Global| Jan 28 2009

Global| Jan 28 2009U.S. Mortgage Applications Fall as Refinancing Boom Ends

by:Tom Moeller

|in:Economy in Brief

Summary

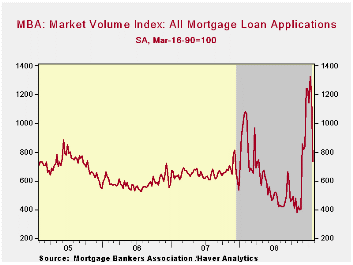

According to the Mortgage Bankers Association, the total number of mortgage applications fell by more than one-third last week and since their peak two weeks ago are down by almost one-half. Applications had been boosted by lower [...]

According to

the Mortgage Bankers Association, the total number of mortgage

applications fell by more than one-third last week and since their peak

two weeks ago are down by almost one-half. Applications had

been boosted by lower interest rates which have risen 25 to 30 basis

points on average.

According to

the Mortgage Bankers Association, the total number of mortgage

applications fell by more than one-third last week and since their peak

two weeks ago are down by almost one-half. Applications had

been boosted by lower interest rates which have risen 25 to 30 basis

points on average.

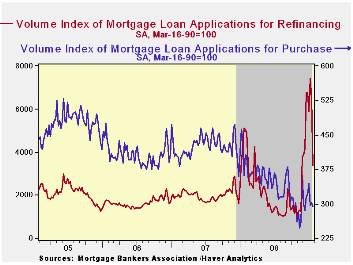

The index of applications to refinance a home mortgage fell by more than one-half during the last two periods.

Applications for a mortgage to purchase a home also fell but the decline only reversed an increase during the prior week. Since their peak early last year applications are down 25%.

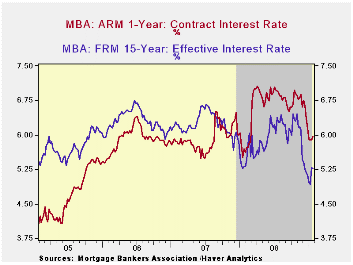

The

effective interest rate on a conventional 15-year

mortgage was roughly stable week-to-week at 5.27% which was up from the

low of 4.92% during the week prior. For a 30-year mortgage, rates also

were roughly stable w/w at 5.43%, up from the low of 5.13% two weeks

ago. Interest rates on 15 and 30 year mortgages are closely correlated

(>90%) with the rate on 10-year Treasury securities. For an

adjustable 1-Year mortgage, the rate also held about steady for the

fourth week at 5.97%, down a full percentage point from this past

Fall.

The

effective interest rate on a conventional 15-year

mortgage was roughly stable week-to-week at 5.27% which was up from the

low of 4.92% during the week prior. For a 30-year mortgage, rates also

were roughly stable w/w at 5.43%, up from the low of 5.13% two weeks

ago. Interest rates on 15 and 30 year mortgages are closely correlated

(>90%) with the rate on 10-year Treasury securities. For an

adjustable 1-Year mortgage, the rate also held about steady for the

fourth week at 5.97%, down a full percentage point from this past

Fall.

During the last ten years there has been a (negative) 79% correlation between the level of applications for purchase and the effective interest rate on a 30-year mortgage. Moreover, during the last ten years there has been a 61% correlation between the y/y change in purchase applications and the change in new plus existing single family home sales.

The

figures for weekly mortgage applications are

available in Haver's SURVEYW

database.

The

figures for weekly mortgage applications are

available in Haver's SURVEYW

database.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey covers roughly 50% of all U.S. residential mortgage applications processed each week by mortgage banks, commercial banks and thrifts. Visit the Mortgage Bankers Association site here.

The Congressional Budget Office Cost Estimate of the American Recovery and Reinvestment Act of 2009 can be found here.

| MBA Mortgage Applications (3/16/90=100) | 01/23/09 | 01/16/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total Market Index | 732.1 | 1,195.3 | -30.6% | 642.9 | 652.6 | 584.2 |

| Purchase | 294.3 | 303.1 | -18.7% | 345.4 | 424.9 | 406.9 |

| Refinancing | 3,373.9 | 6,491.8 | -33.9% | 2,394.1 | 1,997.9 | 1,634.0 |

by Robert Brusca January 28, 2009

While business sentiment is falling to new lows and very low lows in Italy , the good news is that the pace of decline is letting up. Italy ’s businesses are clearly in bad shape and concerned. But maybe the rate of deterioration and adverse assessment is slowing down.

In the table below we rank the various components of this measure since 1996 and we find for just about very category there is a new low being made. Inventories are the sole exception and there the bad news is that inventories are generally regarded as high.

In Italy , Silvio Berlusconi's government has approved a stimulus package to kick-start the economy with measures it says are worth 80 billion Euros, but this program largely recycles existing funds and the plan has failed to lift the pessimism that has imbued the Italian economy.

The Italian results fit in with a new leading index result for Europe that finds conditions are still set to deteriorate further. Confidence a for businesses and consumers is still generally either very low and stuck three or has declined across most of the e-Zone.

| Italy ISAE Business Sentiment | ||||||

|---|---|---|---|---|---|---|

| Since Oct 1996 | ||||||

| Jan-09 | Dec-08 | Nov-08 | Oct-08 | Percentile | Rank | |

| Biz Confidence | 65.5 | 66.8 | 71.7 | 76.5 | 0.0 | 148 |

| TOTAL INDUSTRY | ||||||

| Order books & Demand | ||||||

| Total | -58 | -54 | -45 | -38 | 0.0 | 148 |

| Domestic | -63 | -58 | -47 | -39 | 0.0 | 148 |

| Foreign | -59 | -54 | -44 | -33 | 0.0 | 148 |

| Inventories | 9 | 9 | 8 | 6 | 83.3 | 14 |

| Production | -55 | -46 | -37 | -29 | 0.0 | 148 |

| INTERMEDIATE | ||||||

| Order books & Demand | ||||||

| Total | -74 | -68 | -52 | -42 | 0.0 | 148 |

| Domestic | -74 | -69 | -53 | -40 | 0.0 | 148 |

| Foreign | -73 | -67 | -50 | -38 | 0.0 | 148 |

| Inventories | 12 | 7 | 10 | 9 | 93.1 | 4 |

| Production | -65 | -58 | -43 | -29 | 0.0 | 148 |

| INVESTMENT GOODS | ||||||

| Order books & Demand | ||||||

| Total | -62 | -62 | -52 | -39 | 0.0 | 147 |

| Domestic | -65 | -64 | -56 | -44 | 0.0 | 148 |

| Foreign | -54 | -56 | -45 | -27 | 2.5 | 147 |

| Inventories | 7 | 9 | 11 | 6 | 63.2 | 40 |

| Production | -54 | -50 | -41 | -28 | 0.0 | 148 |

| CONSUMER GOODS | ||||||

| Order books & Demand | ||||||

| Total | -47 | -36 | -32 | -33 | 0.0 | 148 |

| Domestic | -48 | -39 | -32 | -34 | 0.0 | 148 |

| Foreign | -54 | -42 | -36 | -32 | 0.0 | 148 |

| Inventories | 7 | 10 | 5 | 3 | 69.2 | 35 |

| Production | -42 | -28 | -27 | -29 | 0.0 | 148 |

| Total number of months: | 148 | |||||

FOMC Leaves Rates Unchanged

by Tom Moeller January 28, 2009

The

Federal Open Market Committee today left the Federal funds rate in a

"range from 0 to 1/4 percent." The discount also was left unchanged at

0.50%. The Fed funds rate remained the lowest ever and the lack of

action at this meeting was generally anticipated by economists.

The

Federal Open Market Committee today left the Federal funds rate in a

"range from 0 to 1/4 percent." The discount also was left unchanged at

0.50%. The Fed funds rate remained the lowest ever and the lack of

action at this meeting was generally anticipated by economists.

Regarding economic growth, the Fed indicated that "the economy has weakened further. Industrial production, housing starts, and employment have continued to decline steeply, as consumers and businesses have cut back spending ... The Committee anticipates that a gradual recovery in economic activity will begin later this year, but the downside risks to that outlook are significant."

Regarding inflation it was indicated that "the Committee sees some risk that inflation could persist for a time below rates that best foster economic growth and price stability in the longer term."

The Fed

emphasized its concern about the recent turmoil in the credit markets.

"The Federal Reserve will employ all available tools to promote the

resumption of sustainable economic growth and to preserve price

stability ... The Federal Reserve continues to purchase large

quantities of agency debt and mortgage-backed securities to provide

support to the mortgage and housing markets, and it stands ready to

expand the quantity of such purchases and the duration of the purchase

program as conditions warrant. The Committee also is prepared

to purchase longer-term Treasury securities if evolving circumstances

indicate that such transactions would be particularly effective in

improving conditions in private credit markets."

The Fed

emphasized its concern about the recent turmoil in the credit markets.

"The Federal Reserve will employ all available tools to promote the

resumption of sustainable economic growth and to preserve price

stability ... The Federal Reserve continues to purchase large

quantities of agency debt and mortgage-backed securities to provide

support to the mortgage and housing markets, and it stands ready to

expand the quantity of such purchases and the duration of the purchase

program as conditions warrant. The Committee also is prepared

to purchase longer-term Treasury securities if evolving circumstances

indicate that such transactions would be particularly effective in

improving conditions in private credit markets."

The decision was unanimous amongst FOMC voters except that Jeffrey M. Lacker, President of the Federal Reserve Bank of Richmond, preferred to expand the monetary base at this time by purchasing U.S. Treasury securities rather than through targeted credit programs.

For the complete text of the Fed's latest press release please follow this link.

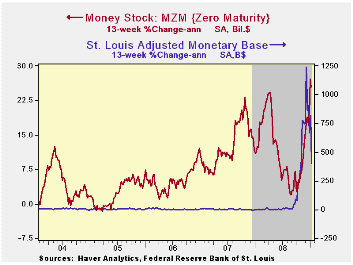

Growth in economic liquidity has risen.  The money stock measure M2 rose

at a 17.0% rate over the last three months, up from a 5% growth rate

earlier this year. The level of demand deposits has surged by

two-thirds since the Spring. In addition, the monetary base

has roughly doubled since last Spring. At the same

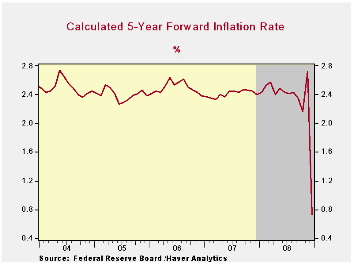

time, inflation expectations have fallen sharply.

The money stock measure M2 rose

at a 17.0% rate over the last three months, up from a 5% growth rate

earlier this year. The level of demand deposits has surged by

two-thirds since the Spring. In addition, the monetary base

has roughly doubled since last Spring. At the same

time, inflation expectations have fallen sharply.

The Haver databases USECON, WEEKLY and DAILY contain the figures from the Federal Reserve Board.

Need to Fix Banking Sector for Stimulus to Work is a recent article published in the IMF Survey Magazine: In the News and it can be found here.

Money, Liquidity, and Monetary Policy from the Federal Reserve Bank of New York is available here.

| Current | Last | November | 2008 | 2007 | 2006 | |

|---|---|---|---|---|---|---|

| Federal Funds Rate, % (Target) | 0.00 - 0.25 | 0.00 - 0.25 | 0.39 | 1.93 | 5.02 | 4.96 |

| Discount Rate, % | 0.50 | 0.50 | 1.25 | 2.39 | 5.86 | 5.96 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief