Global| Nov 16 2009

Global| Nov 16 2009U.S. Business Inventory Decumulation Slows

by:Tom Moeller

|in:Economy in Brief

Summary

Perhaps the recent, moderate turnaround in final demand evident in the economy has begun to affect business' inclination to shed inventory. Or maybe there's nothing left on the lot, in the warehouse or on the shelf to let go. Either [...]

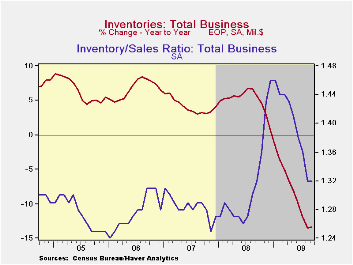

Perhaps the recent, moderate turnaround in final demand evident in the economy has begun to affect business' inclination to shed inventory. Or maybe there's nothing left on the lot, in the warehouse or on the shelf to let go. Either way, business inventories slipped just 0.4% during September which was one-third of the monthly decumulation averaged back to October of last year. The decline also fell short of Consensus expectations for a 0.7% drop.

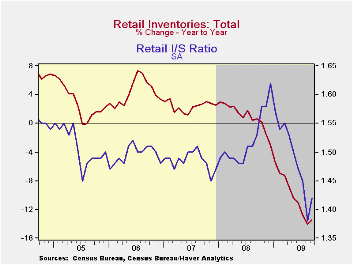

The overall slowdown was caused by a 0.6% increase in retail inventories, the first gain since last July. That increase resulted from a 3.8% (-27.9% y/y) rise in auto inventories which also was the first since July of last year. In contrast, the monthly rate of decline in nonauto inventories continued at 0.6% (-7.5% y/y). Furniture inventories increased 0.1% (-12.5% y/y) but clothing inventories fell a sharp 1.7% (-10.8% y/y). General merchandise inventories fell 0.4% and were off 6.3% y/y while building materials stores slipped just 0.1% (-9.6% y/y). Factory inventories fell a hard 1.0%. Meanwhile, wholesale inventories were off 0.9% and the y/y decline reached a nadir of 15.0%. Excluding oil, wholesale inventories fell 0.9% and the 15.4% rate of decline also was a new low.

Despite a possible interest in slowing the rate of inventory cutbacks, the inventory-to-sales ratio for total business held at the cycle low of 1.32 versus a high of 1.46 in January. The latest was the lowest since last September. In the retail sector the ratio moved higher as a result of the auto inventory rise, but at 1.42 it still was the second lowest of the cycle. For manufacturers and wholesalers, the ratio fell to new cycle lows.

The business sales and inventory data are available in Haver's USECON database.

The Behavior of Household and Business Investment over the Business Cycle from the Federal Reserve Bank of Richmond can be found here.

| Business Inventories (%) | September | August | July | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total | -0.4 | -1.6 | -1.1 | -13.4 | 0.6 | 4.0 | 6.4 |

| Retail | 0.6 | -2.6 | -1.0 | -13.9 | -3.1 | 2.5 | 3.3 |

| Retail excl. Auto | -0.6 | -0.7 | -0.5 | -7.5 | -1.8 | 2.7 | 4.7 |

| Wholesale | -0.9 | -1.3 | -1.6 | -15.0 | 3.1 | 6.2 | 8.2 |

| Manufacturing | -1.0 | -0.9 | -0.9 | -11.8 | 2.1 | 3.7 | 8.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief