Global| Mar 29 2010

Global| Mar 29 2010U.S. Personal Income & Spending Both Moderate

by:Tom Moeller

|in:Economy in Brief

Summary

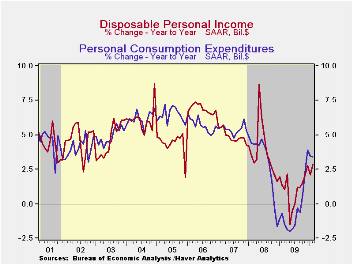

Overall personal income was unchanged in February following a 0.3% January increase, originally reported at 0.1%. The latest reading was the weakest since July and it disappointed Consensus expectations for a 0.1% uptick. Though [...]

Overall personal income was unchanged in

February following a 0.3% January increase, originally reported at

0.1%. The latest reading was the weakest since July and it disappointed

Consensus expectations for a 0.1% uptick. Though moderate, these gains

were enough to lift yearly income growth to 2.0% after the 1.7% decline

in 2009. The three-month rate of increase also improved to 2.8%.

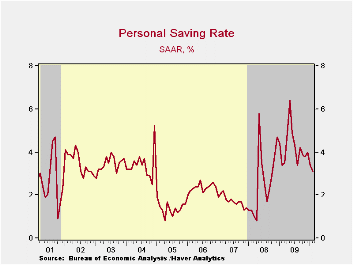

Disposable income was unchanged after January's 0.2% decline. These

moderate income gains caused the savings rate to decline to 3.1%, its

lowest since late-2008. The rate still was up, however, from the 1.0%

low at the beginning of the last recession.

Overall personal income was unchanged in

February following a 0.3% January increase, originally reported at

0.1%. The latest reading was the weakest since July and it disappointed

Consensus expectations for a 0.1% uptick. Though moderate, these gains

were enough to lift yearly income growth to 2.0% after the 1.7% decline

in 2009. The three-month rate of increase also improved to 2.8%.

Disposable income was unchanged after January's 0.2% decline. These

moderate income gains caused the savings rate to decline to 3.1%, its

lowest since late-2008. The rate still was up, however, from the 1.0%

low at the beginning of the last recession.

Moderate employment declines left wages & salaries

unchanged for the second month in the last three. Nevertheless the

modest y/y drop is improved from the sharp 4.0% decline last year.

Wages in the factory sector slipped by 0.2% and the 4.7% y/y decline

was half that during all of last year. In the private service sector

wages ticked up 0.1% for the second month in the last three. Here

again, however, the 1.0% y/y gain is improved versus last year's 3.8%

decline. Working the other, a 0.1% uptick in government sector wages

was behind a deceleration in y/y growth to 2.3%, its lowest since

early-1994.

Moderate employment declines left wages & salaries

unchanged for the second month in the last three. Nevertheless the

modest y/y drop is improved from the sharp 4.0% decline last year.

Wages in the factory sector slipped by 0.2% and the 4.7% y/y decline

was half that during all of last year. In the private service sector

wages ticked up 0.1% for the second month in the last three. Here

again, however, the 1.0% y/y gain is improved versus last year's 3.8%

decline. Working the other, a 0.1% uptick in government sector wages

was behind a deceleration in y/y growth to 2.3%, its lowest since

early-1994.

The weak housing market pulled proprietors' income down 0.6% (+1.9% y/y) for the second consecutive month. Lower interest rates caused interest income also to slip 0.1% but the y/y change of -0.6% was improved from the 5.3% decline during 2009. Dividend income again fell a sharp 2.8% (-11.6% y/y). Finally, unemployment insurance benefits rose 4.2% (54.4% y/y) and offset a January decline.

Personal spending rose 0.3%, down from 0.4% gains during the prior two months. Spending on gasoline fell 1.0% after the 7.3% January jump. Higher prices kept the y/y gain strong at 31.2% but real spending rose just 0.8% y/y. Nominal apparel spending rose a strong 1.2% (0.1% y/y) while spending on home furnishings rose 0.9% (0.5% y/y). That latter decline is improved from a 6.2% drop during all of last year Spending on services continued firm at 2.6% y/y but that was raised by a 4.5% jump in health care expenditures and a 3.1% gain in spending on financial & insurance. Offsetting these gains was a 3.9% decline in spending on motor vehicles & parts (-0.1% y/y).

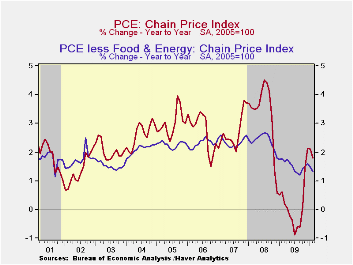

The PCE chain price index slipped modestly with lower gasoline prices. The core PCE price deflator again was unchanged reflecting a 0.6% decline in furniture prices (-1.6% y/y) and a modest 0.3% increase (-4.2% y/y) in appliance prices. Services prices ticked up 0.1% (1.3% y/y) led by a 0.3% gain (2.4% y/y) in health care. Offsetting some of this strength was a 0.5% decline in computer prices (-12.5% y/y) and a 0.7% fall in clothing prices (-0.2% y/y).

The personal income & consumption figures are available in Haver's USECON and USNA databases.

Lessons from the Crisis Stress Tests is the title of last week's speech by Fed Governor Daniel K. Tarullo and it can be found here.

| Disposition of Personal Income (%) | February | January | December | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Personal Income | 0.0 | 0.3 | 0.4 | 2.0 | -1.7 | 2.9 | 5.6 |

| Disposable Personal Income | 0.0 | -0.2 | 0.5 | 2.8 | 1.1 | 3.9 | 4.9 |

| Personal Consumption Expenditures | 0.3 | 0.4 | 0.4 | 3.4 | -0.4 | 3.1 | 5.4 |

| Saving Rate | 3.1 | 3.4 | 4.0 | 3.4 (Feb.'09) | 4.3 | 2.6 | 1.7 |

| PCE Chain Price Index | -0.0 | 0.2 | 0.2 | 1.8 | 0.2 | 3.3 | 2.7 |

| Less food & energy | 0.0 | -0.0 | 0.1 | 1.3 | 1.5 | 2.4 | 2.4 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief