Global| Feb 25 2010

Global| Feb 25 2010U.S. Durable Goods Orders Surge Due To Aircraft

by:Tom Moeller

|in:Economy in Brief

Summary

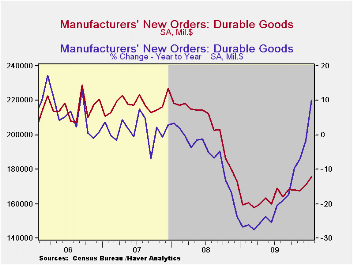

Improvement in the factory sector looked material last month. The overall level of durable goods orders jumped 3.0%, that followed an upwardly revised 1.9% December increase and it far outpaced Consensus expectations for a 1.5% gain. [...]

Improvement

in the factory sector looked material last month. The overall level of

durable goods orders jumped 3.0%, that followed an upwardly revised

1.9% December increase and it far outpaced Consensus expectations for a

1.5% gain. Unfortunately, the strength was limited. Orders for

nondefense aircraft & parts more than doubled and mostly

recouped sharp declines during the prior two months.

Improvement

in the factory sector looked material last month. The overall level of

durable goods orders jumped 3.0%, that followed an upwardly revised

1.9% December increase and it far outpaced Consensus expectations for a

1.5% gain. Unfortunately, the strength was limited. Orders for

nondefense aircraft & parts more than doubled and mostly

recouped sharp declines during the prior two months.

Regardless of the January overstatement from the aircraft sector, the durable factory goods sector appeared on the mend after last year's recession. Less the transportation sector, orders slipped 0.6% though that followed two strong 2.0% monthly increases. That was enough to lift the y/y gain in orders to 8.6%. This strength suggests further improvement in shipments and industrial output are on the come after the modest y/y gains already logged.· Transportation sector orders last month were lifted by the jump in nondefense aircraft as well as by an 11.6% (66.4% y/y) rise in defense sector bookings. Orders for motor vehicles slipped m/m but were up modestly from last year. That increase followed annual declines during each of the last four years which left orders nearly half of their 2006 level

Improvement in other sectors continued last month. Primary metals orders increased 1.9% (31.6% y/y) following even stronger gains during each of the prior four months. Electrical equipment orders also rose 1.4% (3.8% y/y) while orders for computers & related equipment jumped 4.6% (16.0% y/y). Only machinery orders lagged with a 9.7% decline (+8.9% y/y) but that followed sharp increases during three of the prior four months.

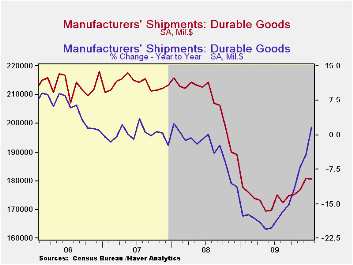

Shipments of durable goods slipped 0.2% (+1.7% y/y) during January following increases during the prior four months. The increase was led by an 8.5% jump (14.0% y/y) in shipments of computers & electronic products but that was offset by declines in shipments of nondefense capital goods (-3.2% y/y), machinery (-7.9% y/y) and electrical equipment (-2.2% y/y). Nevertheless, these negative y/y changes were much-reduced from those during the recession.

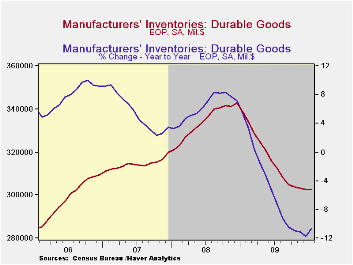

Perhaps the factory sector's inventory retrenchment is winding down, but it's not over. Durable goods inventories slipped just modestly during January (-10.6% y/y) as they did during the prior two months. However, these followed very sharp declines through September. Overall, since the December 2008 peak, inventories have fallen 11.7%.

The durable goods figures are

available in Haver's USECON database.

| NAICS Classification (%) | January | December | November | Y/Y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Durable Goods Orders | 3.0 | 1.9 | -0.4 | 10.2 | -19.8 | -6.0 | 1.4 |

| Excluding Transportation | -0.6 | 2.0 | 2.0 | 8.6 | -17.3 | -1.4 | -0.3 |

| Nondefense Capital Goods | 4.7 | 2.5 | -3.0 | 15.9 | -23.9 | -7.0 | 3.6 |

| Excluding Aircraft | -2.9 | 3.3 | 3.2 | 10.7 | -18.2 | -0.5 | -2.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief