Global| Jun 05 2008

Global| Jun 05 2008U.S. Mortgage Foreclosures Rose Further

by:Tom Moeller

|in:Economy in Brief

Summary

The Mortgage Bankers' Association reported that during the 1st quarter of this year, foreclosures were started on .99% of all mortgages outstanding. That latest level was again by far the highest foreclosure rate on record. [...]

The Mortgage Bankers' Association reported that during the 1st quarter of this year, foreclosures were started on .99% of all mortgages outstanding. That latest level was again by far the highest foreclosure rate on record. Foreclosure rates on both prime and subprime mortgages rose sharply.

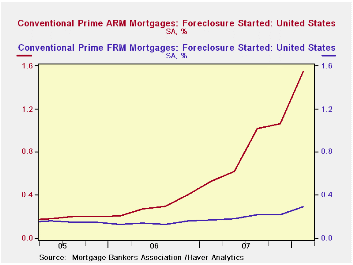

Foreclosures on all prime mortgage loans rose to 0.54% of loans outstanding from 0.41% during 4Q '07. The latest remained nearly double the rate during the prior nine years.

Rates for prime fixed rate mortgages rose slightly to 0.29% of loans outstanding from 0.22% during 4Q. There were 27.7 million of these loans on the books. Of the 6.4 million prime adjustable rate mortgages outstanding, the foreclosure rate rose to 1.55%, up from quarterly rates near 0.2% a few years ago.

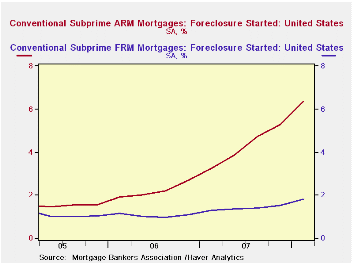

As bad as the above data on prime debt was, the figures on subprime mortgage debt continued far worse. In total, the rate of foreclosure on subprime mortgages rose to 4.06% of outstanding loans during 1Q '08. There were 5.5 million of these loans in the "pool."

The foreclosure rate on subprime fixed rate debt rose to 1.80% of loans outstanding. That was up by more than half from the quarterly running rate in early 2006.There were 2.7 million of these loans outstanding. On variable rate subprime debt foreclosures also surged to 6.35% of loans outstanding from 5.29% during 4Q. There were 2.6 million of these loans on the books.

By the country's regions the Northeast saw an increase in the overall rate of foreclosure to 0.71% last quarter from 0.51% during 1Q '07. In the Midwest that rate rose to 0.98% from 0.79% a year earlier. The West saw an increase to 1.21% of loans outstanding from 0.49% in 1Q '07 and in the South foreclosures were started in 1Q on 0.96% of loans versus 0.54% one year earlier.

Today's testimony by Fed Vice ChairmanDonald L. Kohn, Condition of the Banking System, can be found here

These data series are available in Haver's MBAMTG database.

| Mortgages in Foreclosure (%) | 1Q '08 | 4Q '07 | 1Q '07 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| All Mortgages | 0.99 | 0.83 | 0.58 | 2.84 | 1.84 | 1.64 |

| Conventional Prime | 0.54 | 0.41 | 0.25 | 1.30 | 0.77 | 0.72 |

| Fixed Rate | 0.29 | 0.22 | 0.17 | 0.79 | 0.56 | 0.61 |

| ARM | 1.55 | 1.06 | 0.53 | 3.23 | 1.19 | 0.75 |

| Subprime | 4.06 | 3.44 | 2.43 | 11.71 | 7.23 | 5.66 |

| Fixed Rate | 1.80 | 1.52 | 1.30 | 5.55 | 4.24 | 4.33 |

| ARM | 6.35 | 5.29 | 3.23 | 17.08 | 8.80 | 6.07 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief