Global| Nov 25 2009

Global| Nov 25 2009U.S. Personal Income GainsMinimally As Spending Recovers

by:Tom Moeller

|in:Economy in Brief

Summary

Negative job growth continued to minimize personal income growth last month. Personal income gained 0.2% during October after an upwardly revised like increase in September. The latest figure matched Consensus expectations. While the [...]

Negative job

growth continued to minimize personal income growth last month. Personal

income gained 0.2% during October after an upwardly revised

like increase in September. The latest figure matched Consensus

expectations. While the gains have been small, they are improved from

early this year due to easier declines in employment which have been

accompanied by higher gov't transfer payments.

Negative job

growth continued to minimize personal income growth last month. Personal

income gained 0.2% during October after an upwardly revised

like increase in September. The latest figure matched Consensus

expectations. While the gains have been small, they are improved from

early this year due to easier declines in employment which have been

accompanied by higher gov't transfer payments.

Wages & salaries were unchanged last month after a revised 0.1% September increase. Year-to-year wages fell 3.6% following a 2.1% increase during 2008. Wages in the factory sector fell 0.5% (-11.2% y/y) after a minimal September decline. In the service sector wages rose just 0.1% (-2.6% y/y), but continuing to offset some of this weakness has been the government sector where wages rose 2.7% y/y.

Growth in unemployment insurance payments has slowed recently. They increased just 0.1% last month after a 10.4% 3Q increase and a 27.4% 2Q gain. Interest income rose 0.5% (-5.6% y/y) as the decline in rates found a bottom while dividend income fell by 0.2% (-21.2% y/y).

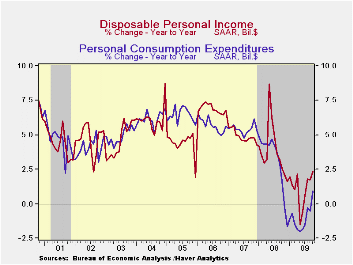

Disposable personal income rose an improved 0.4% due to lower tax payments. Adjusted for inflation real disposable income rose 0.2% after a 0.4% 3Q decline. The saving rate slipped modestly to 4.6% from an upwardly revised 4.6% during September. The rate remained up from last year and more than double the 2007 level due to reduced spending.

Personal

spending gained 0.3% as durables spending increased 0.2%

(0.1% y/y). Spending on motor vehicles recovered 8.6% (3.5% y/y) after

the September drop. That increase was offset by a 0.6% (-4.0% y/y)

decline in spending on furniture & appliances. Spending on

nondurables increased 0.4% (-1.4% y/y) as outlays on apparel rose for

the fourth straight month (0.5% y/y) . Outlays on gasoline rose 0.7%

with higher prices but were down 17.9% from one year ago. Outlays on

services increased 0.5% (1.8% y/y) as spending on health care continued

quite strong posting a 5.6% gain versus last year.

. Outlays on gasoline rose 0.7%

with higher prices but were down 17.9% from one year ago. Outlays on

services increased 0.5% (1.8% y/y) as spending on health care continued

quite strong posting a 5.6% gain versus last year.

The PCE chain price index increased 0.3% during October lifted by a firm 2.1% increase in gasoline costs. Less food-and-energy, "core" prices were again soft and posted just a 0.2% increase. Prices for durable goods rose just 0.1% as home furnishing prices fell (-1.9% y/y) while prices for services gained a steady 1.2% y/y.

The personal income & consumption figures are available in Haver's USECON and USNA databases.

| Disposition of Personal Income (%) | October | September | August | Y/Y | 2008 | 2007 |

|---|---|---|---|---|---|---|

| Personal Income | 0.2 | 0.2 | 0.3 | -1.0 | 2.9 | 5.6 |

| Disposable Personal Income | 0.4 | 0.2 | 0.3 | 2.4 | 3.9 | 4.9 |

| Personal Consumption Expenditures | 0.7 | -0.6 | 1.3 | 0.9 | 3.1 | 5.4 |

| Saving Rate | 4.4 | 4.6 | 3.9 | 2.9 (Oct. '08) | 2.6 | 1.7 |

| PCE Chain Price Index | 0.3 | 0.1 | 0.3 | 0.2 | 3.3 | 2.7 |

| Less food & energy | 0.2 | 0.1 | 0.1 | 1.4 | 2.4 | 2.4 |

U.S. Weekly Initial Claims Insurance For Jobless Insurance Fall To New Low

by Tom Moeller November 25, 2009

The job

market continued to improve last week. The Labor Department reported

that initial claims for unemployment insurance fell to 466,000 from a

downwardly revised 501,000 during the prior week. The latest level was

the lowest since early-September of last year and are down

sharply from the peak reached in March of 674,000 claims. The four-week

moving average of claims fell to 497,000 and the latest weekly figure

was lower than Consensus expectations for 500,000 claims.

The job

market continued to improve last week. The Labor Department reported

that initial claims for unemployment insurance fell to 466,000 from a

downwardly revised 501,000 during the prior week. The latest level was

the lowest since early-September of last year and are down

sharply from the peak reached in March of 674,000 claims. The four-week

moving average of claims fell to 497,000 and the latest weekly figure

was lower than Consensus expectations for 500,000 claims.

Continuing

claims for unemployment insurance during the latest week fell 109,000

to their lowest level since late February. The decline reflects the

improved job market but may also be a function of the exhaustion of

benefits. Continuing claims provide an indication of workers' ability

to find employment. The four-week average of continuing claims fell

modestly to 5,614,750. This series dates back to

1966.

Continuing

claims for unemployment insurance during the latest week fell 109,000

to their lowest level since late February. The decline reflects the

improved job market but may also be a function of the exhaustion of

benefits. Continuing claims provide an indication of workers' ability

to find employment. The four-week average of continuing claims fell

modestly to 5,614,750. This series dates back to

1966.

Extended benefits for unemployment insurance rose fell modestly w/w and averaged 539,531 in early-November versus 550,343 during October.

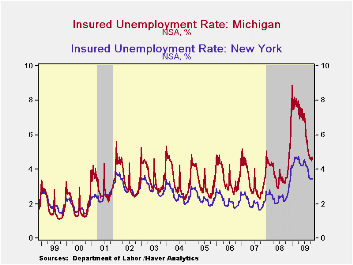

The

insured rate of unemployment fell to 4.1%

and matched its lowest since late-March. The rate reached a high of

5.2% during late-June. During the last ten years, there has been a 93%

correlation between the level of the insured unemployment rate and the

overall rate of unemployment published by the Bureau of Labor

Statistics.

The

insured rate of unemployment fell to 4.1%

and matched its lowest since late-March. The rate reached a high of

5.2% during late-June. During the last ten years, there has been a 93%

correlation between the level of the insured unemployment rate and the

overall rate of unemployment published by the Bureau of Labor

Statistics.

he highest insured unemployment rates in the week ending November 7 were in Puerto Rico (6.2%), Oregon (5.5), Nevada (5.1), Alaska (5.1), Wisconsin (4.9), Pennsylvania (4.9), California (4.7), Michigan (4.6), and South Carolina (4.4). The lowest insured unemployment rates were in North Dakota (1.1%), Virginia (1.9), Texas (2.5), Maine (2.7), Wyoming (2.8), Ohio (3.2), Maryland (2.8), New York (3.5), Mississippi (3.5) and Florida (3.7).

The unemployment insurance claims data is available in Haver's WEEKLY database and the state data is in the REGIONW database.

The minutes to the latest FOMC meeting can be found here.

| Unemployment Insurance (000s) | 11/21/09 | 11/14/09 | 11/07/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Initial Claims | 466 | 501 | 505 | -10.4% | 420 | 321 | 313 |

| ContinuingClaims | -- | 5,423 | 5,613 | 34.9% | 3,342 | 2,552 | 2,459 |

| Insured Unemployment Rate (%) | -- | 4.1 | 4.3 | 3.1(11/2008) | 2.5 | 1.9 | 1.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief