Global| Jun 09 2008

Global| Jun 09 2008U.S. Pending Home Sales in April Rose Unexpectedly

by:Tom Moeller

|in:Economy in Brief

Summary

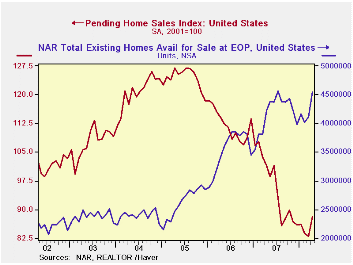

The National Association of Realtors reported that the level of pending sales of existing homes rose an unexpected 6.3% during April. A slight decline in sales had been the Consensus expectation. While a m/m rise in sales is normally [...]

The National Association of Realtors reported that the level of pending sales of existing homes rose an unexpected 6.3% during April. A slight decline in sales had been the Consensus expectation.

While a m/m rise in sales is normally expected due to the warming of temperatures after Winter, the m/m increase was the series' strongest. Nevertheless, sales remained down 13.1% from last April after the 14.6% decline during all of 2007.

These figures are analogous to the new home sales data from

the Commerce Department in that they measure existing home sales when

the sales contract is signed, not at the time the sale is closed. The

series dates back to 2001.

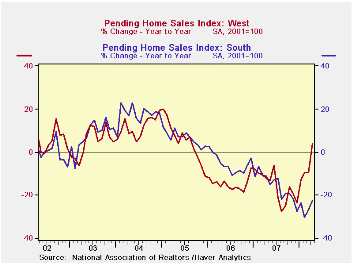

The regional figures indicate a surprising improvement in sales out West which rose 8.3% and by 4.0% y/y. That was the first y/y increase since the middle of 2005. Elsewhere in the country, sales continued to meander with a 1.9% m/m decline in sales in the Northeast. A 13.0% rise in sales in the Midwest left them still down 13.2% from last year as it followed a 10.4% March drop. Sales in the South rose 4.6% m/m but remained down a hefty 22.5% from a year earlier.

The Realtors association indicated in an earlier report that the number of homes on the market & available for sale surged a not seasonally adjusted 10.5% (7.9% y/y) during April. The rise was indeed strong and rivaled past year's April gains. However, it likely reflected a rise usual for the Spring sales season. It followed five months when home inventories declined. As a result the y/y change in the inventory of unsold homes held steady with the prior three months at 7.9% which was down sharply from the 40% growth rates logged during 2006.

At the current sales rate there was an 11.2 months' supply of homes on the market versus an 8.9 months' average during all of last year, a 6.5 months' supply in 2006 and a 4.5 months' supply in 2005. The latest figure was elevated by the low sales rate.

The pending home sales data are available in Haver's PREALTOR database and the number of homes on the market are in the REALTOR database.

| Pending Home Sales (2001=100) | April | March | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total | 88.2 | 83.0 | -13.1% | 95.7 | 112.1 | 124.3 |

| Northeast | 79.3 | 80.8 | -12.3 | 85.6 | 98.5 | 108.3 |

| Midwest | 83.7 | 74.1 | -13.2 | 89.6 | 102.0 | 116.4 |

| South | 88.8 | 84.9 | -22.5 | 107.3 | 127.3 | 134.8 |

| West | 98.8 | 91.2 | 4.0 | 92.1 | 109.5 | 128.6 |

by Robert Brusca June 9, 2008

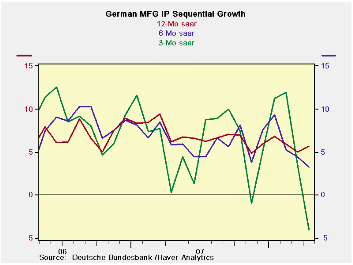

German industrial output in April fell by 0.8% for the second

straight month, held back by dropping construction sector output.

However, the sector indices for consumer goods and intermediate goods

tumbled in April as well. Capital goods output is now down in two of

the last three months and is lower by 1.9% at an annual rate compared

to Q1. Manufacturing IP is flat or lower in the three recent months and

is falling at a 1.3% annual rate in Q2. Manufacturing orders are off

even more sharply, at a 9.3% annual rate in the new quarter.

The signal from orders is clear. It has not yet hit IP with

full force. For now German IP is off in the quarter and more slowing is

coming in the pipeline.

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar exept m/m | Apr-08 | Mar-08 | Feb-08 | 3-mo | 6-mo | 12-mo | Quarter-to-Date |

| IP total | -0.8% | -0.8% | 0.2% | -5.8% | 2.4% | 4.8% | -3.1% |

| Consumer Goods | -2.5% | 0.8% | -0.8% | -9.5% | -2.7% | -0.6% | -4.6% |

| Capital Goods | 1.7% | -2.2% | -0.7% | -4.8% | 5.2% | 8.9% | -1.9% |

| Intermediary Goods | -2.2% | 0.9% | 1.2% | -0.3% | 4.2% | 5.7% | 0.9% |

| Memo | |||||||

| Construction | -2.9% | -13.1% | 3.1% | -42.5% | -2.2% | -2.3% | -38.0% |

| MFG IP | -0.7% | -0.3% | 0.0% | -4.1% | 3.3% | 5.7% | -1.3% |

| MFG Orders | -1.8% | -0.5% | -0.6% | -11.1% | -5.1% | 4.0% | -9.3% |

by Robert Brusca June 9, 2008

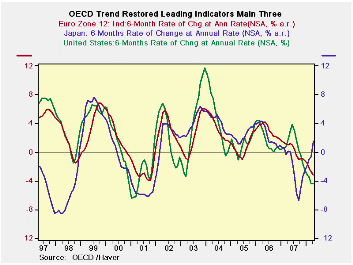

The OECD composite leading indicators (CLIs) show fang growth

trends for the OEC and highly accelerated slowing in the US. The main

regions show an accelerated slowing is in progress, even EMU with a six

month growth rate of -23.1% compared to -1.3% for the previous three

months. Japan alone shows a rebound in place and forceful one with a

current six month growth rate of 4.7% up sharply from -7.2% over the

previous six months.

| OECD Trend-restored leading Indicators | ||||

|---|---|---|---|---|

| Growth progression-SAAR | ||||

| 3-Mos | 6-Mos | 12-Mos | Yr-Ago | |

| OECD | -1.6% | -1.8% | -1.6% | 1.5% |

| OECD7 | -2.7% | -3.1% | -2.6% | 0.5% |

| OECD Europe | -4.8% | -3.3% | -2.3% | 1.2% |

| OECD Japan | 5.0% | 4.7% | -1.5% | 0.0% |

| OECD US | -4.3% | -5.2% | -2.9% | 0.8% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6-Mo Ago | 12-Mo Ago | 18-Mo Ago | |

| OECD | -1.8% | -1.5% | 2.2% | 0.8% |

| OECD7 | -3.1% | -2.0% | 1.2% | -0.2% |

| OECD Europe | -3.3% | -1.3% | 0.9% | 1.5% |

| OECD Japan | 4.7% | -7.2% | 0.0% | -0.1% |

| OECD US | -5.2% | -0.5% | 1.9% | -0.4% |

| Slowdowns indicated by BOLD RED | ||||

by Robert Brusca June 9, 2008

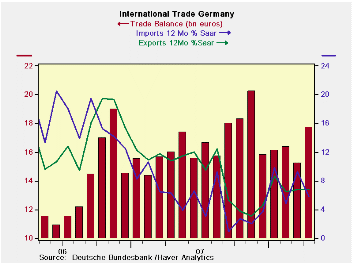

Despite weakening industrial output and fast decelerating

orders German trade flows produced a larger surplus again in April.

Exports rose by 1.2% in the month as imports dropped by a large 2.1%.

Over the last three months import growth is off at an 8% pace, while

for exports growth has decelerated from 6.8% Yr/Yr to 5% over six

months to 1% over 3-months.

The month’s rise in the surplus does not repeal the trend of

fading German export orders. German export trends themselves are still

fading. But the trade balance is, as the name suggests, a balance

between what is bought and what is sold. In April although exports are

still part of a declining trend, imports contracted and did so sharply,

thrusting the trade scene into a surplus.

Weak growth at home is another factor that will come to be

caused by a weakness in exports since Germany’s whole economy is

reliant on trade and on its ability to export. The signals from

weakening orders are due to hit the economy in time. For this month

there is nothing inconsistent about the broad export slowdown trend and

the rise in the trade surplus. The export slowdown is still in place.

| German Trade trends for goods | |||||||

|---|---|---|---|---|---|---|---|

| m/m% | % Saar | ||||||

| Apr-08 | Mar-08 | 3-M | 6-M | 12-M | 12-M Prev | 2-Yr Ago | |

| Balance* | €€ 17.73 | €€ 15.25 | €€ 16.44 | €€ 16.92 | €€ 16.93 | €€ 14.41 | €€ 12.66 |

| EXPORTS | |||||||

| All Exports | 1.2% | -0.8% | 1.0% | 5.0% | 6.8% | 18.3% | 36.1% |

| Capital Goods | -- | -0.8% | 2.8% | 0.6% | 5.0% | 7.3% | 10.7% |

| Motor Vehicles | -- | 0.8% | 6.0% | 5.0% | 7.2% | 10.1% | 9.8% |

| Consumer Goods | -- | -2.3% | 16.7% | 5.6% | 10.2% | 4.3% | 15.3% |

| IMPORTS | |||||||

| All Imports | -2.1% | 0.6% | -8.0% | 8.3% | 5.8% | 12.5% | 34.0% |

| Capital Goods | -- | 2.9% | 44.8% | 7.0% | 8.2% | -3.3% | 23.2% |

| Motor Vehicles | -- | 4.3% | 57.7% | 15.0% | 9.9% | 9.3% | 9.8% |

| Consumer Goods | -- | -4.1% | 6.7% | -2.0% | 0.7% | 3.6% | 21.3% |

| *Eur Blns; mo or period average; Shaded area trends lag one Month | |||||||

by Louise Curley June 9, 2008

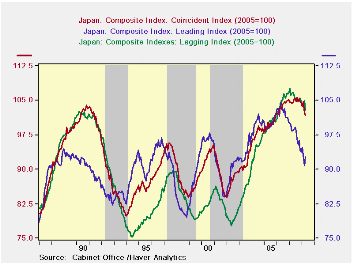

In its assessment of the April, composite leading, lagging and coincident indicators Japan's Cabinet Office remarked that the indicators were "signaling a possible turning point." The first chart, in which we plot the composite indexes for the last 22 years and the Japanese recessions in that period, appears to bear out the Cabinet Office's assessment.

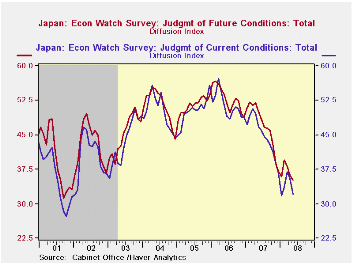

The May survey of the Economy Watchers was also released today. The Economy Watchers have been reducing their appraisals of current and future conditions since early 2006 and their appraisals are now at levels reached in the last recession as can be seen in the second chart.

| JAPAN | May 08 |

Apr 08 |

May 07 |

M/M CHG |

Y/Y CHG |

2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|---|

| Economy Watchers Survey | ||||||||

| Current Conditions | 32.1 | 35.5 | 46.8 | -9.58 | -31.41 | 44.9 | 51.4 | 44.9 |

| Future Conditions | 35.1 | 36.1 | 50.0 | -2.77 | -29.80 | 46.9 | 52.9 | 51.5 |

| Economic Indicators( 2005=100) | Apr 08 |

Mar 08 |

Apr 07 |

M/M CHG |

Y/Y CHG |

2007 | 2006 | 2005 |

| Leading | 92.8 | 90.8 | 98.4 | 2.20 | -5.69 | 97.4 | 102.4 | 100.0 |

| Coincident | 101.7 | 102.4 | 104.4 | -0.68 | -2.59 | 104.8 | 103.8 | 100.0 |

| Lagging | 103.0 | 104.9 | 106.9 | -1.81 | -3.65 | 105.7 | 104.8 | 100.0 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief