Global| Dec 17 2009

Global| Dec 17 2009U.S. Initial JoblessInsurance Claims Unexpectedly Rise To Highest In One Month

by:Tom Moeller

|in:Economy in Brief

Summary

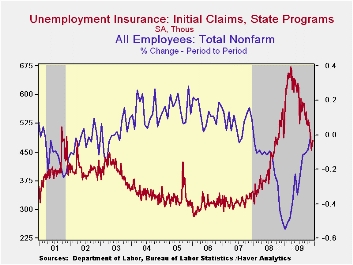

Recent steadying in the job market stalled last week. The Labor Department indicated that initial claims for unemployment insurance rose to 480,000 from a little-revised 473,000 during the prior week. As a result, claims reached the [...]

Recent

steadying in the job market stalled last week. The Labor Department

indicated that initial claims for unemployment insurance rose to

480,000 from a little-revised 473,000 during the prior week. As a

result, claims reached the highest level in four weeks but remained

down from the recession peak of 674,000 hit in March. The four-week

moving average of claims slipped to 467,500 and the latest weekly

figure was higher than Consensus expectations for a decline to 465,000

claims.

Recent

steadying in the job market stalled last week. The Labor Department

indicated that initial claims for unemployment insurance rose to

480,000 from a little-revised 473,000 during the prior week. As a

result, claims reached the highest level in four weeks but remained

down from the recession peak of 674,000 hit in March. The four-week

moving average of claims slipped to 467,500 and the latest weekly

figure was higher than Consensus expectations for a decline to 465,000

claims.

Initial

claims during the latest week cover the survey period

for November nonfarm payrolls. Claims fell 21,000 (4.2%) from the same

week in October. During the last ten years there has been a negative

84% correlation between the level of claims and the m/m change in

nonfarm payrolls.· Continuing claims for unemployment insurance during

the latest week ticked up 5,000 after a little-revised 289,000 decline

during the week prior. Continuing claims were at the lowest level since

late-February. The overall decline is a function of the improved job

market but also reflects the exhaustion of unemployment benefits.

Continuing claims provide an indication of workers' ability to find

employment. The four-week average of continuing claims fell to

5,318,250. This series dates back to 1966.

Initial

claims during the latest week cover the survey period

for November nonfarm payrolls. Claims fell 21,000 (4.2%) from the same

week in October. During the last ten years there has been a negative

84% correlation between the level of claims and the m/m change in

nonfarm payrolls.· Continuing claims for unemployment insurance during

the latest week ticked up 5,000 after a little-revised 289,000 decline

during the week prior. Continuing claims were at the lowest level since

late-February. The overall decline is a function of the improved job

market but also reflects the exhaustion of unemployment benefits.

Continuing claims provide an indication of workers' ability to find

employment. The four-week average of continuing claims fell to

5,318,250. This series dates back to 1966.

Extended

benefits for unemployment insurance retraced much of the prior week's

decline with a rise to 503,100 during the fourth week of November. The

latest compares to 550,343 during all of October.

Extended

benefits for unemployment insurance retraced much of the prior week's

decline with a rise to 503,100 during the fourth week of November. The

latest compares to 550,343 during all of October.

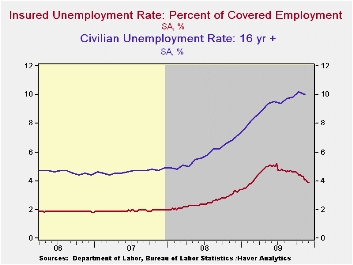

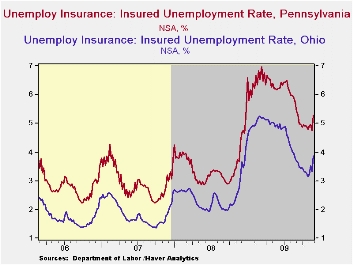

The insured rate of unemployment remained stable at 3.9%, the lowest level since February. The rate reached a high of 5.2% during late-June. During the last ten years, there has been a 93% correlation between the level of the insured unemployment rate and the overall rate of unemployment published by the Bureau of Labor Statistics. · The highest insured unemployment rates in the week ending November 28 were in Wisconsin (6.4), Oregon (6.3), Alaska (6.2), Nevada (5.5), Puerto Rico (5.5%), Pennsylvania (5.3), Michigan (5.3), California (4.9) and South Carolina (4.8). The lowest insured unemployment rates were in North Dakota (1.6%), Virginia (2.2), Texas (2.6), Maine (3.1), Wyoming (3.2), Maryland (3.2), Mississippi (3.7), New York (3.8), Florida (3.8) and Ohio (3.9). The data are not seasonally adjusted but the overall insured unemployment rate is.· The unemployment insurance claims data is available in Haver's WEEKLY database and the state data is in the REGIONW database.

| Unemployment Insurance (000s) | 12/12/09 | 12/05/09 | 11/28/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Initial Claims | 480 | 473 | 454 | -13.0% | 420 | 321 | 313 |

| Continuing Claims | -- | 5,186 | 5,181 | 19.1% | 3,342 | 2,552 | 2,459 |

| Insured Unemployment Rate (%) | -- | 3.9 | 3.9 | 3.3 (12/2008) | 2.5 | 1.9 | 1.9 |

by Tom Moeller December 17, 2009

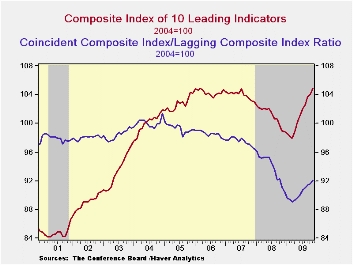

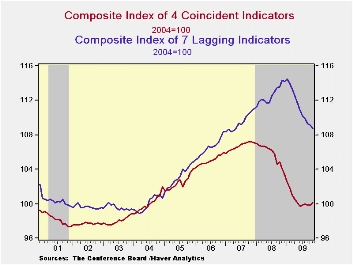

The Conference Board's Index of Leading Economic Indicators continued its uptrend last month giving a strong signal that the recent recession has ended. The 0.9% rise during November was the eighth consecutive monthly increase. Moreover, the 10.2% (centered) rate of increase during the last six months was nearly the strongest since early-1983. The leading index is based on actual reports for eight economic data series. The Conference Board initially estimates two series, consumer and capital goods orders.

The breadth of increase amongst the component series sagged

again last month. Sixty-five percent of the components rose during

November versus last month's reading of 70% that increased. During the

most recent six months, however, 80% of the series rose. Prominent in

last month's increase was a longer workweek, fewer jobless insurance

claims, more building permits, and the steeper interest rate yield

curve. These gains were offset by easier vendor performance, lower

consumer expectations and a downtick in capital goods orders.

Continuing to suggest that the rate of decline in the economy is slowing were the coincident indicators which rose for the first month in the last three. The 0.2% gain followed an unrevised no-change during October. During the last six months the 1.4% rate of decline in the coincident series compares with a shortfall of 8.0% at its worst in January. Moderation of earlier declines has been due to higher industrial production, higher real personal income and higher business sales as well as easier declines in payroll employment.

In a continued sign that excesses in the U.S. economy are falling, the lagging index has been falling since January. Leading the decline has been lower commercial & industrial loans outstanding as well as slower growth in labor costs and less consumer credit. The ratio of coincident-to-lagging indicators (another leading indicator) also continued higher for the eighth straight month to the highest level since November.

The Conference Board figures are available in Haver's BCI database. Visit the Conference Board's site for coverage of leading indicator series from around the world.

| Business Cycle Indicators (%) | November | October | September | August 6-Month % (AR) | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Leading | 0.9 | 0.3 | 1.2 | 10.2 | -2.8 | -0.3 | 1.5 |

| Coincident | 0.2 | 0.0 | -0.1 | -1.4 | -0.9 | 1.6 | 2.5 |

| Lagging | -0.4 | -0.2 | -0.5 | -6.3 | 2.9 | 2.8 | 3.3 |

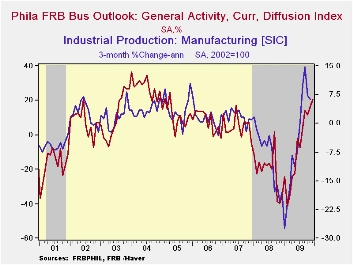

Philadelphia Fed Index Gains With Strength in Employment

by Tom Moeller December 17, 2009

The

Philadelphia Federal Reserve Bank indicated that its index of regional

factory sector activity rose this month to its highest level since

early-2005. At 20.5, the index was unexpectedly strong and positive for

the fifth consecutive month. The latest level compared to figures near

-40.0 this past fall and winter.

The

Philadelphia Federal Reserve Bank indicated that its index of regional

factory sector activity rose this month to its highest level since

early-2005. At 20.5, the index was unexpectedly strong and positive for

the fifth consecutive month. The latest level compared to figures near

-40.0 this past fall and winter.

During the

last ten years there has

been a 77% correlation between the level of the Philadelphia Fed

Business Conditions Index and the three-month growth in factory sector

industrial production. There has been a 70% correlation with q/q growth

in real GDP. The latest survey from the Philadelphia Federal Reserve

Bank can be found here.·

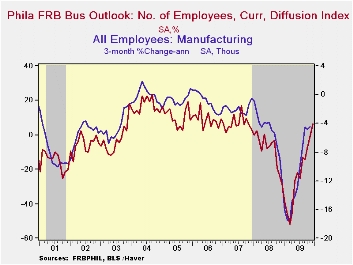

Amongst the components, the employment index was notably strong as it

rose to well above break-even and to the highest level since late-2007.

During the last ten years there has been a 91% correlation between the

index level and the three-month change in manufacturing sector

payrolls. Remaining strong were shipments, the workweek, unfilled

orders and the delivery times components. The inventory component also

improved significantly from its March low.

During the

last ten years there has

been a 77% correlation between the level of the Philadelphia Fed

Business Conditions Index and the three-month growth in factory sector

industrial production. There has been a 70% correlation with q/q growth

in real GDP. The latest survey from the Philadelphia Federal Reserve

Bank can be found here.·

Amongst the components, the employment index was notably strong as it

rose to well above break-even and to the highest level since late-2007.

During the last ten years there has been a 91% correlation between the

index level and the three-month change in manufacturing sector

payrolls. Remaining strong were shipments, the workweek, unfilled

orders and the delivery times components. The inventory component also

improved significantly from its March low.

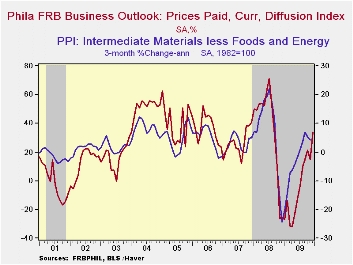

The prices paid index rose

sharply to its highest level since August of last year and compares to

negative readings this past winter and spring. During the last ten

years there has been a 71% correlation between the prices paid index

and the three-month growth in the intermediate goods PPI. There has

been an 82% correlation with the change in core intermediate goods

prices.

The prices paid index rose

sharply to its highest level since August of last year and compares to

negative readings this past winter and spring. During the last ten

years there has been a 71% correlation between the prices paid index

and the three-month growth in the intermediate goods PPI. There has

been an 82% correlation with the change in core intermediate goods

prices.

Expected business conditions in six months deteriorated for the sixth straight month. The December index fell to a still-positive reading of 24.4 but that was well-off the recent high. Many of the index components, especially orders and shipments, were down sharply.· The figures from the Philadelphia Federal Reserve can be found in Haver's SURVEYS database.

| Philadelphia Fed (%) | December | November | October | December '08 | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| General Activity Index | 20.4 | 16.7 | 11.5 | -35.1 | -7.5 | -21.3 | 5.0 |

| New Orders | 6.5 | 14.8 | 6.2 | -29.3 | -9.6 | -14.7 | 6.9 |

| Number of Employees | 6.3 | -0.5 | -6.8 | -23.8 | -23.7 | -8.7 | 6.8 |

| Prices Paid Index | 33.8 | 14.9 | 21.3 | -26.6 | -4.0 | 36.4 | 26.3 |

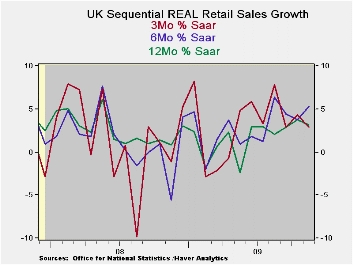

UK Retail Sales Take A Sett Back In November But Cling To Trend Rise

by Robert Brusca December 17, 2009

UK retail sales volumes fell by 0.3% in November after having

rise in October. Sales volumes have risen twice in the last

three-months and seven times in the last 12-months.

The three-month rate of growth has dipped below the six-month

rate of growth but still exceeds the 12-month growth pace. Clothing and

footwear sales, however, are clearly losing momentum having dropped in

the last three months. Retail ex-auto sales are off from their six

month pace but nearly even with their 12-month pace.

In the new quarter, Sales are growing at a pace of 3% to 3.5%.

That should help to underpin Q4 GDP growth.

In a separate report, the CBI survey of the distributive

trades produced diffusion results saying that November sales were flat

with those in October. That of course is more ambitious that the sales

count from National Statistics (above). The outlook in the CBI

framework was negative, however.

A poll of UK inflation expectations found that expectations

were stuck at 2.4% for the third consecutive quarter. While this is

above the BOE ceiling pace for inflation (of 2%) the Bank has admitted

that there would be some temporary overshoot to which it will not

respond. It is heartening that as inflation has risen in the UK,

inflation expectations have not. BOE credibility seems to be well

intact despite the damage done in the financial crisis.

| UK Real and Nominal Retail Sales | Quarter | |||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Nov-09 | Oct-09 | Sep-09 | 3-MO | 6-MO | 12-MO | YrAGo | 2-date |

| Retail Total | -0.3% | 0.5% | 0.4% | 2.9% | 4.0% | 2.6% | 2.0% | 3.2% |

| Food Bev & Tobacco | 0.2% | 0.2% | 0.1% | 2.3% | 2.2% | 3.4% | 7.3% | 2.5% |

| Clothing footwear | -2.0% | 1.5% | 0.4% | -0.7% | 1.5% | 1.4% | -1.7% | 0.3% |

| Real | ||||||||

| Retial Ex auto | -0.4% | 0.6% | 0.4% | 2.9% | 5.3% | 3.1% | 0.8% | 3.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief