Global| Dec 15 2009

Global| Dec 15 2009U.S. PPI Jumps As Fuel CostsSurge; Core Prices Remain Strong

by:Tom Moeller

|in:Economy in Brief

Summary

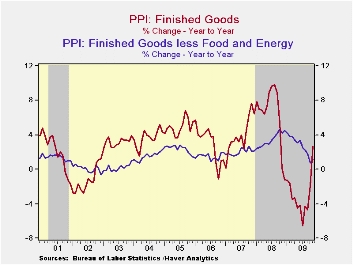

There was a broadening of inflationary pressure last month as measured by the producer price index. The PPI for finished goods jumped 1.8% after the tame 0.3% October increase. The rise was by far the largest increase in months and it [...]

There

was a

broadening of inflationary pressure last month as measured by the

producer price index. The PPI for finished goods jumped 1.8% after the

tame 0.3% October increase. The rise was by far the largest increase in

months and it lifted the y/y gain to 2.7%, its fastest since October of

last year. In addition, the November increase was more-than-double the

Consensus expectation.

There

was a

broadening of inflationary pressure last month as measured by the

producer price index. The PPI for finished goods jumped 1.8% after the

tame 0.3% October increase. The rise was by far the largest increase in

months and it lifted the y/y gain to 2.7%, its fastest since October of

last year. In addition, the November increase was more-than-double the

Consensus expectation.

Higher energy costs led the strength in the PPI last month. The 6.9% increase lifted the y/y increase to 10.6%, its strongest since September 2008. Gasoline prices increased 8.2% (35.9% y/y). Elsewhere, the gain in energy prices was more moderate. Fuel oil prices increased 10.8% but they remained down 7.1% from last year. Natural gas prices also increased a lesser 3.9% and they were down 15.6% from the year ago level. Food prices increased a moderate 0.5% but the increase left prices 1.6% lower than last year. Beef & veal prices were off 8.4% y/y, dairy product prices fell 7.3% and vegetable prices slumped 3.2% y/y.

Excluding

food

& energy prices rose 0.5% and reversed the October decline. The

m/m increase in the core PPI contrasted with expectations for a modest

0.2% increase. The PPI for finished consumer goods less food &

energy rose 0.5% (1.2% y/y) and also reversed the October

decline. Finished durables prices increased 0.6% (0.8% y/y)

while core finished consumer nondurable goods prices rose a modest 0.4%

(2.3% y/y). Capital equipment prices increased for the first time in

three months. The 0.4% increase nevertheless left prices up just 0.4%

y/y, nearly the weakest increase since 2003.

Excluding

food

& energy prices rose 0.5% and reversed the October decline. The

m/m increase in the core PPI contrasted with expectations for a modest

0.2% increase. The PPI for finished consumer goods less food &

energy rose 0.5% (1.2% y/y) and also reversed the October

decline. Finished durables prices increased 0.6% (0.8% y/y)

while core finished consumer nondurable goods prices rose a modest 0.4%

(2.3% y/y). Capital equipment prices increased for the first time in

three months. The 0.4% increase nevertheless left prices up just 0.4%

y/y, nearly the weakest increase since 2003.

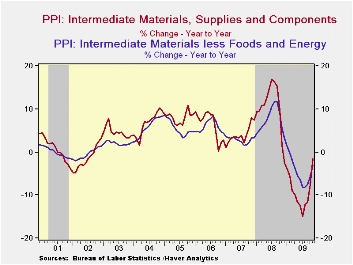

Prices for intermediate

goods jumped 1.4%, reflecting the strength in energy prices. Core

prices also firmed and the 0.3% increase reversed the October decline.

The y/y gain in prices amounted to 0.3% which was a reversal from the

2.4% price deflation at the end of last year. Chemical, lumber and

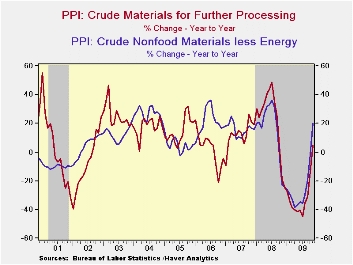

metals prices have firmed. The crude materials PPI again reflected the

strength in energy prices and rose 5.7%. Core prices gave back the

October gain but y/y were up 20.4% due to the improved economy.

Prices for intermediate

goods jumped 1.4%, reflecting the strength in energy prices. Core

prices also firmed and the 0.3% increase reversed the October decline.

The y/y gain in prices amounted to 0.3% which was a reversal from the

2.4% price deflation at the end of last year. Chemical, lumber and

metals prices have firmed. The crude materials PPI again reflected the

strength in energy prices and rose 5.7%. Core prices gave back the

October gain but y/y were up 20.4% due to the improved economy.

The producer price data is available in Haver's USECON database. More detailed data is in the PPI and in the PPIR databases.· Bank Relationships and the Depth of the Current Economic Crisis from the Federal Reserve Bank of San Francisco can be found here.

| Producer Price Index(%) | November | October | September | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Finished Goods | 1.8 | 0.3 | -0.6 | 2.7 | 6.4 | 3.9 | 2.9 |

| Core | 0.5 | -0.6 | -0.1 | 1.2 | 3.4 | 2.0 | 1.5 |

| Intermediate Goods | 1.4 | 0.3 | 0.2 | -1.5 | 10.5 | 4.0 | 6.4 |

| Core | 0.3 | -0.2 | 0.9 | -3.0 | 7.4 | 2.8 | 6.0 |

| Crude Goods | 5.7 | 5.4 | -2.1 | 4.8 | 21.4 | 11.9 | 1.4 |

| Core | -0.8 | 0.5 | 3.6 | 20.4 | 14.8 | 15.6 | 20.8 |

Rising Exports Fuel Rise in Japanese Industrial Production

by Louise Curley December 15, 2009

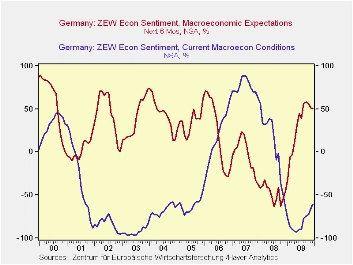

The ZEW

indicator of investors sentiment in Germany declined for the third

month in December. The percent balance of opinion on macro

expectations six months ahead is now at 50.4%, down 7.3 percentage

points from the peak of 57.7% in September. The

current level, however, is well above the long term average

of 27.0%. Although the balance between those respondents who

view current conditions negatively over those who view them positively

is still high at 60.6%, it declined five percentage points in December

and is well below the peak, 92.8%, reached in May of this year when it

was hard to find any optimists. The first chart shows the

percent balances for current conditions and the macro expectations over

the next six months.

The ZEW

indicator of investors sentiment in Germany declined for the third

month in December. The percent balance of opinion on macro

expectations six months ahead is now at 50.4%, down 7.3 percentage

points from the peak of 57.7% in September. The

current level, however, is well above the long term average

of 27.0%. Although the balance between those respondents who

view current conditions negatively over those who view them positively

is still high at 60.6%, it declined five percentage points in December

and is well below the peak, 92.8%, reached in May of this year when it

was hard to find any optimists. The first chart shows the

percent balances for current conditions and the macro expectations over

the next six months.

The survey

is based on the opinions of 277

investors and analysts and took place from November 30 through December

14. During that period, data on new orders, industrial

production and retail sales for October were announced.

Industrial Production was down 1.86%, new orders for manufacturing were

down 2.57%, motor vehicle sales were down 1.37% and retail sales,

excluding motor vehicle sales, were flat. These data

suggested that the economic expansion might be somewhat slower than

earlier expectations and may have dampened some of the optimism of the

participants.

The survey

is based on the opinions of 277

investors and analysts and took place from November 30 through December

14. During that period, data on new orders, industrial

production and retail sales for October were announced.

Industrial Production was down 1.86%, new orders for manufacturing were

down 2.57%, motor vehicle sales were down 1.37% and retail sales,

excluding motor vehicle sales, were flat. These data

suggested that the economic expansion might be somewhat slower than

earlier expectations and may have dampened some of the optimism of the

participants.

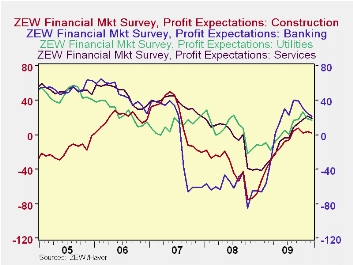

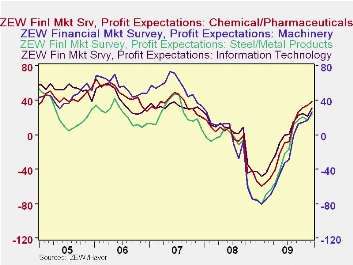

In spite

of the decline in the overall outlook,

participants in the survey are still relatively optimistic regarding

the profit outlook. There are only four industries out of the

thirteen industries surveyed where the current balance of opinion is

for lower profits. These are: banking, construction,

utilities and services. They are shown in the second

chart. Of the remaining industries--insurance,

chemicals/pharmaceuticals, steel/metal, electronics, machinery,

telecommunications, information technology--the balance of opinion is

for higher profits; and for vehicles/automotive and consumption/trade,

the balance of opinion is for smaller losses. The balance of

opinion for higher profits has risen significantly for the information

technology, machinery, steel/metal and chemicals/pharmaceuticals

industries, as can be seen in the third chart.

In spite

of the decline in the overall outlook,

participants in the survey are still relatively optimistic regarding

the profit outlook. There are only four industries out of the

thirteen industries surveyed where the current balance of opinion is

for lower profits. These are: banking, construction,

utilities and services. They are shown in the second

chart. Of the remaining industries--insurance,

chemicals/pharmaceuticals, steel/metal, electronics, machinery,

telecommunications, information technology--the balance of opinion is

for higher profits; and for vehicles/automotive and consumption/trade,

the balance of opinion is for smaller losses. The balance of

opinion for higher profits has risen significantly for the information

technology, machinery, steel/metal and chemicals/pharmaceuticals

industries, as can be seen in the third chart.

| Dec 09 | Nov 09 | Oct 09 | Sep 09 | Aug 09 | Jul 09 | Jun 09 | May 09 | April 09 | |

|---|---|---|---|---|---|---|---|---|---|

| Current Conditions | -60.6 | -65.6 | -72.2 | -74.0 | -77.2 | -89.3 | -89.7 | -92.8 | -91.6 |

| Macro Expectations (6 Months Ahead) | 50.4 | 51.1 | 56.0 | 57.7 | 56.1 | 39.5 | 44.8 | 31.1 | 13.0 |

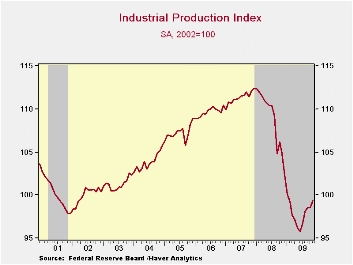

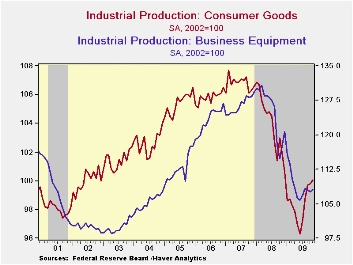

Factory Production Resumes Increase

by Tom Moeller December 15, 2009

Industrial

production resumed the increase that began this past July. The November

0.8% gain followed an unrevised unchanged reading for October and it

exceeded Consensus expectations for a 0.6% rise. The improvement from

October was across-the-board but it was greatest in the construction

supplies and in the materials areas. Output of consumer goods rose a

moderate 0.3% and that was led by a 2.9% (-13.5% y/y) increase in

furniture production and a 1.9% (-6.9% y/y) increase in motor vehicle

output. Output of machinery also rose (-19.7% y/y) as did computers

& electronics (-4.0% y/y) production. Less the motor vehicle

& high-tech sectors output increased 0.8% (-5.1% y/y)

last month.

Industrial

production resumed the increase that began this past July. The November

0.8% gain followed an unrevised unchanged reading for October and it

exceeded Consensus expectations for a 0.6% rise. The improvement from

October was across-the-board but it was greatest in the construction

supplies and in the materials areas. Output of consumer goods rose a

moderate 0.3% and that was led by a 2.9% (-13.5% y/y) increase in

furniture production and a 1.9% (-6.9% y/y) increase in motor vehicle

output. Output of machinery also rose (-19.7% y/y) as did computers

& electronics (-4.0% y/y) production. Less the motor vehicle

& high-tech sectors output increased 0.8% (-5.1% y/y)

last month.

During

November, production increases amongst

industries sagged somewhat to 52.9% of the total from the high of 60.6%

during August. The breadth of increase from last July also dipped to a

still-firm 59.9%, near the strongest since early-2007.

During

November, production increases amongst

industries sagged somewhat to 52.9% of the total from the high of 60.6%

during August. The breadth of increase from last July also dipped to a

still-firm 59.9%, near the strongest since early-2007.

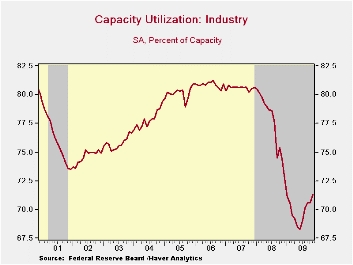

Capacity

utilization rose further to 71.3%, its

highest level since December. In the factory sector alone utilization

rose to 68.4%. Utilization in the primary metals area has risen sharply

to 59.1% with the rebound in output. There's also been a slight rise in

utilization in the machinery area but it's down most elsewhere. The

overall increase was caused by another estimated 0.1% (-0.9% y/y)

decline in industry capacity.

Capacity

utilization rose further to 71.3%, its

highest level since December. In the factory sector alone utilization

rose to 68.4%. Utilization in the primary metals area has risen sharply

to 59.1% with the rebound in output. There's also been a slight rise in

utilization in the machinery area but it's down most elsewhere. The

overall increase was caused by another estimated 0.1% (-0.9% y/y)

decline in industry capacity.

The industrial production data are available in Haver's USECON database.

| Industrial Production (SA,%) | November | October | September | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total Output | 0.8 | 0.0 | 0.5 | -5.2 | -2.2 | 1.5 | 2.3 |

| Manufacturing | 1.1 | -0.2 | 0.6 | -4.8 | -3.2 | 1.4 | 2.5 |

| Consumer Goods | 0.3 | 0.1 | 1.0 | -1.9 | -2.6 | 0.9 | 0.4 |

| Business Equipment | 0.5 | -0.3 | -0.4 | -8.1 | -1.1 | 2.7 | 9.4 |

| Construction Supplies | 1.6 | -1.6 | -1.2 | -12.5 | -6.3 | -2.0 | 2.3 |

| Materials | 1.2 | 0.1 | 0.7 | -4.8 | -1.9 | 2.0 | 2.3 |

| Utilities | -1.8 | 1.6 | 0.3 | -5.1 | 0.3 | 3.4 | -0.6 |

| Capacity Utilization (%) | 71.3 | 70.6 | 70.0 | 74.4 (Nov. '08) | 77.5 | 80.6 | 80.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief