Global| Mar 11 2010

Global| Mar 11 2010U.S. Flow of Funds Shows Outright Contraction of Business Credit; Other Sectors Pay Down except Government

Summary

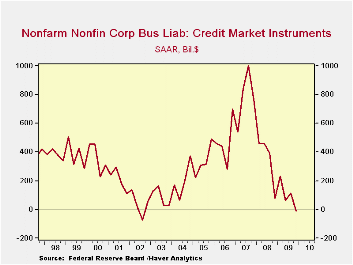

U.S. nonfinancial corporations paid down debt in Q4 2009, according to the Federal Reserve's Flow-of-Funds data reported today, March 11. The contraction was minimal, $8.2 billion at a seasonally adjusted annual rate, but it is the [...]

U.S. nonfinancial corporations paid down debt in Q4 2009, according to the Federal Reserve's Flow-of-Funds data reported today, March 11. The contraction was minimal, $8.2 billion at a seasonally adjusted annual rate, but it is the first quarterly reduction since Q3 2002 and it gives a dramatic contrast to the $999 billion borrowing surge in Q3 2007, just at the peak of the late economic expansion.

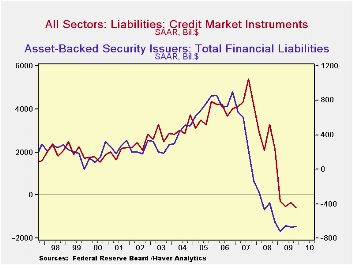

Total credit market debt contracted as well in Q4, with net

paydowns of $577 billion, SAAR, the fourth consecutive negative

quarter. The major contributing sector was financial institutions,

which pulled down their liabilities at almost a $1.3 trillion annual

rate, also a fourth consecutive reduction. The continuing shrinkage of

the market for asset-backed securities accounted for the biggest part,

as these fell at a $660 billion pace, a ninth consecutive down quarter.

Banks, saving institutions and the GSEs' themselves all shrank their

liabilities -- although GSE mortgage-backed pools were still expanding

-- and finance companies participated in the decline. Among

nonfinancial borrowers, households and noncorporate businesses reduced

their debt, households for the seventh quarter in a row and small

businesses for a fourth quarter.

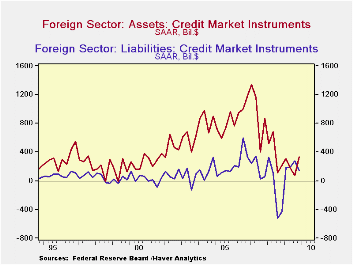

It almost goes without saying that the Federal Government was an exception to this pattern of debt reduction, although their $956 billion increase was the smallest in six quarters. Such a "pause" is likely to be short-lived. State and local governments, which have run aggregate deficits according to national income accounting since Q4 2007, have also been net borrowers. Foreign borrowers also absorbed some capital in Q4, although modestly less than in Q3 and also modest less than the inflow of funds they provided to domestic borrowers. All told, their participation in U.S. credit markets was quite even-handed in 2009, much more so than in the previous six or seven years.

| Flow of Funds (Y/Y % Chg.) | % of Total Outstanding | 4Q '09 | 3Q '09 | 2Q '09 | End of Year | ||

|---|---|---|---|---|---|---|---|

| 2008 | 2007 | 2006 | |||||

| Total Credit Market Debt Outstanding | 100.0% | -0.2 | 0.9 | 2.8 | 5.0 | 10.4 | 9.8 |

| Federal Government | 14.9% | 22.7 | 30.1 | 35.9 | 24.2 | 4.9 | 3.9 |

| Households | 25.8% | -1.7 | -1.8 | -1.3 | 0.2 | 6.7 | 10.0 |

| Nonfinancial Corporate Business | 13.8% | 1.5 | 1.8 | 2.8 | 5.1 | 13.2 | 8.5 |

| Nonfarm, Noncorporate Business | 6.8% | -7.9 | -5.4 | -1.9 | 5.5 | 14.2 | 14.7 |

| Financial Sectors | 29.9% | -8.4 | -5.6 | -1.3 | 5.4 | 13.5 | 9.9 |

| Trillions of $ | |||||||

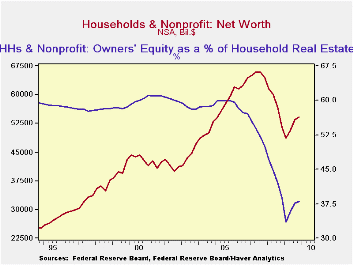

| Net Worth: Households & Nonprofit Organizations | -- | $54.176 | $53.494 | $50.711 | $51,403 | $64.484 | $64.464 |

| Tangible Assets: Households | -- | $23.063 | $23.082 | $22.790 | $23.891 | $28.036 | $29.735 |

| Financial Assets: Households | -- | $45.115 | $44.438 | $41.963 | $41.707 | $50.7698 | $48.134 |

| Total Liabilities: Households | -- | $14.001 | $14.027 | $14.042 | $14.195 | $14.312 | $13.405 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief