Global| Feb 20 2009

Global| Feb 20 2009U.S. CPI Ticked Up

by:Tom Moeller

|in:Economy in Brief

Summary

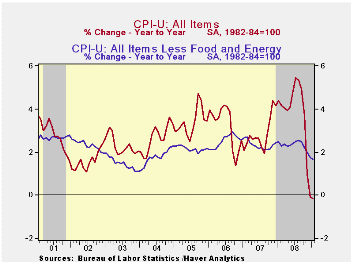

During February the consumer price index (CPI-U) rose for the first month since July, according to the U.S. Bureau of Labor Statistics. The 0.3% gain followed drops of 0.8% and 1.7% during December and November. Due to those earlier [...]

During

February the consumer price index (CPI-U) rose for

the first month since July, according to the U.S. Bureau of Labor

Statistics. The 0.3% gain followed drops of 0.8% and 1.7% during

December and November. Due to those earlier sharp declines the

three-month rate of change remained quite weak at -8.4% (AR). The

latest increase matched Consensus expectations.

During

February the consumer price index (CPI-U) rose for

the first month since July, according to the U.S. Bureau of Labor

Statistics. The 0.3% gain followed drops of 0.8% and 1.7% during

December and November. Due to those earlier sharp declines the

three-month rate of change remained quite weak at -8.4% (AR). The

latest increase matched Consensus expectations.

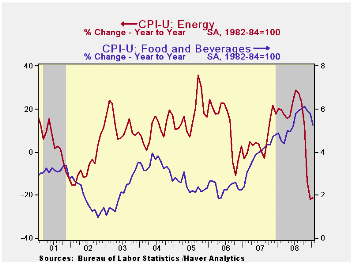

A 1.7% rise in energy prices led last month's increase in the CPI after having been down during the previous five months. Gasoline prices reversed earlier declines with a 6.0% (-40.4% y/y) increase to an average of $1.79 per gallon of regular. Still moving lower last month, however, were fuel oil prices which fell 2.7% (-19.5% y/y). It was their sixth consecutive monthly drop while prices for natural gas & electricity fell 0.8% m/m (+7.2% y/y).

Increases in food & beverage prices have very much tapered off from their strong gains earlier this year. A 0.1% uptick followed a like gain during December. That pulled the three month annual rate of increase down to 1.4% after growth as high as 8.7% this summer. Outright declines in meat and dairy product prices as well as much easier growth in cereal & bakery product costs account for the moderation.

Core prices (CPI

less food and energy)

showed their strongest increase since August with a 0.2%

rise. However, despite the increase the year-to-year gain of

1.7% remained its weakest since mid-2004. Little or no growth in core

prices during the prior four months accounts for the moderation.

Core prices (CPI

less food and energy)

showed their strongest increase since August with a 0.2%

rise. However, despite the increase the year-to-year gain of

1.7% remained its weakest since mid-2004. Little or no growth in core

prices during the prior four months accounts for the moderation.

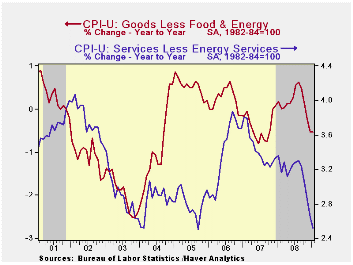

Core goods prices rose for the first time since July. The 0.3% increase reversed the prior month's decline but nevertheless left the three-month rate of change at a negative 0.9%. Prices of new & used motor vehicles increased for the first time in a year, but the 0.2% rise left them down 3.2% during that period. Lower prices of used cars paced the decline with a 9.2% twelve month decrease. Apparel prices ticked up 0.3% (-0.9% y/y) while prices for household furnishings & operations ticked lower by 0.1% (+1.8% y/y). Appliance prices were up 2.0% y/y while furniture prices were unchanged y/y. Tobacco prices again were strong during January and they posted a 0.8% increase (+6.1% y/y).

Gains in core services prices continued

moderate

with a 0.2% increase That left the three-month rate of increase at 1.6%

(AR) after growing at a 3.9% rate this past summer. Medical

care services prices rose 0.5% (3.0% y/y) which was their strongest

increase in twelve months. Education costs posted a 0.3%

increase and the year-to-year rise of 5.5% was stable with the growth

in recent years, though down from the 6.9% increase during

2004. Shelter prices rose 0.2% and the y/y increase fell to

1.8%. As the housing market remained deeply depressed, owners

equivalent rent of primary residence, a measure not equivalent to other

house price measures, rose 0.3% (2.2% y/y). Public

transportation prices fell hard for the fifth consecutive month and

were unchanged year-to-year. Recreation prices also were

unchanged last month and they have been flat or down during the last

there periods, +1.6% y/y.

Shelter prices rose 0.2% and the y/y increase fell to

1.8%. As the housing market remained deeply depressed, owners

equivalent rent of primary residence, a measure not equivalent to other

house price measures, rose 0.3% (2.2% y/y). Public

transportation prices fell hard for the fifth consecutive month and

were unchanged year-to-year. Recreation prices also were

unchanged last month and they have been flat or down during the last

there periods, +1.6% y/y.

The chained CPI, which adjusts for shifts in consumption patterns, rose 0.5%, the first increase since July. Less food and energy, chained prices rose 0.2% after two months of 0.3% decline.

The consumer price data is available in Haver's USECON database while detailed figures can be found in the CPIDATA database.

House Prices and Bank Loan Performance from the Federal Reserve Bank of San Francisco can be found here.

Labor Supply Responses to Changes in Wealth and Credit also from the Federal Reserve Bank of San Francisco is available here.

| Consumer Price Index (%) | January | December | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total | 0.3 | -0.8 | -0.2 | 3.8 | 2.9 | 3.2 |

| Total less Food & Energy | 0.2 | 0.0 | 1.7 | 2.3 | 2.3 | 2.5 |

| Goods less Food & Energy | 0.1 | -0.2 | -0.5 | 0.1 | -0.4 | 0.2 |

| Services less Energy | 0.2 | 0.1 | 2.5 | 3.1 | 3.4 | 3.4 |

| Energy | 1.7 | -9.3 | -21.1 | 13.5 | 5.7 | 11.0 |

| Food & Beverages | 0.1 | 0.1 | 5.2 | 5.4 | 3.9 | 2.3 |

| Chained CPI: Total (NSA) | 0.5 | -1.3 | -0.5 | 3.3 | 2.5 | 2.9 |

| Total less Food & Energy | 0.2 | -0.3 | 1.2 | 2.0 | 2.0 | 2.2 |

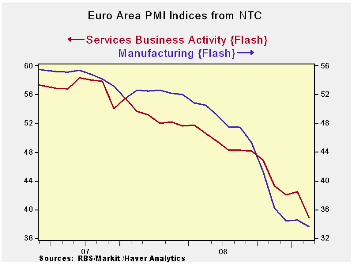

Euro Area PMIs Continue To Drop... Very Sharply

by Robert Brusca February 20, 2009

The European PMI readings are very weak again in February. In

January there was a slight bounce in the indices for MFG as well as for

Services but in February the weakness is back in force with the indices

dropping very sharply - especially for Services. There the

month-to-month drop form this already low level is the largest decline

m/m on record.

Weakness in the Euro Area is still gathering pace, which is

terrible news.

Germany, today saw its 50 billion euro stimulus plan go over

its last hurdle. Italian industrial orders fell in December but by less

than expected. December UK retail sales rose unexpectedly. But in

France its survey by Insee produced its lowest reading in the history

of the survey that extends back to the mid-1970s. Europe is continuing

to be buffeted with weakness and the more topical the measure the

weaker the results seem to be.

| FLASH Readings | ||

|---|---|---|

| Market PMIs for the Euro Area | ||

| MFG | Services | |

| Feb-09 | 33.63 | 38.92 |

| Jan-09 | 34.42 | 42.16 |

| Dec-08 | 33.88 | 42.06 |

| Nov-08 | 35.58 | 42.47 |

| Averages | ||

| 3-Mo | 34.63 | 41.15 |

| 6-Mo | 39.58 | 43.64 |

| 12-Mo | 44.98 | 46.82 |

| 127-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.63 | 38.92 |

| % Range | 0.0% | 0.0% |

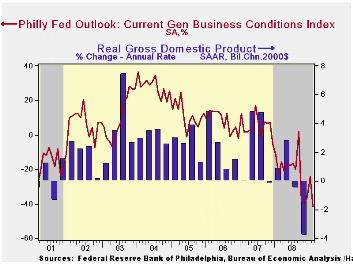

Philadelphia Fed Index Lowest Since 1990

by Tom Moeller February 20, 2009

The latest figures from the Philadelphia Federal Reserve Bank show that the February Business Activity Index fell further to its lowest level since 1990 and that rivaled the lows of the series' forty year history. The bank reported that its February Index of General Business conditions in the manufacturing sector fell to -41.3 from 24.3 last month. A reading of -25 had been expected.

During the last ten years there has been a 70% correlation between the level of the Philadelphia Fed Business Conditions Index and the three-month growth in factory sector industrial production. There has been a 64% correlation with q/q growth in real GDP.

The Philadelphia Fed constructs a diffusion index for total business activity and each of the sub-indexes. The business conditions index reflects a separate survey question.

Amongst the sub-indexes, the new orders figure led this

month's weakness with a decline to near the lowest since 1980. The

shipments index fell to a record low.

The employment index fell another 6.8 points this month, and was down 17.2 points during the last two months, to a record low. Forty eight percent of respondents expected to reduce employment levels, a record, while only two percent expected to raise them. During the last ten years there has been a 79% correlation between the index level and the m/m change in manufacturing sector payrolls.

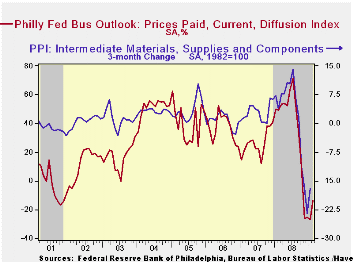

The prices paid index nudged up month-to-month to -13.7 but just thirteen percent of respondents planned to raise prices. Thirty two percent expected to lower prices. During the last ten years there has been a 72% correlation between the prices paid index and the three-month growth in the intermediate goods PPI. There has been an 80% correlation with the change in core intermediate goods prices.

The separate index of expected business conditions in six months improved to its highest level since September. The expectations index for new orders led the gain but the expectations index for employment rose just marginally from the record low reached in January.

The figures from the Philadelphia Federal Reserve can be found in Haver's SURVEYS database.

The latest Business Outlook Survey from the Federal Reserve Bank of Philadelphia can be found here.

| Philadelphia Fed (%) | February | January | February '08 | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| General Activity Index | -41.3 | -24.3 | -22.6 | -21.3 | 5.0 | 8.0 |

| Prices Paid Index | -13.7 | -27.0 | 49.5 | 36.4 | 26.3 | 36.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief