Global| Mar 19 2008

Global| Mar 19 2008U.S. Business Inventories Starting to Back Up

by:Tom Moeller

|in:Economy in Brief

Summary

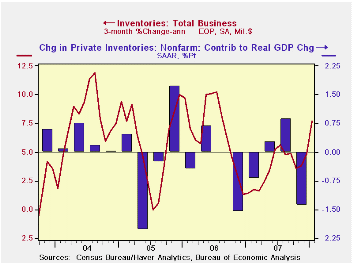

The Commerce Department reported that for January total business inventories rose 0.8% after an upwardly revised 0.7% rise in December. The annualized three month growth in inventories rose as a result to 7.7%, its strongest since [...]

The Commerce Department reported that for January total business inventories rose 0.8% after an upwardly revised 0.7% rise in December. The annualized three month growth in inventories rose as a result to 7.7%, its strongest since mid-2006. The quicker rate of accumulation, if sustained, would reverse much of the -1.4 percentage point contribution inventories made to 4Q07 growth in real GDP.

A quicker rate of accumulation of factory inventories accounts for much of the acceleration. In January they surged by 1.3% after a strong 0.9% December increase. Together they raised the three month rate of accumulation to 12.0%, up from 7.2% during 4Q07. Higher oil prices were behind some of that faster rate of gain as petroleum inventories rose 8.1% in January (29.7% y/y). Nevertheless, excluding petroleum factory inventories still increased a firm 0.8% during January, the same as in the prior month, and the three month rate of accumulation rose to 8.8%, up from the 5.9% 4Q rate of gain and from the 1.7% 3Q rise.

Retail inventories are up, but the rate of gain shows a less pronounced acceleration due to auto cutbacks. During January total retail inventories rose 0.4% after no change in December. The three month rate of increase was a minimal 0.7% after a 0.2% 4Q rise. Inventories of motor vehicle & parts rose just 0.4% in January after four consecutive months of decline. As a result motor vehicle inventories during the last three months fell at a 4.8% rate after an 8.0% 4Q drop. Motor vehicle inventories were reduced as production was cut back. Outside of autos retail inventories were well behaved through January and rose just 0.4%, half the December rise. That lowered the three month growth rate to 3.3% from 4.3% during 4Q.

The industry detail in the retail sector shows that building materials inventories grew at a 6.4% rate over the last three months versus a 7.6% 4Q gain. Furniture inventories fell at a 5.7% rate after a 2.3% 4Q rise. At clothing & accessory stores the three month rate of accumulation of 0.4% offset a 0.3% rate of decumulation during 4Q. General merchandise stores' inventories rose at a 0.8% rate over the last three months following decumulation at a 1.7% rate during 4Q.

The gains in wholesale inventories have been strong, rising 0.8% in January after a 1.1% December rise. Curiously, the value of inventories of petroleum products fell 3.4% in January and offset half of the prior month's increase. Less petroleum wholesale inventories rose a strong 1.0% and the three month rate of increase nearly doubled to 10.5% versus 4Q. During the last ten years there has been a 59% correlation between the annual change in wholesale inventories less petroleum and the change in merchandise imports.

Business sales rose 1.5% and three month growth was still a firm 9.4% as of January. Much of that strength was due to wholesale sales which grew at a 17.7% rate over the three months. Petroleum industry sales grew at a 76.2% rate but less petroleum wholesale sales still were strong and grew at a 10.7% rate over the last three months.

As of January, strength in sales offset the gain in inventories and the I/S ratio fell to 1.25%, the lowest since 2005.

Inventories, Lumpy Trade, and Large Devaluations from the Federal Reserve Bank of Philadelphia can be found here.

| Business Inventories | January | December | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total | 0.8% | 0.7% | 4.8% | 4.1% | 5.8% | 6.2% |

| Retail | 0.4% | 0.0% | 3.3% | 3.0% | 3.2% | 2.8% |

| Retail excl. Auto | 0.4% | 0.8% | 3.8% | 3.3% | 4.5% | 4.5% |

| Wholesale | 0.8% | 1.1% | 6.4% | 6.1% | 8.5% | 7.4% |

| Manufacturing | 1.3% | 0.9% | 5.0% | 3.7% | 6.4% | 8.9% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief