Global| Nov 06 2003

Global| Nov 06 2003U.S. Productivity Surged in 3Q 2003

by:Tom Moeller

|in:Economy in Brief

Summary

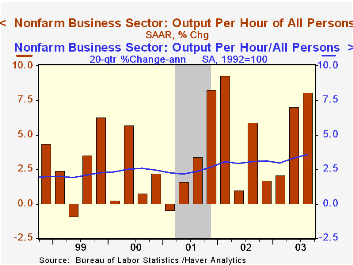

Nonfarm labor productivity growth last quarter surged 8.1%, the fastest rate of growth since 1Q02. Productivity growth in 2Q was revised up slightly. Consensus expectations had been for 3Q growth of 8.0%. Strong growth in recent [...]

Nonfarm labor productivity growth last quarter surged 8.1%, the fastest rate of growth since 1Q02. Productivity growth in 2Q was revised up slightly. Consensus expectations had been for 3Q growth of 8.0%.

Strong growth in recent quarters pulled the five-year growth in productivity to 3.6%, the fastest since the mid-1960s. Combined with 1.2% growth in the labor force over that period it suggests the economy's potential rate of growth is near 5.0%.

Unit labor costs plunged 4.6% in 3Q, the sharpest decline since 1Q02. Compensation per hour was moderate at 3.1%, about the growth rate during the last two years.

Output grew 8.8% (4.1% y/y) last quarter and hours of all persons (employment times hours) rose just 0.7% (-0.6% y/y). Since peaking in three years ago, hours worked have fallen 5.3%.

Manufacturing sector productivity growth surged 8.6% (3.8% y/y) in 3Q. That pulled the five year growth rate to 4.2%. Unit labor costs fell 4.0% (+0.7% y/y).

A report from the Brookings Institution by Barry P. Bosworth and Jack E. Triplett on economic growth and productivity can be found here.

| Nonfarm Business Sector (SAAR) | 3Q '03 | 2Q '03 | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Output per Hour | 8.1% | 7.0% | 4.7% | 5.4% | 1.9% | 3.0% |

| Compensation | 3.1% | 3.6% | 2.7% | 2.8% | 3.6% | 7.0% |

| Unit Labor Costs | -4.6% | -3.2% | -1.9% | -2.4% | 1.7% | 3.9% |

by Tom Moeller November 6, 2003

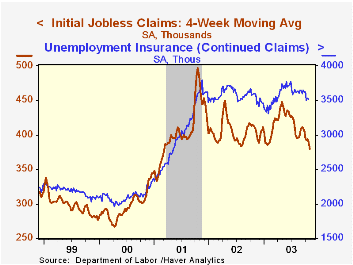

Initial claims for jobless insurance plunged 43,000 to 348,000 last week, the lowest level since January 2001. The modest decline reported initially for the week prior was revised to unchanged. Consensus expectations had been for claims of 385,000.

The four-week moving average of initial claims fell to 380,000 (-7.5% y/y).

Continuing claims for unemployment insurance fell 22,000 and the 57,000 reported initially for the prior week was about halved.

The insured rate of unemployment was stable at 2.8%.

| Unemployment Insurance (000s) | 11/01/2003 | 10/25/2003 | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Initial Claims | 348.0 | 391.0 | -7.2% | 404.3 | 406.0 | 299.7 |

| Continuing Claims | -- | 3,511 | -2.2% | 3,575 | 3,022 | 2,114 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.