraisal of the profit prospects in the thirteen industries regularly

canvassed. In November, the respondents expected declines in

profits in seven of the industries and increases in six.

Declines in profits are expected in Banking, Insurance, Steel and

Metal, Consumption/Trade, Utilities, Telecommunication and Information

Technology. Increases in profits are expected in

Vehicles/Automotive, Chemicals/Pharmaceuticals, Electronics, Machinery,

Construction and Services. Selected industries where profits

are expected to decline are shown in the second chart and selected

industries where profits are expected to increase are shown in the

third chart. Profit expectations in the Banking and Insurance

industries have been declining since August and appear to have had the

biggest negative reappraisal.

| ZEW INDICATORS (% Bal.) | Nov 09 | Oct 09 | Nov 08 | M/M Chg | Y/Y Chg | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|---|

| Macroeconomic Expectations 6 Months Ahead | 51.1 | 56.0 | -53.5 | -4.9 | 104.6 | -47.5 | -3.0 | 22.3 |

| Current Conditions | -65.6 | -72.2 | -50.5 | 6.6 | -15.2 | 7.3 | 75.9 | 18.3 |

| PROFIT EXPECTATIONS | ||||||||

| Banking | 24.7 | 31.1 | -64.9 | -9.4 | 89.6 | -59.5 | -3.5 | 47.7 |

| Insurance | 16.4 | 19.8 | -70.1 | -3.4 | 86.5 | -45.4 | 9.7 | 46.0 |

| Chemicals/Pharmaceuticals | 34.8 | 31.6 | -41.6 | 3.2 | 76.4 | -8.6 | 35.3 | 48.3 |

| Vehicles/Automotive | -33.9 | -40.9 | -94.2 | 7.0 | 60.7 | -55.6 | 8.6 | 16.9 |

Inflationary Signals Abound;Gold & Oil Prices Strengthen While Dollar Weakens

by Tom Moeller November 10, 2009

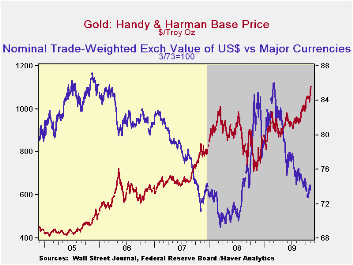

There's

little to suggest that current inflation is a problem for the U.S.

economy as consumer & producer prices remain weak.

Nevertheless, market signals suggest a future problem may be

developing. Higher gold prices are one of the more visible indicators

of pending inflationary power with its rise yesterday to an all-time

high of $1,107 per ounce. That strength has been accompanied by a drop

in the trade-weighted value of the U.S. dollar to its lowest level

since the summer of last year.

There's

little to suggest that current inflation is a problem for the U.S.

economy as consumer & producer prices remain weak.

Nevertheless, market signals suggest a future problem may be

developing. Higher gold prices are one of the more visible indicators

of pending inflationary power with its rise yesterday to an all-time

high of $1,107 per ounce. That strength has been accompanied by a drop

in the trade-weighted value of the U.S. dollar to its lowest level

since the summer of last year.

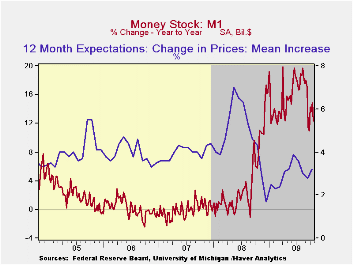

U.S. monetary & fiscal stimulus has done much to generate this inflationary scenario. Low interest rates and the propping up of the banking system have combined to generate an excessive 60% y/y rise in the monetary base and 12% y/y growth in the money supply (M1). Fiscal stimulus is more-than-evident in the budget deficit which ballooned last year to $680 billion and is projected by OMB to be around $1 trillion for the next ten years. Of course, monetization of this deficit is the worry.

The end of

the U.S. recession

and of the recessions abroad have given rise to energy prices which

potentially could fuel higher inflation. Though they are down slightly

from the early-October high, crude oil prices at

an average $79.43 per barrel yesterday were up sharply from the

December low of $32.37. For all of last week the spot market price for

light sweet crude oil averaged $79.04 per barrel.

The end of

the U.S. recession

and of the recessions abroad have given rise to energy prices which

potentially could fuel higher inflation. Though they are down slightly

from the early-October high, crude oil prices at

an average $79.43 per barrel yesterday were up sharply from the

December low of $32.37. For all of last week the spot market price for

light sweet crude oil averaged $79.04 per barrel.

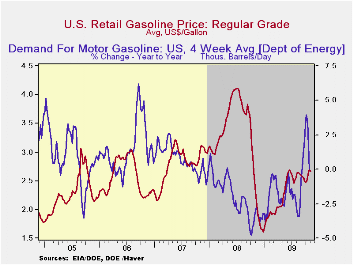

Consumers have seen

this pricing strength, and worries abound. The pump price for

regular gasoline slipped last week to $2.67 per gallon which

was slightly below the June high. However, prices remain up from the

December low of $1.61 and this week the wholesale gasoline price

remained firm at $1.97. Though gas prices were down slightly from the

October high of $2.10, worries abound about the future for pricing

power.  The expected rate of inflation for the next year has risen to

3.2%, roughly double the December low according to the University of

Michigan's survey. Finally, higher gasoline prices have prompted a

cutback in driving. Following earlier strength, the demand for motor

gasoline fell slightly last week from one year earlier. The energy

price figures are reported by the U.S. Department of Energy and can be

found in Haver's WEEKLY & DAILY databases.

The gasoline demand figures are in OILWKLY.

The expected rate of inflation for the next year has risen to

3.2%, roughly double the December low according to the University of

Michigan's survey. Finally, higher gasoline prices have prompted a

cutback in driving. Following earlier strength, the demand for motor

gasoline fell slightly last week from one year earlier. The energy

price figures are reported by the U.S. Department of Energy and can be

found in Haver's WEEKLY & DAILY databases.

The gasoline demand figures are in OILWKLY.

Natural gas prices also have strengthened ahead of the winter heating season. They slipped last week to an average of $4.27 per mmbtu (-36.6% y/y). Though they remained down by two-thirds from the high of $13.19/mmbtu reached in early-July of last year, they are more than double the low reached early last month. A bit of good news for the pricing outlook occurred yesterday. Prices natural gas slipped further to $3.87/mmbtu.

| Weekly Prices | 11/09/09 | 10/19/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Retail Regular Gasoline ($ per Gallon, Regular) | 2.67 | 2.69 | 19.9% | 3.25 | 2.80 | 2.57 |

| Light Sweet Crude Oil, WTI ($ per bbl.) | 79.04 | 78.51 | 22.9% | 100.16 | 72.25 | 66.12 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief