Global| Dec 23 2009

Global| Dec 23 2009U.S. Disposable Personal Income& Spending Continue Firm

by:Tom Moeller

|in:Economy in Brief

Summary

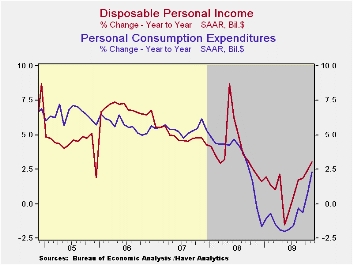

Tax breaks continued to spur growth in disposable personal income. Last month's 0.5% gain followed an upwardly revised 0.5% October increase. A decline in tax payments (-25.7% y/y), which began early in 2008, helped spur y/y [...]

Tax breaks

continued to spur growth in disposable personal income.

Last month's 0.5% gain followed an upwardly revised 0.5% October

increase. A decline in tax payments (-25.7% y/y), which began early in

2008, helped spur y/y disposable income growth to 3.1%. Adjusted for a

0.2% (1.5% y/y) rise in the chain price index, real disposable income

rose 0.2% (1.5% y/y) for the third consecutive month.

Tax breaks

continued to spur growth in disposable personal income.

Last month's 0.5% gain followed an upwardly revised 0.5% October

increase. A decline in tax payments (-25.7% y/y), which began early in

2008, helped spur y/y disposable income growth to 3.1%. Adjusted for a

0.2% (1.5% y/y) rise in the chain price index, real disposable income

rose 0.2% (1.5% y/y) for the third consecutive month.

Personal

spending rose 0.5% after a 0.6% October increase which was

double the initial estimate. The rise fell short of the 0.7% increase

which was the Consensus expectation. Durables spending jumped 1.1%

(2.5% y/y) as spending on motor vehicles gained another 2.2% (7.9% y/y)

following a 9.5% October surge. Spending on other durables, however,

remained lackluster. Furniture & appliance purchases fell

slightly for the second month and were off 2.9% y/y. Spending on

nondurables increased 1.5% (4.6% y/y) as outlays on gasoline jumped

7.2% (18.6% y/y) with higher prices. In constant dollars gasoline

outlays rose just 0.9% and were down slightly y/y. Spending on clothing

slipped 0.3% (-1.1% y/y) though that y/y change is improved from 6.8%

decline at the worst of the recent recession. Outlays on services were

unchanged (1.5% y/y). Spending on health care rose 0.4% (4.8% y/y) but

housing & utilities spending fell 0.4% (+0.2% y/y).

Personal

spending rose 0.5% after a 0.6% October increase which was

double the initial estimate. The rise fell short of the 0.7% increase

which was the Consensus expectation. Durables spending jumped 1.1%

(2.5% y/y) as spending on motor vehicles gained another 2.2% (7.9% y/y)

following a 9.5% October surge. Spending on other durables, however,

remained lackluster. Furniture & appliance purchases fell

slightly for the second month and were off 2.9% y/y. Spending on

nondurables increased 1.5% (4.6% y/y) as outlays on gasoline jumped

7.2% (18.6% y/y) with higher prices. In constant dollars gasoline

outlays rose just 0.9% and were down slightly y/y. Spending on clothing

slipped 0.3% (-1.1% y/y) though that y/y change is improved from 6.8%

decline at the worst of the recent recession. Outlays on services were

unchanged (1.5% y/y). Spending on health care rose 0.4% (4.8% y/y) but

housing & utilities spending fell 0.4% (+0.2% y/y).

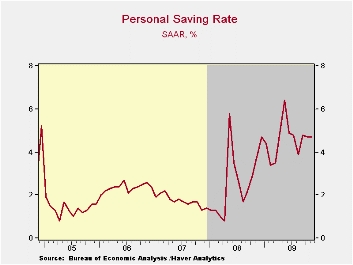

As a result of tax cuts and moderate spending, the savings rate held steady at the upwardly revised 4.7% October level. The rate has risen sharply from near 1.0% at the beginning of last year.

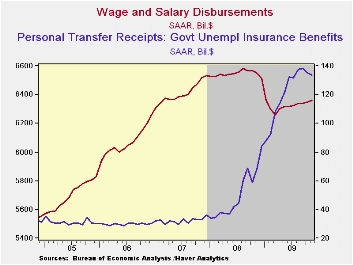

Overall personal

income gained 0.4% during November after an upwardly revised

0.3% October increase. The latest figure fell short of Consensus

expectations for a 0.5% rise. Wages & salaries rose 0.3% due to

the pickup in average hourly earnings reported with the jobs numbers.

Nevertheless, year-to-year growth in wages continued negative (-2.8%

y/y), only slightly improved from the worst y/y growth of this cycle.

Wages in the factory sector rose 0.2% (-10.4% y/y) after a 0.4% October

decline. In the service sector wages rose a firmer 0.4% (-1.7% y/y).

Though wages in the government sector only ticked up 0.1% last month,

the 2.9% y/y gain easily outpaced the 4.1% decline in private sector

earnings.

Overall personal

income gained 0.4% during November after an upwardly revised

0.3% October increase. The latest figure fell short of Consensus

expectations for a 0.5% rise. Wages & salaries rose 0.3% due to

the pickup in average hourly earnings reported with the jobs numbers.

Nevertheless, year-to-year growth in wages continued negative (-2.8%

y/y), only slightly improved from the worst y/y growth of this cycle.

Wages in the factory sector rose 0.2% (-10.4% y/y) after a 0.4% October

decline. In the service sector wages rose a firmer 0.4% (-1.7% y/y).

Though wages in the government sector only ticked up 0.1% last month,

the 2.9% y/y gain easily outpaced the 4.1% decline in private sector

earnings.

Growth in

unemployment insurance payments slowed

further as joblessness fell. In fact, moderate declines during the last

two months compare with the y/y doubling earlier this year. Interest

income rose 0.2% (-4.6% y/y) as the decline in rates found a bottom

while another 0.9% m/m increase in dividend income

nevertheless left it down 18.0% y/y with the weaker economy.

Growth in

unemployment insurance payments slowed

further as joblessness fell. In fact, moderate declines during the last

two months compare with the y/y doubling earlier this year. Interest

income rose 0.2% (-4.6% y/y) as the decline in rates found a bottom

while another 0.9% m/m increase in dividend income

nevertheless left it down 18.0% y/y with the weaker economy.

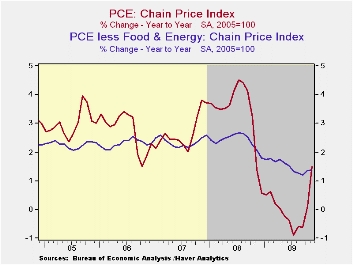

The PCE chain price index increased a moderate 0.2% during November led by a 6.2% (18,5% y/y) increase in gasoline costs. Less food-and-energy, "core" prices were unchanged. Prices for durable goods were off 0.1% (-1.1% y/y) as home furnishing prices fell 0.5% (-2.1% y/y) and apparel prices also fell 0.5% (+0.8% y/y). Prices for services gained a steady 1.2% y/y.

The personal income & consumption figures are available in Haver's USECON and USNA databases.

| Disposition of Personal Income (%) | November | October | September | Y/Y | 2008 | 2007 |

|---|---|---|---|---|---|---|

| Personal Income | 0.4 | 0.3 | 0.3 | -0.3 | 2.9 | 5.6 |

| Disposable Personal Income | 0.5 | 0.5 | 0.3 | 3.1 | 3.9 | 4.9 |

| Personal Consumption Expenditures | 0.5 | 0.6 | -0.6 | 2.3 | 3.1 | 5.4 |

| Saving Rate | 4.7 | 4.7 | 4.8 | 3.8 (Nov.'08) | 2.6 | 1.7 |

| PCE Chain Price Index | 0.2 | 0.3 | 0.1 | 1.5 | 3.3 | 2.7 |

| Less food & energy | 0.0 | 0.2 | 0.1 | 1.4 | 2.4 | 2.4 |

Michigan Consumer Sentiment Increases Smartly

by Tom Moeller December 23, 2009

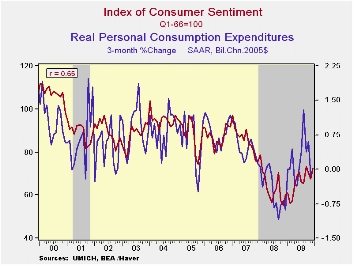

Though the

December Reuters/University of Michigan Index of Consumer Sentiment

slipped from mid-month, is 7.6% increase to 72.5 recovered most of the

declines during the prior two months. The latest figure fell short of

Consensus expectations for a level of 73.8. Nevertheless, sentiment was

up sharply from its low last Fall. During the last ten years there has

been a two-thirds correlation between the level of sentiment and the

three-month change real consumer spending.

Though the

December Reuters/University of Michigan Index of Consumer Sentiment

slipped from mid-month, is 7.6% increase to 72.5 recovered most of the

declines during the prior two months. The latest figure fell short of

Consensus expectations for a level of 73.8. Nevertheless, sentiment was

up sharply from its low last Fall. During the last ten years there has

been a two-thirds correlation between the level of sentiment and the

three-month change real consumer spending.

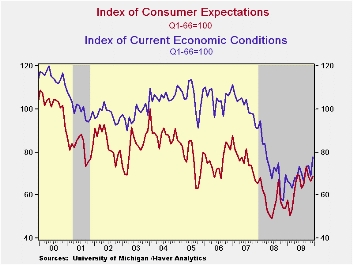

Sentiment about current economic conditions jumped 13.4% from November to the highest level since March of last year. Assessments of current financial conditions improved to the highest since September of last year. Buying conditions for large household goods, including furniture, refrigerators, stoves & televisions, also moved up by 12.3% to the highest level since January 2008.

The

full-month December reading on expected economic conditions recovered

its November decline with a 3.6% increase to the highest level since

September. The outlook for business conditions during the next twelve

months improved sharply and recovered most of November's decline but

the expected business conditions during the next five years fell and

expected personal finances advanced just modestly. All three of these

readings recently have been flat after sharp improvement early this

year.

The

full-month December reading on expected economic conditions recovered

its November decline with a 3.6% increase to the highest level since

September. The outlook for business conditions during the next twelve

months improved sharply and recovered most of November's decline but

the expected business conditions during the next five years fell and

expected personal finances advanced just modestly. All three of these

readings recently have been flat after sharp improvement early this

year.

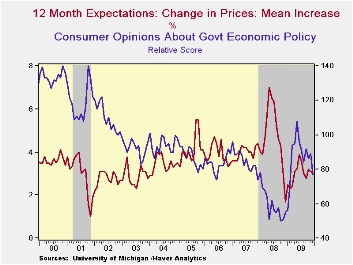

Expected

price inflation during the next year was roughly steady

m/m at 3.0% but it was up from last December's reading of

1.7%. Respondents' view of government policy, which may

eventually influence economic expectations, fell sharply m/m to the

lowest level since February. Sixteen percent of respondent thought that

a good job was being done by government versus 39% who thought a poor

job was being done.

Expected

price inflation during the next year was roughly steady

m/m at 3.0% but it was up from last December's reading of

1.7%. Respondents' view of government policy, which may

eventually influence economic expectations, fell sharply m/m to the

lowest level since February. Sixteen percent of respondent thought that

a good job was being done by government versus 39% who thought a poor

job was being done.

The Reuters/University of Michigan survey data are not seasonally adjusted. The reading is based on telephone interviews with about 500 households at month-end. These mid-month results are based on about 320 interviews. The summary indexes are in Haver's USECON database with details in the proprietary UMSCA database.

Inflation Expectations and the Risk of Deflation from the Federal Reserve Bank of San Francisco is available here.

| University of Michigan | December | Mid-December | November | October | Dec y/y | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 72.5 | 73.4 | 67.4 | 70.6 | 20.6% | 66.3 | 63.8 | 85.6 |

| Current Conditions | 78.0 | 79.1 | 68.8 | 73.7 | 12.2 | 69.6 | 73.7 | 101.2 |

| Expectations | 68.9 | 69.7 | 66.5 | 68.6 | 27.6 | 64.1 | 57.3 | 75.6 |

U.S. New Home Sales Fall Sharply

by Tom Moeller Deecember 23, 2009

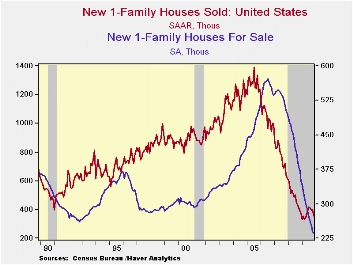

Conflicting

signals have been flashed regarding homes sales last month. In contrast

to yesterday's report that existing home sales rose, today the Commerce

Department reported that new home sales fell by 11.3% m/m to 355,000,

the lowest level since April. Nevertheless, near term home sales should

be helped by the recent extension of the Federal government's tax

credit which now it is for all home buyers and not just first-time

purchases. The November sales figure fell well short of Consensus

expectations for 439,000 sales.

Conflicting

signals have been flashed regarding homes sales last month. In contrast

to yesterday's report that existing home sales rose, today the Commerce

Department reported that new home sales fell by 11.3% m/m to 355,000,

the lowest level since April. Nevertheless, near term home sales should

be helped by the recent extension of the Federal government's tax

credit which now it is for all home buyers and not just first-time

purchases. The November sales figure fell well short of Consensus

expectations for 439,000 sales.

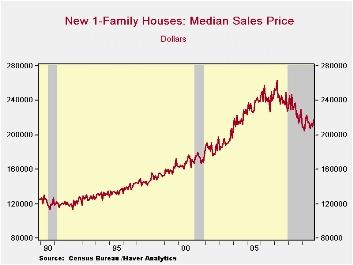

Home

prices firmed

during November though the October figure was revised down. The median

price of a new single-family home rose to $217,400 which was the

highest level since May. The increase pared the y/y decline to 1.9%

from its worst of -14.5% this past February. The average new home price

of $280,300 was off 3.4% y/y.

Home

prices firmed

during November though the October figure was revised down. The median

price of a new single-family home rose to $217,400 which was the

highest level since May. The increase pared the y/y decline to 1.9%

from its worst of -14.5% this past February. The average new home price

of $280,300 was off 3.4% y/y.

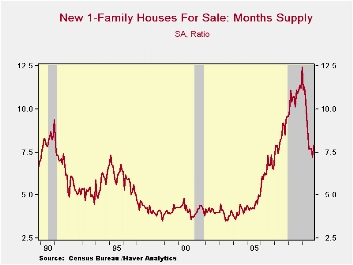

Price

discounts, higher sales

and much lower housing starts have combined to lower the overhang of

unsold homes by more than one-third y/y to the overhang lowest level

since the early-1970s. The months' supply of unsold homes rose

moderately to 7.9 months but remained down from the high of 12.4 months

in January. The figure was the lowest since May 2007.

Price

discounts, higher sales

and much lower housing starts have combined to lower the overhang of

unsold homes by more than one-third y/y to the overhang lowest level

since the early-1970s. The months' supply of unsold homes rose

moderately to 7.9 months but remained down from the high of 12.4 months

in January. The figure was the lowest since May 2007.

Recent Developments in Mortgage Finance from the Federal Reserve Bank of San Francisco can be found here.

| US New Homes | November | October | September | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total Sales (SAAR, 000s) | 355 | 400 | 393 | -9.0% | 481 | 769 | 1,049 |

| Northeast | 29 | 30 | 36 | -23.7 | 35 | 64 | 64 |

| Midwest | 68 | 56 | 68 | 23.6 | 69 | 118 | 161 |

| South | 179 | 227 | 196 | -14.8 | 264 | 409 | 559 |

| West | 79 | 87 | 93 | -9.2 | 113 | 178 | 266 |

| Median Price (NSA, $) | 217,400 | 209,400 | 213,500 | -1.9 | 230,408 | 243,742 | 243,067 |

Italy's Consumer Confidence Lifts Spirits For Christmas

Oh Come Ye Faithful...

by Tom Moeller December 23, 2009

Confidence rose again in December for Italian consumers making

the string of rises two months long. Still, the overall situation

deteriorated by one point to a -57 reading in December leaving the

current situation in the 68th percentile of its range.

The outlook for the overall situation also backtracked

dropping by 5 points month to month. Unemployment expectations rose and

now reside on the top 5% of their range.

The outlook for current savings backtracked but the outlook

for future savings rose sharply in the month.

The current environment for major purchase was sharply better

with its index rising to -38 from -43 and moving up to the 59th

percentile of its range.

Clearly the Italian consumer still feels pressured. The rise

in confidence is a good development despite backtracking in some key

components.

Italy still has a long way to go to cement any notion of

stability.

| Since Jan 1992 Rank | |||||||

| Dec-09 | Nov-09 | Oct-09 | Sep-09 | Percentile | Rank | percentile | |

| Consumer Confidence | 113.7 | 112.8 | 111.7 | 113.6 | 60.1 | 76 | 64.3% |

| Last 12 months | |||||||

| OVERALL SITUATION | -57 | -56 | -58 | -58 | 72.0 | 68 | 68.1% |

| PRICE TRENDS | -41 | -39 | -40.5 | -42 | 13.6 | 207 | 2.8% |

| Next 12months | |||||||

| OVERALL SITUATION | -1 | 4 | -2 | 5 | 60.3 | 109 | 48.8% |

| PRICE TRENDS | 8.5 | 8 | 7 | 9.5 | 17.3 | 96 | 54.9% |

| UNEMPLOYMENT | 16 | 15 | 19 | 17 | 67.6 | 10 | 95.3% |

| HOUSEHOLD BUDGET | 1 | 3 | 5 | 6 | 17.8 | 199 | 6.6% |

| HOUSEHOLD FIN SITUATION | |||||||

| Last 12 months | -37 | -36 | -35 | -33 | 38.8 | 129 | 39.4% |

| Next12 months | -3 | -2 | -4 | -1 | 65.3 | 102 | 52.1% |

| HOUSEHOLD SAVINGS | |||||||

| Current | 73 | 77 | 79 | 80 | 88.3 | 6 | 97.2% |

| Future | -20 | -29 | -30 | -16 | 62.2 | 124 | 41.8% |

| MAJOR Purchases | |||||||

| Current | -38 | -43 | -38 | -40 | 47.3 | 87 | 59.2% |

| Total number of months: 213 | |||||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief