Global| Dec 04 2009

Global| Dec 04 2009U.S. Payrolls Decline Minimally and Unemployment Rate Falls Unexpectedly

by:Tom Moeller

|in:Economy in Brief

Summary

The labor market improved last month. Moreover, accompanying data showed that earlier labor market deterioration was not as large as reported initially. The Bureau of Labor Statistics reported that nonfarm payrolls fell 11,000 in [...]

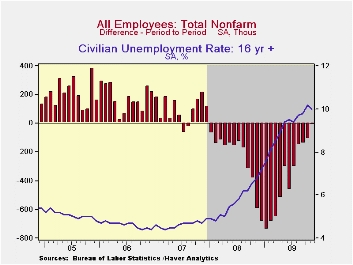

The labor market improved last month. Moreover, accompanying data showed that earlier labor market deterioration was not as large as reported initially. The Bureau of Labor Statistics reported that nonfarm payrolls fell 11,000 in November following smaller, revised declines of 111,000 and 139,000. Last month's payroll employment decline was the shallowest since the recession began in December 2007. Consensus expectations were for a 106,000 worker decline in employment but the range of estimates was an uncommonly wide -50,000 to -170,000.

The payroll employment decline was accompanied by a drop in

the unemployment rate to 10.0% from 10.2%. Perhaps more notable was the

impetus for the decline. Household sector employment increased 227,000

(-3.9% y/y) which was the first monthly gain since April and the

largest since April 2008. The labor force shrank by 98,000 (-0.5% y/y)

as the trend toward dropping out continued. The number of individuals

not in the labor force rose to 82,866,000 (3.3% y/y) with 6,011,000

(11.4% y/y) who want a job now.

The payroll employment decline was accompanied by a drop in

the unemployment rate to 10.0% from 10.2%. Perhaps more notable was the

impetus for the decline. Household sector employment increased 227,000

(-3.9% y/y) which was the first monthly gain since April and the

largest since April 2008. The labor force shrank by 98,000 (-0.5% y/y)

as the trend toward dropping out continued. The number of individuals

not in the labor force rose to 82,866,000 (3.3% y/y) with 6,011,000

(11.4% y/y) who want a job now.

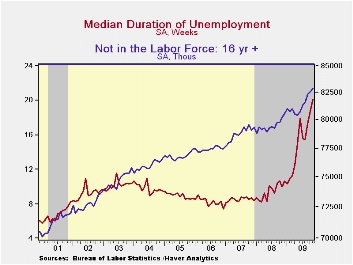

Another signal of an improved labor market was shrinkage in the number of job losers on temporary layoff, off 189,000 or about the same as in October. The number on permanent layoff fell by 272,000 but the level remained nearly double last year. Overall, the total of unemployment plus those part-time for economic reasons fell, but just modestly to 17.2%. Also compromising the picture of labor market improvement was the rise in the median duration of unemployment to a record-high 20.1 weeks. The percent of those unemployed for more than 27 weeks rose to 38.3%.

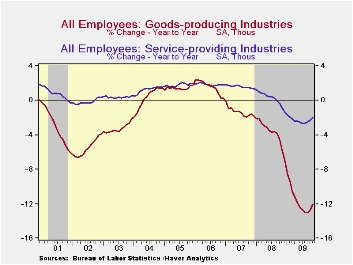

The smaller decline in November payroll employment owed to an

increase in service sector hiring of 58,000. That followed a 2,000

October increase, revised from a 61,000 worker decline reported last

month. The services increase was led by an 86,000 (-4.1% y/y) worker

rise in professional & business services accompanied by a

40,000 (+2.0% y/y) gain in education & health services. Factory

sector employment fell again and the 41,000 worker decline continued a

trend which began in the late-1970s. Construction employment fell but

the 27,000 decline was nearly the smallest since the recession began.

Government sector employment rose just 7,000 (-0.2% y/y). Temporary

help services employment, which may presage future employment growth,

rose 52,400, the fourth consecutive monthly increase.

The smaller decline in November payroll employment owed to an

increase in service sector hiring of 58,000. That followed a 2,000

October increase, revised from a 61,000 worker decline reported last

month. The services increase was led by an 86,000 (-4.1% y/y) worker

rise in professional & business services accompanied by a

40,000 (+2.0% y/y) gain in education & health services. Factory

sector employment fell again and the 41,000 worker decline continued a

trend which began in the late-1970s. Construction employment fell but

the 27,000 decline was nearly the smallest since the recession began.

Government sector employment rose just 7,000 (-0.2% y/y). Temporary

help services employment, which may presage future employment growth,

rose 52,400, the fourth consecutive monthly increase.

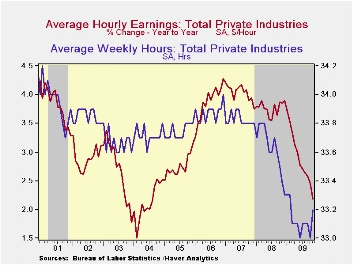

The length of the average workweek, often a harbinger of

future employment, rose to 33.2 weeks, its highest level since

February. The workweek in the factory sector jumped to 40.4 weeks and

the figure has been rising since a May low.

The length of the average workweek, often a harbinger of

future employment, rose to 33.2 weeks, its highest level since

February. The workweek in the factory sector jumped to 40.4 weeks and

the figure has been rising since a May low.

Average hourly earnings increased a minimal 0.1% in November and the gain lowered the y/y increase to 2.2% which was its weakest since mid-2004, off from 4.2% growth reached during 2007. Earnings in the factory sector reversed a revised October decline with a 0.4% increase (+2.5% y/y). The durable sector's earnings rose 3.4% y/y while earnings in the private service sector rose an increased 2.7% y/y. Construction sector earnings rose 2.2% y/y.

The figures referenced above are available in Haver's USECON database. Additional detail can be found in the LABOR and in the EMPL databases.

| Employment: 000s | November | October | September | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Payroll Employment | -11 | -111 | -139 | -3.5% | -0.4% | 1.1% | 1.8% |

| Previous | -- | -190 | -219 | -- | -- | -- | -- |

| Manufacturing | -41 | -51 | -41 | -11.0 | -3.3% | -2.0% | -0.5% |

| Construction | -27 | -56 | -53 | -14.1 | -5.5% | -0.8% | 4.9% |

| Service Producing | 58 | 2 | -44 | -2.0% | 0.2% | 1.6% | 1.8% |

| Average Weekly Hours | 33.2 | 33.0 | 33.1 | 33.4 (Nov. '08) | 33.6 | 33.8 | 33.9 |

| Average Hourly Earnings | 0.1 | 0.3% | 0.1% | 2.2% | 3.8% | 4.0% | 3.9% |

| Unemployment Rate | 10.0 | 10.2% | 9.8% | 6.8% (Nov. '08) | 5.8% | 4.6% | 4.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief