Global| Sep 26 2005

Global| Sep 26 2005U.S. Existing Home Sales Still Near Record in August

by:Tom Moeller

|in:Economy in Brief

Summary

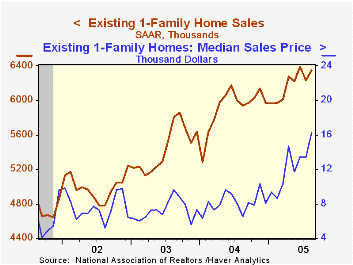

The National Association of Realtors reported that with a 2.0% m/m rise in August to 7.29 million, total existing home sales recovered nearly all of the prior month's downwardly revised 2.7% decline. Consensus expectations had been [...]

The latest release from the National Association of Realtors is available here.

| Existing Home Sales (000, AR) | Aug | July | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total Home Sales | 7,290 | 7,150 | 7.8% | 6,723 | 6,170 | 5,653 |

| Single Family Home Sales | 6,350 | 6,230 | 6.9% | 5,913 | 5,441 | 4,995 |

| Single Family Median Home Price ($,000) | $219.4 | $215.7 | 16.2% | $182.8 | $169.1 | $157.6 |

by Louise Curley September 26, 2005

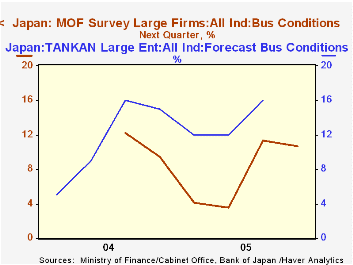

Large Corporations (corporations with capital of 1 billion or more) in Japan have become more optimistic according to the Business Outlook Survey conducted by the Ministry of Finance (MOF) and the Cabinet Office's Economic and Social Research Institute. The percentage of all large corporations reporting better rather than worse current conditions in the third quarter rose to 9.7% from 0.9% in the second quarter. This was below the estimate of 11.3% for the third quarter made in the second quarter. However, the current estimate for the next quarter--the fourth of 2005--is 10.7%, which suggests that the optimists continue to outweigh the pessimists. As for large manufacturing corporation, while the mood has become more optimistic, the excess of better over worse conditions for the current quarter is only 6.4%. In looking ahead, however, large manufacturers have been estimating steady improvement

The latest survey shows that optimists outweighed pessimists in medium sized corporations (corporations with capital of 100 million to 1 billion yen) in the current quarter. and are expected to continue to do so. Small sized corporations (corporations with capital between 10 and 100 million yen) continue to be pessimistic, but their degree of pessimism had begun to diminish.The excess of pessimists fell from 21.4% to 15.1% in the current survey.

Some analysts have come to look upon the MOF's Business Outlook Survey as an indicator of the business conditions indicator for large enterprises in the more widely known Tankan Survey that tends to be released about a week or so after the MOF survey. (The next Tankan results are due on October 3, 2005.) The attached chart showing the next quarter estimate of the Business Outlook Survey and the forecast of business conditions for large enterprises in the Tankan Survey seems to bear out this hypothesis, but it should be kept in mind that as it is based on only a small number of data points it significance is yet to be tested.

| Ministry of Finance Business Outlook Survey | Current | Quarter | Estimate | Next | Quarter | Estimate | |

|---|---|---|---|---|---|---|---|

| of Change | Q3 05 | Q2 05 | Q1 05 | Q4 05 | Q3 05 | Q2 05 | |

| All Industry | |||||||

| Large Corporations | 9.7 | 0.9 | 0.6 | 10.7 | 11.3 | 3.6 | |

| Medium Corporations | 5.5 | -5.0 | -9.7 | 7.5 | 7.5 | 3.4 | |

| Small Corporations | -15.1 | -21.4 | -24.3 | -3.8 | -12.6 | -11.1 | |

| Manufacturing | |||||||

| Large Corporations | 6.4 | -2.4 | -7.6 | 11.1 | 10.9 | 1.9 | |

| Medium Corporations | -5.1 | -6.9 | -18.7 | 8.1 | 8.2 | 7.8 | |

| Small Corporations | -11.9 | -19.9 | -24.6 | -1.7 | -10.5 | -9.1 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief